Regions Bank 2010 Annual Report Download - page 124

Download and view the complete annual report

Please find page 124 of the 2010 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

|

|

Regions has also established processes to ensure appropriate disclosure controls and procedures are

maintained. These controls and procedures as defined by the Securities and Exchange Commission (“SEC”) are

generally designed to ensure that financial and non-financial information required to be disclosed in reports filed

with the SEC is reported within the time periods specified in the SEC’s rules and forms, and that such

information is communicated to management, including the Chief Executive Officer (“CEO”) and Chief

Financial Officer (“CFO”), as appropriate, to allow timely decisions regarding required disclosure.

Regions’ Disclosure Review Committee, which includes representatives from the legal, risk management,

accounting, investor relations and audit departments, meets quarterly to review recent internal and external

events to determine whether all appropriate disclosures have been made in reports filed with the SEC. In

addition, the CEO and CFO meet quarterly with the SEC Filings Review Committee, which includes senior

representatives from accounting, legal, risk management, audit, and operations and technology, as well as from

the core business segments. The SEC Filings Review Committee reviews certain reports to be filed with the SEC,

including Forms 10-K and 10-Q and evaluates the adequacy and accuracy of the disclosures. As part of this

process, certifications of internal control effectiveness are obtained from all core business segments, accounting,

legal, risk management, and operations and technology. These certifications are reviewed and presented to the

CEO and CFO as evidence of the Company’s assessment of internal controls over financial reporting. The Forms

10-K and 10-Q are presented to the Audit Committee of the Board of Directors for approval. Financial results

and other financial information are also reviewed with the Audit Committee on a quarterly basis.

As required by applicable regulatory pronouncements, the CEO and the CFO review and make various

certifications regarding the accuracy of Regions’ periodic public reports filed with the SEC, as well as the

effectiveness of disclosure controls and procedures and internal controls over financial reporting. With the

assistance of the financial review committees, Regions will continue to assess and monitor disclosure controls

and procedures and internal controls over financial reporting, and will make refinements as necessary.

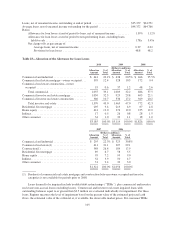

COMPARISON OF 2009 WITH 2008

Regions reported a net loss available to common shareholders of $1.3 billion or $1.27 per diluted common

share in 2009. Significant drivers of 2009 results include an elevated provision for loan losses and pressured net

interest income. Offsetting these items to some extent was Regions’ solid fee and mortgage income.

Net loss from continuing operations in 2009 was $1.3 billion, or $1.27 per diluted common share, compared

to net loss from continuing operations of $5.6 billion, or $8.07 per diluted share in 2008. Regions incurred an $18

million pre-tax loss related to EquiFirst resulting in an after-tax net loss of $11 million, for the year ended

December 31, 2008, which was accounted for as discontinued operations. Net income in 2008 includes after-tax

merger charges of $125 million, or $0.18 per diluted share and a $6 billion non-cash goodwill impairment

charge, or $8.63 per diluted share.

Net interest income was $3.3 billion in 2009 compared to $3.8 billion in 2008. The net interest margin

(taxable-equivalent basis) was 2.67 percent in 2009, compared to 3.23 percent during 2008. The decline in the net

interest margin was impacted primarily by factors directly and indirectly associated with the erosion of economic

and industry conditions since late 2007. These factors include Regions’ asset sensitive balance sheet, which was

impacted by an unfavorable decline in the general level and shape of the yield curve, higher spreads on new debt

issuances, and rising non-performing asset levels. Additionally, loan yields declined throughout the year, as

variable rate loans fell in response to declines in the short-term rates to which they are tied. Declining deposit

rates partially offset these movements, but the decline was somewhat limited by the competitive demand for

deposits within the industry, largely prompted by stressed economic conditions throughout the U.S.

The following discussion of non-interest income and expense is from continuing operations and excludes

EquiFirst, which is reported separately as discontinued operations in the consolidated statements of operations.

Non-interest income totaled $3.8 billion in 2009, compared to $3.1 billion in 2008. The increase in non-interest

110