Regions Bank 2010 Annual Report Download - page 120

Download and view the complete annual report

Please find page 120 of the 2010 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

|

|

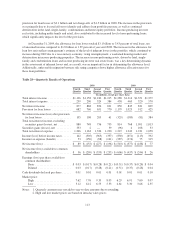

Regions measures the level of impairment based on pools of loans stratified by common risk characteristics. If

current valuations are lower than the current book balance of the credit, the negative differences are reviewed for

possible charge-off. In instances where management determines that a charge-off is not appropriate, a specific

reserve is established for the individual loan in question. This specific reserve is incorporated as a part of the

overall allowance for credit losses. The recorded investment in impaired loans was approximately $4.5 billion at

December 31, 2010 and $5.0 billion at December 31, 2009. Loans that were characterized as TDRs totaled $2.1

billion and $1.9 billion at December 31, 2010 and 2009, respectively. The allowance allocated to TDRs totaled

$224 million and $57 million at December 31, 2010 and 2009, respectively. For further details on impaired loans

and the allowance for credit losses, see Note 5 “Allowance for Credit Losses” to the consolidated financial

statements.

Regions continues to work to meet the individual needs of consumer borrowers to stem foreclosure through

the Customer Assistance Program (“CAP”). Regions designed the program to allow for customer-tailored

modifications with the goal of keeping customers in their homes and avoiding foreclosure where possible.

Modification may be offered to any borrower experiencing financial hardship—regardless of the borrower’s

payment status. Under the CAP, Regions may offer a short-term deferral, a term extension, an interest rate

reduction, a new loan product, or a combination of these options. Regions evaluates the success of the

modification program (the “recidivism rate”). The recidivism rate is the 60-day and greater delinquency rate

inclusive of non-accruing loans for all TDRs which were restructured six months or prior to the reporting period.

For CAP modifications, this rate is currently approximately 22 percent. For loans restructured under CAP,

Regions expects to collect the original contractually due principal. The gross original contractual interest may be

collectible, depending on the terms modified. The length of the CAP modifications ranges from temporary

payment deferrals of three months to term extensions for the life of the loan. All such modifications are

considered TDRs regardless of the term if there is a concession to a borrower experiencing financial difficulty.

Modified loans are subject to policies governing accrual/nonaccrual evaluation consistent with all other loans of

the same product type. Consumer loans are subject to objective accrual/nonaccrual decisions. Under these

policies, loans subject to CAP are charged down to estimated value and placed on nonaccrual status on or before

the month in which the loan becomes 180 days past due. Because the program was designed to evaluate potential

CAP participants as early as possible in the lifecycle of the troubled loan, many of the modifications are finalized

without the borrower ever reaching 180 days past due, and with the loans having never been placed on

nonaccrual. Accordingly, given the positive impact of the restructuring on the likelihood of recovery of cash

flows due under the modified terms, accrual status continues to be appropriate for these loans. None of the

modified consumer loans listed in the TDR disclosures were collateral-dependent at the time of modification. At

December 31, 2010, approximately $153 million in residential first mortgage TDRs and approximately $9

million in home equity TDRs were in excess of 180 days past due and are considered collateral-dependent.

106