Bank of America 2007 Annual Report Download - page 49

Download and view the complete annual report

Please find page 49 of the 2007 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

|

|

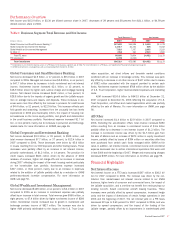

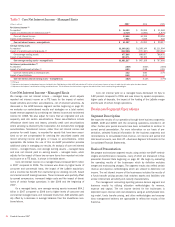

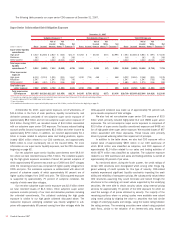

December 31 Average Balance

(Dollars in millions) 2007 2006 2007 2006

Total loans and leases

$359,946

$307,661

$327,810

$288,131

Total earning assets

(1)

383,384

343,338

353,591

344,013

Total assets

(1)

442,987

399,373

408,034

396,559

Total deposits

344,850

329,195

328,918

332,242

(1) Total earning assets and total assets include asset allocations to match liabilities (i.e., deposits).

The strategy for GCSBB is to attract, retain and deepen customer

relationships. We achieve this strategy through our ability to offer a wide

range of products and services through a franchise that stretches coast to

coast through 32 states and the District of Columbia. We also provide

credit card products to customers in Canada, Ireland, Spain and the

United Kingdom. In the U.S., we serve approximately 59 million consumer

and small business relationships utilizing our network of 6,149 banking

centers, 18,753 domestic branded ATMs, and telephone and Internet

channels. Within GCSBB, there are three primary businesses: Deposits,

Card Services, and Consumer Real Estate. In addition, ALM/Other

includes the results of ALM activities and other consumer-related busi-

nesses (e.g., insurance). GCSBB, specifically Card Services, is presented

on a managed basis. For a reconciliation of managed GCSBB to held

GCSBB, see Note 22 – Business Segment Information to the Consolidated

Financial Statements.

During 2007, Visa Inc. filed a registration statement with the SEC

with respect to a proposed IPO. Subject to market conditions and other

factors, Visa Inc. expects the IPO to occur in the first half of 2008. We

expect to record a gain associated with the IPO. In addition, we expect

that a portion of the proceeds from the IPO will be used by Visa Inc. to

fund liabilities arising from litigation which would allow us to record an

offset to the litigation liabilities that we recorded in the fourth quarter of

2007 as discussed below.

Net income decreased $1.9 billion, or 17 percent, to $9.4 billion

compared to 2006 as increases in noninterest income and net interest

income were more than offset by increases in provision for credit losses

and noninterest expense.

Net interest income increased $612 million, or two percent, to $28.8

billion due to the impacts of organic growth and the LaSalle acquisition on

average loans and leases, and deposits compared to 2006. Noninterest

income increased $2.1 billion, or 13 percent, to $18.9 billion compared to

the same period in 2006, mainly due to increases in card income, service

charges and mortgage banking income.

Provision for credit losses increased $4.4 billion, or 51 percent, to

$12.9 billion compared to 2006. This increase primarily resulted from a

$3.2 billion increase in Card Services and a $978 million increase in

Consumer Real Estate. For further discussion of the increase in provision

for credit losses related to Card Services and Consumer Real Estate, see

their respective discussions.

Noninterest expense increased $1.7 billion, or nine percent, to

$20.1 billion largely due to increases in personnel-related expenses, Visa-

related litigation costs, equally allocated to Card Services and Treasury

Services on a management accounting basis, and technology related

costs. For additional information on Visa-related litigation, see Note 13 –

Commitments and Contingencies to the Consolidated Financial

Statements.

Deposits

Deposits provides a comprehensive range of products to consumers and

small businesses. Our products include traditional savings accounts,

money market savings accounts, CDs and IRAs, and noninterest and

interest-bearing checking accounts. Debit card results are also included in

Deposits.

Deposit products provide a relatively stable source of funding and

liquidity. We earn net interest spread revenues from investing this liquidity

in earning assets through client-facing lending activity and our ALM activ-

ities. The revenue is allocated to the deposit products using our funds

transfer pricing process which takes into account the interest rates and

maturity characteristics of the deposits. Deposits also generate fees such

as account service fees, non-sufficient fund fees, overdraft charges and

ATM fees, while debit cards generate merchant interchange fees based on

purchase volume.

Excluding accounts obtained through acquisitions, we added approx-

imately 2.3 million net new retail checking accounts in 2007. These addi-

tions resulted from continued improvement in sales and service results in

the Banking Center Channel and Online, and the success of such products

as Keep the Change

TM

, Risk Free CDs, Balance Rewards and Affinity.

We continue to migrate qualifying affluent customers and their

related deposit balances from GCSBB to GWIM. In 2007, a total of $11.4

billion of deposits were migrated from GCSBB to GWIM compared to $10.7

billion in 2006. After migration, the associated net interest income, serv-

ice charges and noninterest expense are recorded in GWIM.

Net income increased $364 million, or seven percent, to $5.2 billion

compared to 2006 as an increase in noninterest income was partially

offset by an increase in noninterest expense. Net interest income

remained relatively flat at $9.4 billion compared to 2006 as the addition

of LaSalle and higher deposit spreads resulting from disciplined pricing

were offset by the impact of lower balances. Average deposits decreased

$3.2 billion, or one percent, largely due to the migration of customer rela-

tionships and related balances to GWIM, partially offset by the acquisition

of LaSalle. The increase in noninterest income was driven by higher serv-

ice charges of $665 million, or 12 percent, primarily as a result of new

demand deposit account growth and the addition of LaSalle. Additionally,

debit card revenue growth of $248 million, or 13 percent, was due to a

higher number of checking accounts, increased usage, the addition of

LaSalle and market penetration (i.e., increase in the number of existing

account holders with debit cards).

Noninterest expense increased $323 million, or four percent, to $9.1

billion compared to 2006, primarily due to the addition of LaSalle, and to

higher account and transaction volumes.

Card Services

Card Services, which excludes the results of debit cards (included in

Deposits), provides a broad offering of products, including U.S. Consumer

and Business Card, Unsecured Lending, and International Card. We offer a

variety of co-branded and affinity credit card products and have become

the leading issuer of credit cards through endorsed marketing in the U.S.

and Europe. During 2007, Merchant Services was transferred to Treasury

Services within GCIB. Previously their results were reported in Card Serv-

ices. Prior period amounts have been reclassified.

Bank of America 2007

47