Regions Bank 2010 Annual Report Download - page 201

Download and view the complete annual report

Please find page 201 of the 2010 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

|

|

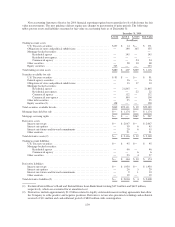

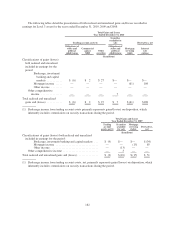

The carrying amounts and estimated fair values of the Company’s financial instruments as of December 31

are as follows:

December 31, 2010 December 31, 2009

Carrying

Amount

Estimated

Fair

Value(1)

Carrying

Amount

Estimated

Fair

Value(1)

(In millions)

Financial assets:

Cash and cash equivalents .................................. $ 6,919 $ 6,919 $ 8,011 $ 8,011

Trading account assets ..................................... 1,116 1,116 3,039 3,039

Securities available for sale ................................. 23,289 23,289 24,069 24,069

Securities held to maturity .................................. 24 26 31 31

Loans held for sale ........................................ 1,485 1,485 1,511 1,511

Loans (excluding leases), net of unearned income and allowance for

loan losses(2), (3) ....................................... 77,864 69,775 85,452 72,119

Other interest-earning assets ................................ 1,219 1,219 734 734

Derivatives, net ........................................... 140 140 520 520

Financial liabilities:

Deposits ................................................ 94,614 94,883 98,680 99,168

Short-term borrowings ..................................... 3,937 3,937 3,668 3,668

Long-term borrowings ..................................... 13,190 13,115 18,464 17,710

Loan commitments and letters of credit ........................ 125 899 194 1,014

(1) Estimated fair values are consistent with an exit price concept. The assumptions used to estimate the fair

values are intended to approximate those that a market participant would use in a hypothetical orderly

transaction. In estimating fair value, the Company makes adjustments for interest rates, market liquidity and

credit spreads as appropriate.

(2) The estimated fair value of portfolio loans assumes sale of the loans to a third-party financial investor.

Accordingly, the value to the Company if the loans were held to maturity is not reflected in the fair value

estimate. In the current whole loan market, financial investors are generally requiring a higher rate of return

than the return inherent in loans if held to maturity. The fair value discount at December 31, 2010 was $8.1

billion or 10.4 percent.

(3) Excluded from this table is the lease carrying amount of $1.8 billion at December 31, 2010 and $2.1 billion

at December 31, 2009.

NOTE 22. BUSINESS SEGMENT INFORMATION

Regions’ segment information is presented based on Regions’ key segments of business. Each segment is a

strategic business unit that serves specific needs of Regions’ customers. The Company’s primary segment is

Banking/Treasury, which represents the Company’s branch network, including consumer and commercial

banking functions, and has separate management that is responsible for the operation of that business unit. This

segment also includes the Company’s Treasury function, including the Company’s securities portfolio and other

wholesale funding activities.

In addition to Banking/Treasury, Regions has designated as distinct reportable segments the activity of its

Investment Banking/Brokerage/Trust and Insurance divisions. Investment Banking/Brokerage/Trust includes

trust activities and all brokerage and investment activities associated with Morgan Keegan. Insurance includes all

business associated with commercial insurance and credit life products sold to consumer customers.

During 2010, minor reclassifications were made from the Banking/Treasury segment to the Insurance

segment to more appropriately present management’s current view of the segments. The 2009 and 2008 amounts

presented below have been adjusted to conform to the 2010 presentation.

187