Bank of America 2007 Annual Report Download - page 90

Download and view the complete annual report

Please find page 90 of the 2007 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

|

|

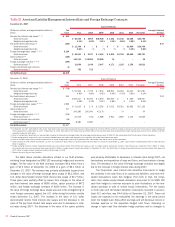

Histogram of Daily Trading-Related Revenue

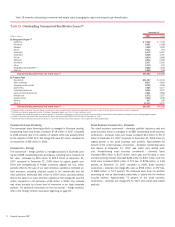

Twelve Months Ended December 31, 2007

0

10

20

30

40

50

60

70

< -50 -50 to -40 -40 to -30 -30 to -20 -20 to -10 -10 to 0 0 to 10 10 to 20 20 to 30 30 to 40 40 to 50 > 50

Revenue (dollars in millions)

Number of Days

The histogram of daily revenue or loss above is a graphic depiction of

trading volatility and illustrates the daily level of trading-related revenue for

the twelve months ended December 31, 2007. During the twelve months

ended December 31, 2007, positive trading-related revenue was recorded

for 71 percent of the trading days. During the second half of 2007, CDO-

related markets experienced significant liquidity constraints impacting the

availability and reliability of transparent pricing resulting in the valuation of

CDOs becoming more complex and time consuming. Accordingly, it was

not possible to mark these positions to market on a daily basis. As a

result, we recorded valuation adjustments in trading account profits

(losses) of approximately $4.0 billion on certain discrete dates relating to

our super senior CDO exposure. For further discussion of our super senior

CDO exposure and related losses see page 53. Excluding the discrete

writedowns on our super senior CDO exposure, 21 percent of the total

trading days had losses greater than $10 million, and the largest loss was

$159 million. This can be compared to the twelve months ended

December 31, 2006, where positive trading-related revenue was recorded

for 96 percent of the trading days and there were no losses greater than

$10 million, and the largest loss was $10 million. The increase in the

total trading days with losses greater than $10 million was due to the

period of market disruption during the second half of 2007.

To evaluate risk in our trading activities, we focus on the actual and

potential volatility of individual positions as well as portfolios. VAR is a key

statistic used to measure market risk. In order to manage day-to-day risks,

VAR is subject to trading limits both for our overall trading portfolio and

within individual businesses. All limit excesses are communicated to

management for review.

A VAR model simulates the value of a portfolio under a range of hypo-

thetical scenarios in order to generate a distribution of potential gains and

losses. The VAR represents the worst loss the portfolio is expected to

experience based on historical trends with a given level of confidence. VAR

depends on the volatility of the positions in the portfolio and on how

strongly their risks are correlated. Within any VAR model, there are sig-

nificant and numerous assumptions that will differ from company to com-

pany. In addition, the accuracy of a VAR model depends on the availability

and quality of historical data for each of the positions in the portfolio. A

VAR model may require additional modeling assumptions for new products

which do not have extensive historical price data, or for illiquid positions

for which accurate daily prices are not consistently available. Our VAR

model uses a historical simulation approach based on three years of his-

torical data and assumes a 99 percent confidence level. Statistically, this

means that losses will exceed VAR, on average, one out of 100 trading

days, or two to three times each year.

A VAR model is an effective tool in estimating ranges of potential

gains and losses on our trading portfolios. There are however many limi-

tations inherent in a VAR model as it utilizes historical results over a

defined time period to estimate future performance. Historical results may

not always be indicative of future results and changes in market con-

ditions or in the composition of the underlying portfolio could have a mate-

rial impact on the accuracy of the VAR model. This was of particular

relevance in the last part of 2007 when markets experienced a period of

extreme illiquidity resulting in losses that were far outside of the normal

loss forecasts by VAR models. Due to these limitations, we have histor-

ically used the VAR model as only one of the components in managing our

trading risk and also use other techniques such as stress testing and

desk level limits. Periods of extreme market stress influence the reliability

of these techniques to various degrees. See discussion on stress testing

on the following page.

On a quarterly basis, the accuracy of the VAR methodology is

reviewed by backtesting (i.e., comparing actual results against expect-

ations derived from historical data) the VAR results against the daily profit

and loss. Graphic representation of the backtesting results with additional

explanation of backtesting excesses are reported to the GRC. Backtesting

excesses occur when trading losses exceed the VAR. Senior management

reviews and evaluates the results of these tests.

88

Bank of America 2007