Regions Bank 2010 Annual Report Download - page 155

Download and view the complete annual report

Please find page 155 of the 2010 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

|

|

Regions in the ordinary course of business. Total loans to these persons (excluding loans which in the aggregate

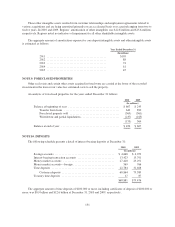

do not exceed $60,000 to any such person) at December 31, 2010 and 2009 were approximately $156 million and

$266 million, respectively. These loans were made in the ordinary course of business and on substantially the

same terms, including interest rates and collateral, as those prevailing at the same time for comparable

transactions with other persons and involve no unusual risk of collectability.

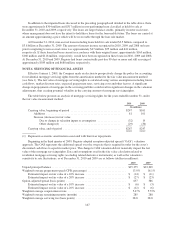

NOTE 5. ALLOWANCE FOR CREDIT LOSSES

The allowance for credit losses represents management’s estimate of credit losses inherent in the loan and

credit commitment portfolios as of year-end. The allowance for credit losses consists of two components: the

allowance for loan and lease losses and the reserve for unfunded credit commitments. Management’s assessment

of the adequacy of the allowance for credit losses is based on a combination of both of these components.

Regions determines its allowance for credit losses in accordance with applicable accounting literature as well as

regulatory guidance related to receivables and contingencies. Binding unfunded credit commitments include

items such as letters of credit, financial guarantees and binding unfunded loan commitments.

Allowance Process—Factors considered by management in determining the adequacy of the allowance

include, but are not limited to: (1) detailed reviews of individual loans that result in risk ratings; (2) historical and

current trends in gross and net loan charge-offs for the various classes of loans evaluated; (3) the Company’s

policies relating to delinquent loans and charge-offs; (4) the level of the allowance in relation to total loans and to

historical loss levels; (5) levels and trends in non-performing and past due loans; (6) collateral values of

properties securing loans; (7) the composition of the loan portfolio, including unfunded credit commitments;

(8) management’s analysis of current economic conditions; (9) migration of loans between risk rating categories;

and (10) estimation of inherent credit losses in the portfolio. In support of collateral values, Regions obtains

updated valuations for non-performing loans on at least an annual basis.

Credit Risk Management and the Special Assets Division (specializes in managing distressed credit

exposure) are both involved in the credit risk management process to assess the accuracy of risk ratings, the

quality of the portfolio and the estimation of inherent credit losses in the loan portfolio. This comprehensive

process also assists in the prompt identification of problem credits. The Company has taken a number of

measures to manage the portfolios and reduce risk, particularly in the more problematic portfolios. In addition, a

strong Customer Assistance Program is in place which educates consumer loan customers about options and

initiates early contact with customers to discuss solutions when a loan first becomes delinquent.

For loans that are not specifically reviewed, management uses information from its ongoing review

processes to stratify the loan portfolio segments into pools sharing common risk characteristics. Loans that share

common risk characteristics are assigned a portion of the allowance for credit losses based on the assessment

process described above. Credit exposures are categorized by type and assigned estimated amounts of inherent

loss based on several factors, including current and historical loss experience for each pool and management’s

judgment of current economic conditions and their expected impact on credit performance. Adjustments to the

allowance for credit losses calculated using a pooled approach are recorded through the provision for loan losses

or non-interest expense, as applicable.

As a matter of business practice, Regions may require some form of credit support, such as a guarantee.

Guarantees are legally binding and entered into simultaneously with the primary loan agreements. Regions

underwrites the ability of each guarantor to perform under its guarantee in the same manner and to the same

extent as would be required to underwrite the repayment plan of a direct obligor. This entails obtaining sufficient

information on the guarantor, including financial and operating information, to sufficiently measure a guarantor’s

ability to perform, under the guarantee. However, the benefit assigned to credit support within the calculation of

the allowance for credit losses is not material to the consolidated financial statements.

Management considers the current level of allowance for credit losses adequate to absorb losses inherent in

the loan portfolio and unfunded commitments. Management’s determination of the adequacy of the allowance for

credit losses, which is based on the factors and risk identification procedures previously discussed, requires the

use of judgments and estimations that may change in the future. Changes in the factors used by management to

141