Bank of America 2007 Annual Report Download - page 120

Download and view the complete annual report

Please find page 120 of the 2007 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

|

|

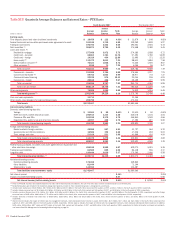

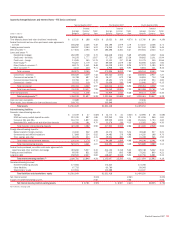

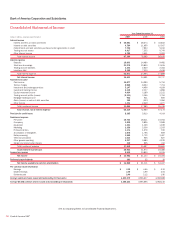

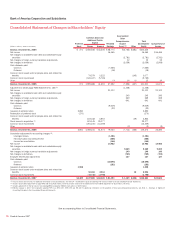

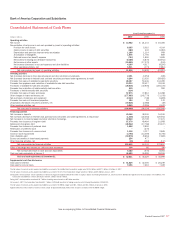

Bank of America Corporation and Subsidiaries

Notes to Consolidated Financial Statements

On October 1, 2007, Bank of America Corporation and its subsidiaries

(the Corporation) acquired all the outstanding shares of ABN AMRO North

America Holding Company, parent of LaSalle Bank Corporation (LaSalle),

for $21.0 billion in cash. On July 1, 2007, the Corporation acquired all the

outstanding shares of U.S. Trust Corporation for $3.3 billion in cash. On

January 1, 2006, the Corporation acquired 100 percent of the outstanding

stock of MBNA Corporation (MBNA). These mergers were accounted for

under the purchase method of accounting. Consequently, LaSalle, U.S.

Trust Corporation and MBNA’s results of operations were included in the

Corporation’s results from their dates of acquisition.

The Corporation, through its banking and nonbanking subsidiaries,

provides a diverse range of financial services and products throughout the

U.S. and in selected international markets. At December 31, 2007, the

Corporation operated its banking activities primarily under three charters:

Bank of America, National Association (Bank of America, N.A.), FIA Card

Services, N.A. and LaSalle Bank, N.A. Bank of America, N.A. was the sur-

viving entity after the merger with Fleet National Bank on June 13, 2005.

Effective June 10, 2006, MBNA America Bank N.A. was renamed FIA Card

Services, N.A., and on October 20, 2006, Bank of America, N.A. (USA)

merged into FIA Card Services, N.A. These mergers had no impact on the

Consolidated Financial Statements of the Corporation. LaSalle Bank, N.A.

was acquired in connection with the LaSalle acquisition.

Note 1 – Summary of Significant Accounting

Principles

Principles of Consolidation and Basis of Presentation

The Consolidated Financial Statements include the accounts of the Corpo-

ration and its majority-owned subsidiaries, and those variable interest enti-

ties (VIEs) where the Corporation is the primary beneficiary. All significant

intercompany accounts and transactions have been eliminated. Results of

operations of companies purchased are included from the dates of acquis-

ition and for VIEs, from the dates that the Corporation became the primary

beneficiary. Assets held in an agency or fiduciary capacity are not included

in the Consolidated Financial Statements. The Corporation accounts for

investments in companies for which it owns a voting interest of 20 percent

to 50 percent and for which it has the ability to exercise significant influ-

ence over operating and financing decisions using the equity method of

accounting. These investments are included in other assets and the

Corporation’s proportionate share of income or loss is included in equity

investment income.

The preparation of the Consolidated Financial Statements in con-

formity with accounting principles generally accepted in the United States

(GAAP) requires management to make estimates and assumptions that

affect reported amounts and disclosures. Actual results could differ from

those estimates and assumptions.

In 2007, the Corporation changed its basis of presentation for its

business segments. For additional information on the Corporation’s busi-

ness segments see Note 22 – Business Segment Information to the

Consolidated Financial Statements. Also in 2007, the Corporation

changed the current and historical presentation of its Consolidated State-

ment of Income to present gains (losses) on sales of debt securities as a

component of noninterest income.

Certain prior period amounts have been reclassified to conform to

current period presentation.

Recently Issued Accounting Pronouncements

On December 4, 2007, the Financial Accounting Standards Board (FASB)

issued Statement of Financial Accounting Standards (SFAS) No. 141

(revised 2007), “Business Combinations” (SFAS 141R). SFAS 141R modi-

fies the accounting for business combinations and requires, with limited

exceptions, the acquirer in a business combination to recognize 100 per-

cent of the assets acquired, liabilities assumed, and any noncontrolling

interest in the acquiree at the acquisition-date fair value. In addition, SFAS

141R requires the expensing of acquisition-related transaction and

restructuring costs, and certain contingent assets and liabilities acquired,

as well as contingent consideration, to be recognized at fair value. SFAS

141R also modifies the accounting for certain acquired income tax assets

and liabilities. SFAS 141R is effective for new acquisitions consummated

on or after January 1, 2009 and early adoption is not permitted.

On December 4, 2007, the FASB also issued SFAS No. 160,

“Noncontrolling Interests in Consolidated Financial Statements” (SFAS

160). SFAS 160 requires all entities to report noncontrolling (i.e., minority)

interests in subsidiaries as equity in the Consolidated Financial State-

ments and to account for transactions between an entity and non-

controlling owners as equity transactions if the parent retains its

controlling financial interest in the subsidiary. SFAS 160 also requires

expanded disclosure that distinguishes between the interests of the con-

trolling owners and the interests of the noncontrolling owners of a sub-

sidiary. SFAS 160 is effective for the Corporation’s financial statements

for the year beginning on January 1, 2009 and earlier adoption is not

permitted. The adoption of SFAS 160 is not expected to have a material

impact on the Corporation’s financial condition and results of operations.

On November 5, 2007, the Securities and Exchange Commission (SEC)

issued Staff Accounting Bulletin (SAB) No. 109, “Written Loan Commitments

Recorded at Fair Value Through Earnings” (SAB 109). SAB 109 requires that

the expected net future cash flows related to servicing of a loan be included

in the measurement of all written loan commitments that are accounted for at

fair value through earnings. The adoption of SAB 109 is on a prospective

basis and effective for the Corporation’s loan commitments measured at fair

value through earnings which are issued or modified after January 1, 2008.

The adoption of SAB 109 will not have a material impact on the Corporation’s

financial condition and results of operations.

On June 27, 2007, the FASB ratified the Emerging Issues Task Force

(EITF) consensus on Issue No. 06-11, “Accounting for Income Tax Benefits

of Dividends on Share-Based Payment Awards” (EITF 06-11). Effective

January 1, 2008, EITF 06-11 requires on a prospective basis that the tax

benefit related to dividend equivalents paid on restricted stock and

restricted stock units which are expected to vest be recorded as an

increase to additional paid-in capital. Prior to January 1, 2008, the Corpo-

118

Bank of America 2007