Regions Bank 2010 Annual Report Download - page 121

Download and view the complete annual report

Please find page 121 of the 2010 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

|

|

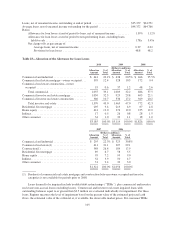

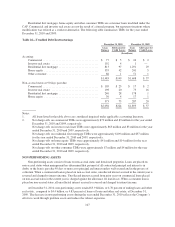

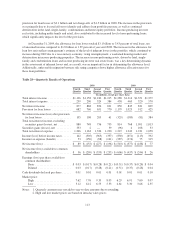

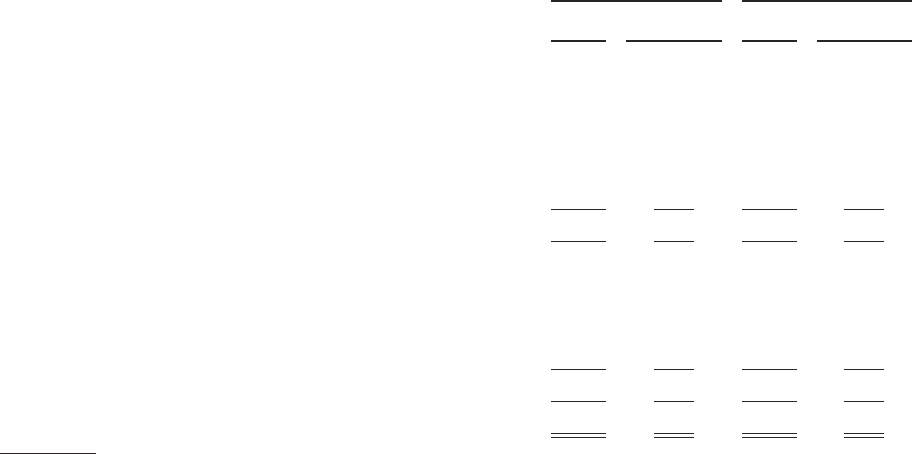

Residential first mortgage, home equity and other consumer TDRs are consumer loans modified under the

CAP. Commercial and investor real estate are not the result of a formal program, but represent situations where

modification was offered as a workout alternative. The following table summarizes TDRs for the years ended

December 31, 2010 and 2009:

Table 26—Troubled Debt Restructurings

December 31, 2010 December 31, 2009

Loan

Balance

Allowance for

Credit Losses

Loan

Balance

Allowance for

Credit Losses

(In millions)

Accruing:

Commercial ....................................... $ 77 $ 5 $ 24 $ 2

Investor real estate ................................. 192 4 1 —

Residential first mortgage ............................ 813 97 1,291 29

Home equity ...................................... 335 42 241 5

Other consumer .................................... 66 1 51 1

$1,483 $149 $1,608 $ 37

Non-accrual status or 90 days past due:

Commercial ....................................... $ 105 $ 23 $ 17 $ 2

Investor real estate ................................. 198 20 75 16

Residential first mortgage ............................ 240 28 178 1

Home equity ...................................... 30 4 17 1

573 75 287 20

$2,056 $224 $1,895 $ 57

Notes:

1. All loans listed in the table above are considered impaired under applicable accounting literature.

2. Net charge-offs on commercial TDRs were approximately $72 million and $9 million for the year ended

December 31, 2010 and 2009, respectively.

Net charge-offs on investor real estate TDRs were approximately $63 million and $3 million for the year

ended December 31, 2010 and 2009, respectively.

Net charge-offs on residential first mortgage TDRs were approximately $109 million and $57 million

for the year ended December 31, 2010 and 2009, respectively.

Net charge-offs on home equity TDRs were approximately $41 million and $14 million for the year

ended December 31, 2010 and 2009, respectively.

Net charge-offs on other consumer TDRs were approximately $7 million and $4 million for the year

ended December 31, 2010 and 2009, respectively.

NON-PERFORMING ASSETS

Non-performing assets consist of loans on non-accrual status and foreclosed properties. Loans are placed on

non-accrual status when management has determined that payment of all contractual principal and interest is in

doubt, or the loan is past due 90 days or more as to principal and interest unless well-secured and in the process of

collection. When a commercial loan is placed on non-accrual status, uncollected interest accrued in the current year is

reversed and charged to interest income. Uncollected interest accrued from prior years on commercial loans placed

on non-accrual status in the current year is charged against the allowance for loan losses. When a consumer loan is

placed on non-accrual status, all uncollected interest accrued is reversed and charged to interest income.

At December 31, 2010, non-performing assets totaled $3.9 billion, or 4.70 percent of ending loans and other

real estate , compared to $4.4 billion, or 4.83 percent of loans of loans and other real estate, at December 31,

2009. The decrease in non-performing assets during the year ended December 31, 2010 reflects the Company’s

efforts to work through problem assets and reduce the riskiest exposures.

107