Regions Bank 2010 Annual Report Download - page 72

Download and view the complete annual report

Please find page 72 of the 2010 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

|

|

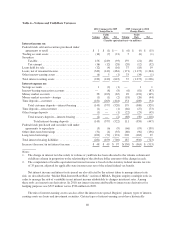

The Company is subject to income tax in the U.S. and multiple state and local jurisdictions. The tax laws

and regulations in each jurisdiction may be interpreted differently in certain situations, which could result in a

range of outcomes. Thus, the Company is required to exercise judgment regarding the application of these tax

laws and regulations. In the event a dispute with a taxing authority arises, the Company will evaluate and

recognize tax liabilities related to the tax uncertainties. Due to the complexity of some of these uncertainties, the

ultimate resolution may result in a payment that is different from the current estimate of the tax liabilities.

The Company’s estimate of accrued income taxes, deferred income taxes and income tax expense can also

change in any period as a result of new legislative or judicial guidance impacting tax positions, as well as

changes in income tax rates. Any changes, if they occur, can be significant to the Company’s financial position,

results of operations or cash flows.

OPERATING RESULTS

GENERAL

Regions reported a net loss available to common shareholders of $763 million in 2010, compared to a net

loss available to common shareholders of $1.3 billion in 2009. The lower loss in 2010 was primarily reflective of

moderation in credit quality within the Company’s loan portfolio. However, the provision for loan losses

remained elevated.

NET INTEREST INCOME AND MARGIN

Net interest income (interest income less interest expense) is Regions’ principal source of income and is one

of the most important elements of Regions’ ability to meet its overall performance goals. Net interest income on

a taxable-equivalent basis increased 3 percent to $3.5 billion in 2010 from $3.4 billion in 2009 despite a decrease

in the level of average earning assets, from $125.9 billion in 2009 to $119.3 billion in 2010. The increase in the

net interest margin to 2.90 percent in 2010 from 2.67 percent in 2009 was sufficient to offset the impact of the

smaller balance sheet size.

Comparing 2010 to 2009, interest-earning asset yields were lower, decreasing 30 basis points on average.

However, interest-bearing liability rates were also lower, declining by 60 basis points, which was more than

enough improvement in funding costs to offset the drop in interest-earning asset yields. As a result, the net

interest rate spread increased 30 basis points to 2.58 percent in 2010 as compared to 2.28 percent in 2009.

Continued low levels of long-term interest rates affected interest-earning asset yields through their influence on

the behavior and pricing of fixed-rate loans and securities. Longer-term rates remained at historical low levels and

fluctuated throughout the year. The yield on the benchmark 10-year U.S. Treasury note ranged from a high of 4.01

percent to a low of 2.41 percent, and for the year decreased 55 basis points, ending the year at 3.30 percent.

Persistently low long-term rates can incent fixed-rate borrowers to accelerate reductions or prepayments of existing

loans, often at lower rates of interest. This results in pressure on yields for portfolios that have a significant

concentration of fixed-rate loans. The taxable investment securities portfolio, which contains significant residential

fixed-rate exposure, for example, decreased in yield from 4.78 percent in 2009 to 3.66 percent in 2010.

The negative influence of low, long-term interest rates on net interest margin, however, was offset by

improvements in liability costs. The Federal Funds rate and the Prime Rate, which are influential drivers of loan

and deposit pricing on the shorter end of the yield curve, remained low at approximately 0.25 percent and 3.25

percent, respectively, throughout 2010, essentially unchanged from the previous year-end level. Despite the lack

of movement in short-term rates compared to historic lows, deposit costs improved considerably from 1.35

percent in 2009 to 0.78 percent in 2010. There was substantial improvement in costs in every deposit category,

including average money market accounts which declined from 0.84 percent to 0.43 percent, and yet experienced

an increase in average total balance from $21.4 billion in 2009 to $26.8 billion in 2010. The improvement in

overall deposit cost was also attributable to a less costly mix of deposits. For example, average time deposits

declined from $32.7 billion in 2009 to $26.2 billion in 2010. Meanwhile, average non-interest bearing customer

deposits increased from $20.7 billion in 2009 to $24.0 billion in 2010.

58