Regions Bank 2010 Annual Report Download - page 190

Download and view the complete annual report

Please find page 190 of the 2010 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

|

|

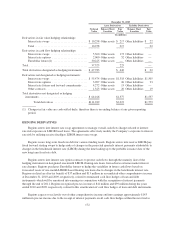

zero recovery. The fair value of sold protection at December 31, 2010 was immaterial. In transactions where

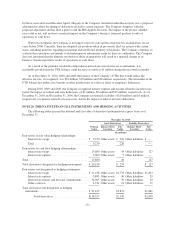

Regions has sold credit protection, recourse to collateral associated with the original swap transaction is available

to offset some or all of Regions’ obligation.

CONTINGENT FEATURES

Certain of Regions Bank’s derivative instrument contracts with broker-dealers contain provisions allowing

those broker-dealers to terminate the contracts in the event that Regions’ and/or Regions Bank’s credit rating

falls below specified ratings from certain major credit rating agencies. During the fourth quarter 2010, Regions

and Regions Bank experienced ratings downgrades from major credit rating agencies. At December 31, 2010,

Moody’s credit ratings for Regions and Regions Bank were below investment grade, and S&P credit ratings for

Regions were below investment grade. As a result of these downgrades, certain of Regions Bank’s broker-dealer

counterparties could have terminated these contracts at their discretion. In lieu of terminating the contracts,

Regions Bank and certain of its broker-dealer counterparties amended the contracts such that Regions Bank was

required to post additional collateral in the cumulative amount of $195 million to theses counterparties.

Some of these contracts with broker-dealers still contain credit-related termination provisions and/or credit-

related provisions regarding the posting of collateral. At December 31, 2010, the net fair value of such contracts

containing credit-related termination provisions that were in a liability position was $446 million, for which

Regions had posted collateral of $591 million. At December 31, 2010, the net fair value of contracts that do not

contain credit-related termination provisions that were in a liability position was $224 million for which Regions

had posted collateral of $219 million. Other derivative contracts with broker-dealers do not contain any credit-

related provisions. These counterparties require complete overnight collateralization.

The aggregate fair value of all derivative instruments with any credit-risk-related contingent features that are

in a liability position on December 31, 2010 and 2009, was $508 million and $261 million, respectively, for

which Regions had posted collateral of $652 million and $247 million, respectively, in the normal course of

business.

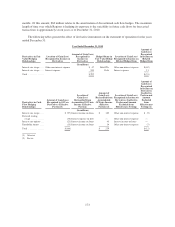

NOTE 21. FAIR VALUE MEASUREMENTS

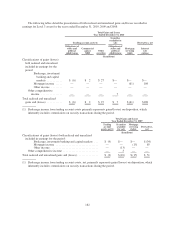

Fair value guidance establishes a framework for using fair value to measure assets and liabilities and defines

fair value as the price that would be received to sell an asset or paid to transfer a liability (an exit price) as

opposed to the price that would be paid to acquire the asset or received to assume the liability (an entry price). A

fair value measure should reflect the assumptions that market participants would use in pricing the asset or

liability, including the assumptions about the risk inherent in a particular valuation technique, the effect of a

restriction on the sale or use of an asset and the risk of nonperformance. Required disclosures include

stratification of balance sheet amounts measured at fair value based on inputs the Company uses to derive fair

value measurements. These strata include:

• Level 1 valuations, where the valuation is based on quoted market prices for identical assets or

liabilities traded in active markets (which include exchanges and over-the-counter markets with

sufficient volume),

• Level 2 valuations, where the valuation is based on quoted market prices for similar instruments traded

in active markets, quoted prices for identical or similar instruments in markets that are not active and

model-based valuation techniques for which all significant assumptions are observable in the market,

and

• Level 3 valuations, where the valuation is generated from model-based techniques that use significant

assumptions not observable in the market, but observable based on Company-specific data. These

unobservable assumptions reflect the Company’s own estimates for assumptions that market

176