Regions Bank 2010 Annual Report Download - page 158

Download and view the complete annual report

Please find page 158 of the 2010 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

|

|

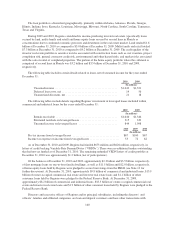

customers to borrow against the equity in their home. Real estate market values as of the time the loan or line is

secured directly affect the amount of credit extended and, in addition, changes in these values impact the depth of

potential losses. Indirect lending, which is lending initiated through third-party business partners, is largely

comprised of loans made through automotive dealerships. Other consumer loans include direct consumer

installment loans, overdrafts and other revolving credit, and educational loans. Loans in this portfolio segment

are sensitive to unemployment and other key consumer economic measures.

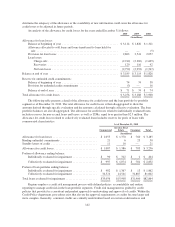

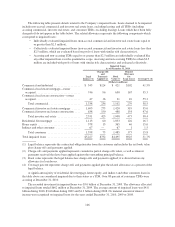

The following table presents credit quality indicators for the loan portfolio segments and classes, excluding

loans held for sale. Commercial and investor real estate loan classes are detailed by categories related to

underlying credit quality and probability of default. These categories are utilized to develop the associated

allowance for credit losses using historical losses adjusted for current economic conditions and are defined as

follows:

• Pass—includes obligations where the probability of default is considered low;

• Other Loans Especially Mentioned (“OLEM”)—includes obligations that have potential weakness

which may, if not reversed or corrected, weaken the credit or inadequately protect the Company’s

position at some future date. Obligations in this category may also be subject to economic or market

conditions which may, in the future, have an adverse affect on debt service ability;

• Substandard Accrual—includes obligations that exhibit a well-defined weakness which presently

jeopardizes debt repayment, even though they are currently performing. These obligations are

characterized by the distinct possibility that the Company may incur a loss in the future if these

weaknesses are not corrected;

• Non-accrual—includes obligations where management has determined that full payment of principal

and interest is in doubt.

Classes in the consumer portfolio segment are disaggregated by accrual status. Consumer loans are charged

down to estimated value and placed on non-accrual status based on period of delinquency, unless the loan is well-

secured and in process of collection. The associated allowance for credit losses is generally based on historical

losses of the various classes adjusted for current economic conditions.

December 31, 2010

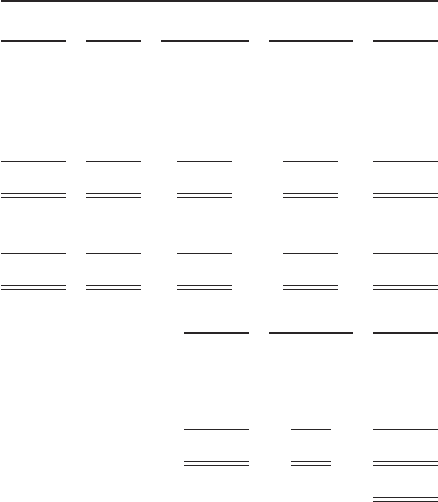

Pass OLEM

Substandard

Accrual Non-accrual Total

(In millions)

Commercial and industrial ........................ $20,764 $ 517 $ 792 $ 467 $22,540

Commercial real estate mortgage—owner occupied .... 10,344 283 813 606 12,046

Commercial real estate construction—owner

occupied .................................... 393 25 23 29 470

Total commercial ........................... $31,501 $ 825 $1,628 $1,102 $35,056

Commercial investor real estate mortgage ........... 8,755 1,300 2,301 1,265 13,621

Commercial investor real estate construction ......... 904 342 589 452 2,287

Total investor real estate ..................... $ 9,659 $1,642 $2,890 $1,717 $15,908

Accrual Non-accrual Total

(In millions)

Residential first mortgage .......................................... $14,613 $285 $14,898

Home equity ..................................................... 14,170 56 14,226

Indirect and other consumer ......................................... 2,776 — 2,776

Total consumer ............................................... $31,559 $341 $31,900

$82,864

144