Regions Bank 2010 Annual Report Download - page 110

Download and view the complete annual report

Please find page 110 of the 2010 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

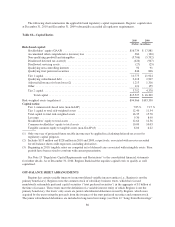

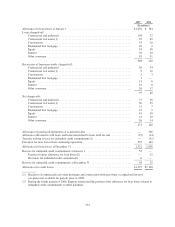

|

|

described above, including the review and approval of new business and ongoing assessments of existing loans in

the portfolio. Independent commercial and consumer credit risk management provides for more accurate risk

ratings and the timely identification of problem credits, as well as oversight for the Chief Credit Officer on

conditions and trends in the credit portfolios.

Credit quality and trends in the loan portfolio are measured and monitored regularly and detailed reports, by

product, business unit and geography, are reviewed by line of business personnel and the Chief Credit Officer.

The Chief Credit Officer reviews summaries of these credit reports with executive management and the Board of

Directors. Finally, the Credit Review department provides ongoing independent oversight of the credit portfolios

to ensure policies are followed, credits are properly risk-rated and that key credit control processes are

functioning as intended.

Risk Characteristics of the Loan Portfolio

In order to assess the risk characteristics of the loan portfolio, Regions considers the current U.S. economic

environment and that of its primary banking markets, as well as risk factors within the major categories of loans.

Economic Environment in Regions’ Banking Markets

The largest factor influencing the credit performance of Regions’ loan portfolio is the overall economic

environment in the U.S. and the primary markets in which it operates. The Great Recession that began in

December 2007 continued through 2008 and into 2009. Through this recessionary period, the overall output of

goods and services experienced its sharpest decline since the early 1980s. Consumer spending, about 70 percent

of all recorded spending, has been adversely impacted by declining inflation-adjusted income, low additional

credit capacity, historically high required monthly debt payments, a negative employment outlook, a higher

savings portion of after-tax personal income, and historically low consumer confidence. However, business

sector output continues to grow, driven by replenishment of inventories that were highly depleted during the

recession.

In 2009, the economic downturn that began with the housing slowdown continued to negatively impact

consumer confidence. In turn, lower confidence levels negatively affected demand for goods and services. This

lower demand impacted retail sales and led to increased vacancy rates and lower rent rolls for the commercial

real estate sector. High unemployment continued in 2009 but began improving in 2010. Residential real estate

prices were stable in 2010; however, concerns remain about the impact on real estate prices from the future sale

of the large supply of homes that are either on bank balance sheets or currently delinquent.

In the fourth quarter of 2010, significant fiscal and monetary stimuli were implemented. On December 17,

2010, the President approved significant tax provisions that are expected to increase consumption, and, thereby,

Gross Domestic Product, in 2011 and 2012. On November 3, 2010, the Federal Reserve approved the purchase of

an additional $600 billion in U.S. Treasury bonds. The combination of these two policy actions should support

growth and dramatically lower the possibility of a second recession in 2011. These actions should also help

mitigate further downside risk for asset prices, in particular real estate prices.

Portfolio Characteristics

Regions has a diversified loan portfolio, in terms of product type, collateral and geography. At

December 31, 2010, commercial loans represented 42 percent of total loans, net of unearned income, investor

real estate loans represented 19 percent, residential first mortgage loans totaled 18 percent and other consumer

loans, largely home equity lending, comprised the remaining 21 percent. Following is a discussion of risk

characteristics of each loan type.

Commercial—The commercial loan portfolio segment totaled $35.1 billion at year-end 2010 and primarily

consists of loans to small and mid-sized commercial and large corporate customers with business operations in

Regions’ geographic footprint. Loans in this portfolio are generally underwritten individually and are usually

96