Philips 2009 Annual Report Download - page 64

Download and view the complete annual report

Please find page 64 of the 2009 Philips annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

|

|

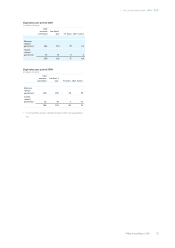

4.1.13 Performance by market cluster

In 2009, sales declined 11% on a comparable basis,

impacted by the global recession, with double-digit sales

declines visible in both mature and emerging markets.

Comparable sales growth by market cluster1)

as a % ■-Philips Group--■-emerging markets--■-mature markets

15

10

5

0

(5)

(10)

(15)

(20)

4.9

10.2

2.8

2007

(2.7)

3.5

(5.4)

2008

(11.4) (10.8) (11.7)

2009

1) For a reconciliation to the most directly comparable GAAP measures, see

chapter 14, Reconciliation of non-GAAP information, of this Annual Report.

The comparatively lower sales in mature markets were

the result of lower sales in all three sectors. In Western

Europe, the sharp sales decline was largely attributable to

lower sales at Consumer Lifestyle, partly due to managed

portfolio pruning, and in Lighting. A double-digit decline

was visible in North America, with lower sales in all

sectors, due to the recession and uncertainty surrounding

the pending US Healthcare Reform Act.

Sales in emerging markets declined 11%, largely impacted

by a double-digit decline in Latin America (Consumer

Lifestyle and Lighting) and a low single-digit decline in

China as growth at Lighting and Healthcare was more than

offset by lower sales at Consumer Lifestyle. Sharp declines

were also visible in Russia, which were partly offset by

slight growth in India and the Middle East.

Sales per market cluster

in millions of euros

■-Western Europe--■-North America--■-other mature--■-emerging

30,000

20,000

10,000

0

2007

10,275

7,147

1,331

8,040

26,793

2008

9,518

7,577

1,269

8,021

26,385

2009

8,431

6,597

1,252

6,909

23,189

EBITA in mature markets improved by EUR 115 million

compared to 2008 as lower EBITA in Western Europe

was more than offset by higher EBITA in North America,

mainly reflecting the effect of a EUR 264 million asbestos-

related settlement charge in 2008. The EBITA decline in

Western Europe was mainly attributable to lower sales at

Consumer and Lifestyle. EBITA improved compared with

2008 in the emerging markets, mainly due to growth at

Healthcare in Latin America and China, lower

restructuring charges and a EUR 131 million curtailment

gain for retiree medical benefit plans.

EBITA per market cluster1,2)

in millions of euros

2007 2008 2009

Western Europe 1,169 283 94

North America 433 219 466

Other mature markets 63 14 71

Total mature markets 1,665 516 631

Emerging markets 429 228 419

2,094 744 1,050

1) For a reconciliation to the most directly comparable GAAP measures, see

chapter 14, Reconciliation of non-GAAP information, of this Annual Report

2) As reported on a geographical basis

EBIT per market cluster1)

in millions of euros

2007 2008 2009

Western Europe 1,146 258 73

North America 233 (402) 105

Other mature markets 63 14 63

Total mature markets 1,442 (130) 241

Emerging markets 425 184 373

1,867 54 614

1) As reported on a geographical basis

4.1.14 Performance by key function

Marketing

Throughout 2009, Philips continued to deliver on its

brand promise of “sense and simplicity”. Driving thought

leadership in Health and Well-being, combined with a

continued focus on Net Promoter Score (NPS) to

improve customer experiences across all touchpoints,

was central to Philips’ marketing strategy in 2009. As a

result, the company moved up to 42nd place on the

Interbrand ranking of the 100 best global brands. This

progression is continued evidence that the promise of

4 Our group performance 4.1.13 - 4.1.14

64 Philips Annual Report 2009