Regions Bank 2010 Annual Report Download - page 86

Download and view the complete annual report

Please find page 86 of the 2010 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

|

|

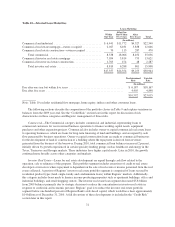

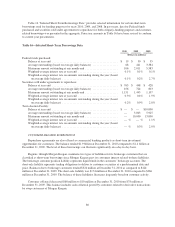

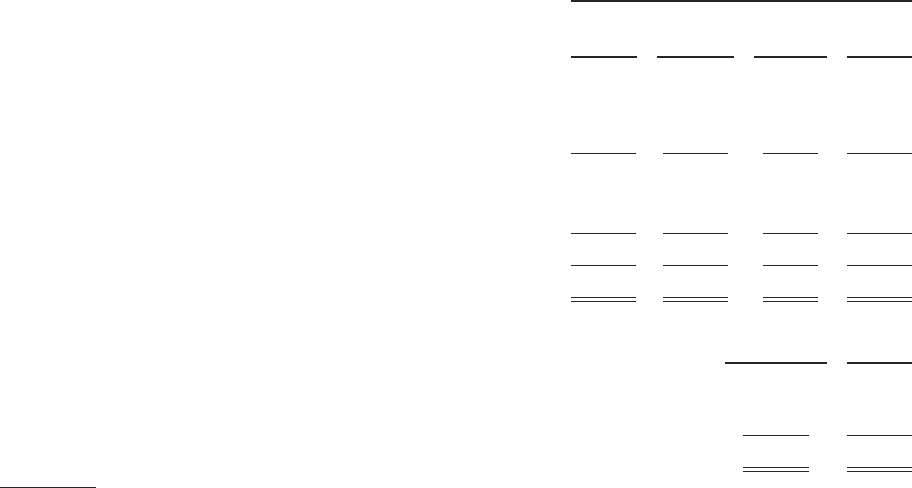

Table 10—Selected Loan Maturities

Loans Maturing

Within

One Year

After One

But Within

Five Years

After

Five Years Total

(In millions)

Commercial and industrial ................................. $ 6,441 $11,772 $4,327 $22,540

Commercial real estate mortgage—owner-occupied ............. 2,027 6,181 3,838 12,046

Commercial real estate construction—owner occupied ........... 70 113 287 470

Total commercial .................................... 8,538 18,066 8,452 35,056

Commercial investor real estate mortgage ..................... 7,054 5,814 753 13,621

Commercial investor real estate construction ................... 1,765 474 48 2,287

Total investor real estate ............................... 8,819 6,288 801 15,908

$17,357 $24,354 $9,253 $50,964

Predetermined

Rate

Variable

Rate

(In millions)

Due after one year but within five years ...................................... $ 6,187 $18,167

Due after five years ...................................................... 4,405 4,848

$10,592 $23,015

Note: Table 10 excludes residential first mortgage, home equity, indirect and other consumer loans.

The following sections describe the composition of the portfolio classes in Table 9 and explain variations in

balances from the 2009 year-end. See the “Credit Risk” section later in this report for discussion of risk

characteristics in these categories and Regions’ management of those risks.

Commercial—The Commercial category includes commercial and industrial, representing loans to

commercial customers for use in normal business operations to finance working capital needs, equipment

purchases and other expansion projects. Commercial also includes owner-occupied commercial real estate loans

to operating businesses, which are loans for long-term financing of land and buildings, and are repaid by cash

flow generated by business operations. Owner-occupied construction loans are made to commercial businesses

for the development of land or construction of a building where the repayment is derived from revenues

generated from the business of the borrower. During 2010, total commercial loan balances increased 2 percent,

initially driven by growth experienced in certain specialty lending groups such as healthcare and energy in the

Texas, Tennessee and Georgia markets. These industries have higher capital needs. Later in 2010, the growth

continued more broadly across other categories and markets.

Investor Real Estate—Loans for real estate development are repaid through cash flow related to the

operation, sale or refinance of the property. This portfolio segment includes extensions of credit to real estate

developers or investors where repayment is dependent on the sale of real estate or income generated from the real

estate collateral. A portion of Regions’ investor real estate portfolio segment is comprised of loans secured by

residential product types (land, single-family and condominium loans) within Regions’ markets. Additionally,

this category includes loans made to finance income-producing properties such as apartment buildings, office and

industrial buildings, and retail shopping centers. The investor real estate loan segment decreased $5.8 billion

from 2009 balances primarily due to strategic decisions to reduce the concentration in investor real estate in

response to credit risk and economic pressure. Regions’ goal is to reduce the investor real estate portfolio

segment below one hundred percent of Regions Bank’s risk-based capital, which would have been approximately

$14 billion as of December 31, 2010. A full discussion of these developments is included in the “Credit Risk”

section later in this report.

72