Regions Bank 2010 Annual Report Download - page 126

Download and view the complete annual report

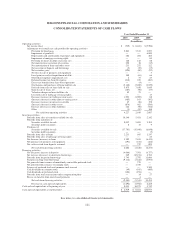

Please find page 126 of the 2010 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

|

|

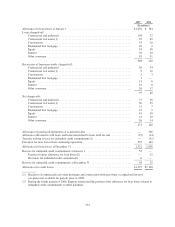

Professional and legal fees are comprised of amounts related to legal, consulting and other professional fees.

These fees increased $95 million to $309 million in 2009. Included in professional fees during 2008 were $7

million of merger-related charges. The increase in 2009 is primarily due to higher legal expenses incurred at

Morgan Keegan and credit-related legal costs (such as legal fees associated with loan work-outs).

Other real estate owned (“OREO”) expenses include the cost of adjusting foreclosed properties to fair value

after these assets have been classified as OREO and net gains and losses on sales of properties, as well as other

costs to maintain the property such as property taxes, security, grounds maintenance, etc. Foreclosed properties

balances increased $364 million to $607 million in 2009 compared to $243 million in 2008 due to increasing

numbers of foreclosures. OREO expense increased $72 million to $175 million in 2009 compared to $103

million in 2008, driven by the significant increase in OREO balances, coupled with property valuation declines

resulting from further deterioration of the housing and real estate markets.

Marketing expenses decreased $22 million during 2009 to $75 million compared to $97 million in 2008.

The decrease was driven by $13 million of merger-related charges in 2008.

Mortgage servicing rights impairment was $85 million in 2008. There was no impairment related to

mortgage servicing rights in 2009 as the Company elected the fair value method as of January 1, 2009.

FDIC premiums, including a special assessment, increased $212 million to $227 million in 2009. The

increases resulted from higher premium rates applied to a higher level of insured deposit balances. The FDIC

made a number of changes to its assessment rate schedule, which drove the increase in premium rates. The bank

regulatory agencies’ ratings, comprised of Regions Bank’s capital, asset quality, management, earnings, liquidity

and sensitivity to risk, along with its long-term debt issuer ratings and financial ratios, were the primary factors in

determining FDIC insurance premiums.

Other miscellaneous expenses include communications, and business development services. Other

miscellaneous expenses decreased $186 million to $736 million in 2009. Included in other miscellaneous

expenses are merger charges totaling $38 million in 2008. The decline in 2009 was attributable to several factors.

As discussed above, in January 2009, Regions began accounting for mortgage servicing rights at fair market

value with any changes to fair value being recorded in mortgage income. At that time, Regions was no longer

required to adjust non-interest expense for amortization of mortgage servicing rights. The impact of the

amortization expense for 2008 was $75 million and there was no corresponding impact in 2009. Also, included in

other non-interest expense in 2008 was $49 million of write-downs on investments in two Morgan Keegan

mutual funds with no similar expense during 2009.

Regions’ 2009 benefit for income taxes from continuing operations decreased $177 million to a tax benefit

of $171 million compared to a tax benefit of $348 million in 2008. The decrease in the benefit is primarily

related to the tax expenses on leveraged lease terminations in 2009.

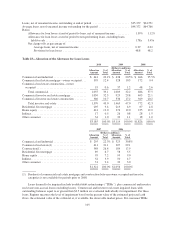

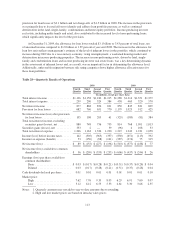

Net charge-offs totaled $2.3 billion, or 2.38 percent of average loans in 2009 compared to $1.5 billion, or

1.59 percent of average loans in 2008. The increased loss rate reflected ongoing pressure in property valuations

and continued strains in the economy as a whole. Non-performing assets increased $2.7 billion between

December 31, 2009 and December 31, 2008 to $4.4 billion, primarily due to continued weakness in the

Company’s land, single-family and condominium portfolios. Non-performing assets held for sale totaled $317

million and $423 million at December 31, 2009 and 2008, respectively.

The provision for loan losses is used to maintain the allowance for loan losses at a level that in

management’s judgment is adequate to cover losses inherent in the portfolio at the balance sheet date. During

2009 the provision for loan losses was $3.5 billion and net charge-offs were $2.3 billion. This compares to a

112