Philips 2009 Annual Report Download - page 170

Download and view the complete annual report

Please find page 170 of the 2009 Philips annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

|

|

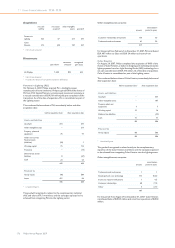

use is measured as the present value of future cash flows expected to be

generated by the asset. If the carrying amount of an asset is deemed not

recoverable, an impairment charge is recognized in the amount by

which the carrying amount of the asset exceeds the recoverable

amount. The review for impairment is carried out at the level where

discrete cash flows occur that are independent of other cash flows.

An impairment loss related to intangible assets other than goodwill,

tangible fixed assets, inventories and equity-accounted investees is

reversed if and to the extent there has been a change in the estimates

used to determine the recoverable amount. The loss is reversed only to

the extent that the asset’s carrying amount does not exceed the

carrying amount that would have been determined, net of depreciation

or amortization, if no impairment loss had been recognized. Reversals

of impairment are recognized in the Statements of income.

Goodwill

Goodwill represents the excess of the cost of an acquisition over the

fair value of the Company’s share of the net identifiable assets of the

acquired subsidiary/equity-accounted investee at the date of

acquisition. Goodwill is measured at cost less accumulated impairment

losses. In respect of equity-accounted investees, the carrying amount of

goodwill is included in the carrying amount of the investment.

Impairment of goodwill

Goodwill is not amortized but tested for impairment annually and

whenever impairment indicators require. In most cases the Company

identified its cash generating units as one level below that of an

operating sector. Cash flows at this level are substantially independent

from other cash flows and this is the lowest level at which goodwill is

monitored by the Board of Management. The Company performed and

completed annual impairment tests in the same quarter of all years

presented in the Consolidated statements of income. A goodwill

impairment loss is recognized in the statement of income whenever and

to the extent that the carrying amount of a cash-generating unit exceeds

the recoverable amount of that unit.

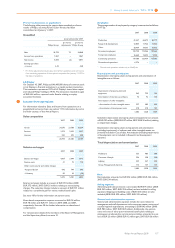

Share capital

Incremental costs directly attributable to the issuance of shares are

recognized as a deduction from equity. When share capital recognized

as equity is repurchased, the amount of the consideration paid, including

directly attributable costs, is recognized as a deduction from equity.

Repurchased shares are classified as treasury shares and are presented

as a deduction from stockholders’ equity.

Debt and other liabilities

Debt and liabilities other than provisions are stated at amortized cost.

However, loans that are hedged under a fair value hedge are

remeasured for the changes in the fair value that are attributable to the

risk that is being hedged.

Provisions

Provisions are recognized if, as a result of a past event, the Company has

a present legal or constructive obligation that can be estimated reliably,

and it is probable that an outflow of economic benefits will be required

to settle the obligation.

Provisions are measured at the present value of the expenditures

expected to be required to settle the obligation using a pre-tax discount

rate that reflects current market assessments of the time value of

money and the risks specific to the obligation. The increase in the

provision due to passage of time is recognized as interest expense.

The Company accrues for losses associated with environmental

obligations when such losses are probable and can be estimated reliably.

Measurement of liabilities is based on current legal and constructive

requirements. Liabilities and expected insurance recoveries, if any, are

recorded separately. The carrying amount of liabilities is regularly

reviewed and adjusted for new facts and changes in law.

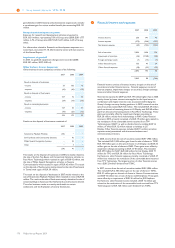

Restructuring

The provision for restructuring relates to the estimated costs of

initiated reorganizations that have been approved by the Board of

Management, and which involve the realignment of certain parts of the

industrial and commercial organization. When such reorganizations

require discontinuance and/or closure of lines of activities, the

anticipated costs of closure or discontinuance are included in

restructuring provisions. A liability is recognized for those costs only

when the Company has a detailed formal plan for the restructuring and

has raised a valid expectation with those affected that it will carry out

the restructuring by starting to implement that plan or announcing its

main features to those affected by it.

Guarantees

The Company recognizes a liability at the fair value of the obligation at

the inception of a financial guarantee contract. The guarantee is

subsequently measured at the higher of the best estimate of the

obligation or the amount initially recognized.

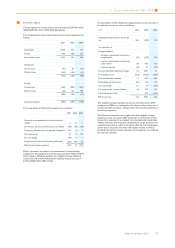

IFRS accounting standards adopted as from 2009

The Company has adopted the following new and amended IFRSs as of

January 1, 2009. None of these standards and/or interpretations had a

material effect on the Consolidated financial statements of the

Company; however certain of these standards affected the disclosures.

Amendment to IFRS 2 ‘Share-based Payment - Vesting Conditions and

Cancellations’

The amendment to IFRS 2 clarifies the definition of vesting conditions,

introduces the concept of non-vesting conditions, requires non-vesting

conditions to be reflected in grant-date fair value and provides the

accounting treatment for non-vesting conditions and cancellations.

Amendment to IFRS 7 ‘Financial Instruments – Disclosures’

The amendment requires enhanced disclosures about fair value

measurement and liquidity risk. In particular, the amendment requires

disclosure of fair value measurements by level of a fair value

measurement hierarchy. This amendment only results in additional

disclosures to the Consolidated financial statements.

Amendments to IAS 1 ‘Presentation of Financial Statements – A revised

presentation’

The amendments to IAS 1 mainly concern the presentation of changes

in equity, in which changes as a result of the transaction with

shareholders should be presented separately and for which a different

format of the overview of the changes in equity can be selected.

Furthermore, an opening balance sheet of the corresponding period is

presented where restatements have occurred. Philips has chosen to

present all non-owner changes in equity in two statements (a separate

Statement of income and a Statement of comprehensive income). These

amendments only impact the presentation aspects of the Consolidation

financial statements.

Amendments to IAS 32 ‘Financial instruments: Presentation’ and IAS 1

‘Presentation of Financial Statements - Puttable Financial Instruments and

Obligations Arising on Liquidation’

The amendments to IAS 32 and IAS 1 are relevant to entities that have

issued financial instruments that are (i) puttable financial instruments or

(ii) instruments, or components of instruments that impose on the

entity an obligation to deliver to another party a pro-rata share of the

net assets of the entity on liquidation. Under the amended IAS 32,

subject to specified criteria being met, these instruments will be

classified as equity.

Improvements to IFRSs 2008

The improvements published under the IASB’s annual improvement

process are intended to deal with non-urgent, minor amendments to

the standards. Most of the improvements are applicable to the

Company on January 1, 2009, some on January 1, 2010. The

improvements to IFRSs 2008 relate mainly to the following:

• Disclosure requirements: Classification as held-for-sale of the assets

and liabilities of a subsidiary where the parent is committed to a plan

to sell its controlling interest but intends to retain a non-controlling

interest.

• Recognition of government grants arising from government loans at

below-market interest.

• Recognition of advertising and promotional expenditure as an asset

is not permitted beyond the point at which the entity has the right to

access the goods purchased or services received.

• Classification of property under construction for investment

purposes as investment property under IAS 40.

11 Group financial statements 11.11 - 11.11

170 Philips Annual Report 2009