Regions Bank 2010 Annual Report Download - page 114

Download and view the complete annual report

Please find page 114 of the 2010 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

|

|

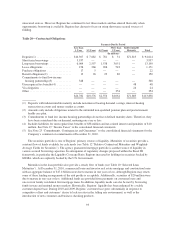

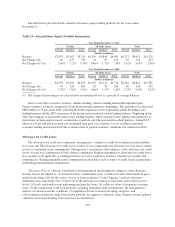

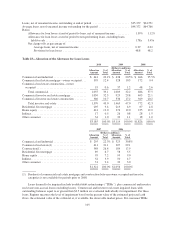

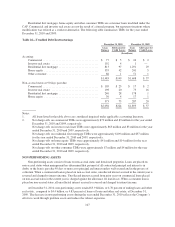

The table below provides details related to the home equity lending portfolio for the years ended

December 31:

Table 23—Selected Home Equity Portfolio Information

Year Ended December 31, 2010

Florida All Other States Total

1st Lien 2nd Lien Total 1st Lien 2nd Lien Total 1st Lien 2nd Lien Total

(Dollars in millions)

Balance .............. $2,074 $3,167 $5,241 $4,139 $4,846 $8,985 $6,213 $8,013 $14,226

Net Charge-offs ....... 56 237 293 34 87 121 90 324 414

Net Charge-off %(1) .... 2.66% 7.12% 5.38% 0.80% 1.71% 1.30% 1.42% 3.85% 2.80%

Year Ended December 31, 2009

Florida All Other States Total

1st Lien 2nd Lien Total 1st Lien 2nd Lien Total 1st Lien 2nd Lien Total

(Dollars in millions)

Balance .............. $2,170 $3,485 $5,655 $4,395 $5,331 $9,726 $6,565 $8,816 $15,381

Net Charge-offs ....... 59 250 309 30 76 106 89 326 415

Net Charge-off %(1) .... 2.75% 7.01% 5.41% 0.66% 1.37% 1.05% 1.33% 3.58% 2.63%

(1) Net charge-off percentages are calculated on an annualized basis as a percent of average balances.

Indirect and Other Consumer Lending—Indirect lending, which is lending initiated through third-party

business partners, is largely comprised of loans made through automotive dealerships. This portfolio class decreased

$860 million or 35 percent in 2010, reflecting the 2008 suspension of new originations within the indirect auto

lending business and the 2007 suspension of the marine and recreational vehicle lending business. Beginning in late

2010, the Company re-entered the indirect auto lending business. Other consumer loans, which consist primarily of

borrowings for home improvements, automobiles, overdrafts and other personal household purposes, totaled $1.2

billion as of year-end and were relatively unchanged from prior year’s balance. Losses on indirect and other

consumer lending increased in 2009 due to deterioration of general economic conditions, but stabilized in 2010.

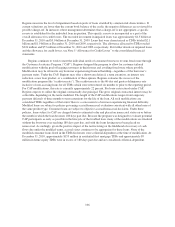

Allowance for Credit Losses

The allowance for credit losses represents management’s estimate of credit losses inherent in the portfolio

as of year-end. The allowance for credit losses consists of two components: the allowance for loan losses and the

reserve for unfunded credit commitments. Management’s assessment of the adequacy of the allowance for credit

losses is based on a combination of both of these components. Regions determines its allowance for credit losses

in accordance with applicable accounting literature as well as regulatory guidance related to receivables and

contingencies. Binding unfunded credit commitments include items such as letters of credit, financial guarantees

and binding unfunded loan commitments.

Allowance Process—Factors considered by management in determining the adequacy of the allowance

include, but are not limited to: (1) detailed reviews of individual loans; (2) historical and current trends in gross

and net loan charge-offs for the various classes of loans evaluated; (3) the Company’s policies relating to

delinquent loans and charge-offs; (4) the level of the allowance in relation to total loans and to historical loss

levels; (5) levels and trends in non-performing and past due loans; (6) collateral values of properties securing

loans; (7) the composition of the loan portfolio, including unfunded credit commitments; (8) management’s

analysis of current economic conditions; (9) migration of loans between risk rating categories; and

(10) estimation of inherent credit losses in the portfolio. In support of collateral values, Regions obtains updated

valuations for non-performing loans on at least an annual basis.

100