Bank of America 2007 Annual Report Download - page 50

Download and view the complete annual report

Please find page 50 of the 2007 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

|

|

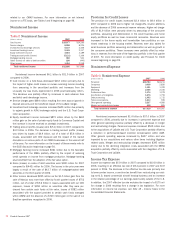

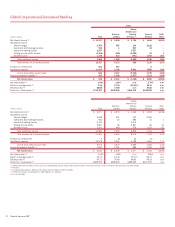

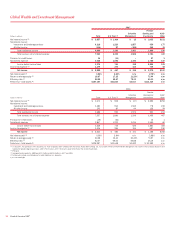

The Corporation reports its GCSBB results, specifically Card Services,

on a managed basis, which is consistent with the way that management

evaluates the results of GCSBB. Managed basis assumes that securitized

loans were not sold and presents earnings on these loans in a manner

similar to the way loans that have not been sold (i.e., held loans) are

presented. Loan securitization is an alternative funding process that is

used by the Corporation to diversify funding sources. Loan securitization

removes loans from the Consolidated Balance Sheet through the sale of

loans to an off-balance sheet QSPE which is excluded from the Corpo-

ration’s Consolidated Financial Statements in accordance with GAAP.

Securitized loans continue to be serviced by the business and are

subject to the same underwriting standards and ongoing monitoring as

held loans. In addition, excess servicing income is exposed to similar

credit risk and repricing of interest rates as held loans.

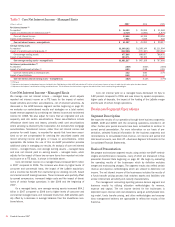

Net income decreased $2.0 billion, or 35 percent, to $3.7 billion

compared to 2006 as growth in noninterest income and net interest

income was more than offset by higher provision for credit losses and

noninterest expense. Net interest income increased $205 million, or one

percent, to $16.6 billion as an increase in managed average loans and

leases of $18.5 billion was partially offset by spread compression.

Noninterest income increased $692 million, or eight percent, to $9.0

billion mainly due to higher cash advance fees related to organic loan

growth in domestic credit card and unsecured lending. All other income

increased $124 million primarily due to higher foreign revenues.

Provision for credit losses increased $3.2 billion, or 40 percent, to

$11.3 billion compared to 2006. The increase was primarily driven by

higher managed net losses from portfolio seasoning and increases from

unusually low loss levels experienced in 2006 post bankruptcy reform. The

higher provision was also driven by reserve increases in our small busi-

ness portfolio reflective of growth in the business and portfolio deterio-

ration. In addition, higher provision was due to seasoning of the unsecured

lending portfolio. These increases in provision were partially offset by a

higher level of reserve reduction from the addition of higher loss profile

accounts to the domestic credit card securitization trust.

Noninterest expense increased $775 million, or 10 percent, to $8.3

billion compared to 2006, largely due to increases in personnel-related

expenses, Card Services’ allocation of the Visa-related litigation costs and

technology related costs. For additional information on Visa-related liti-

gation, see Note 13 – Commitments and Contingencies to the Con-

solidated Financial Statements.

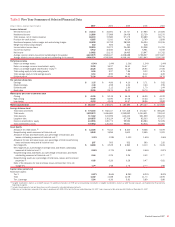

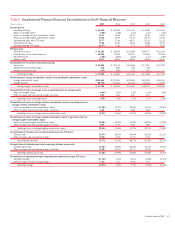

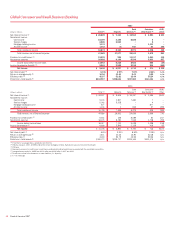

Key Statistics

(Dollars in millions) 2007 2006

Card Services

Average – total loans and leases:

Managed

$209,774

$191,314

Held

106,490

95,076

Period end – total loans and leases:

Managed

227,822

203,151

Held

124,855

101,286

Managed net losses

(1)

:

Amount

10,099

7,236

Percent

4.81%

3.78%

Credit Card (2)

Average – total loans and leases:

Managed

$171,376

$163,409

Held

70,242

72,979

Period end – total loans and leases:

Managed

183,691

170,489

Held

80,724

72,194

Managed net losses

(1)

:

Amount

8,214

6,375

Percent

4.79%

3.90%

(1) Represents net charge-offs on held loans combined with realized credit losses associated with the

securitized loan portfolio.

(2) Includes U.S. consumer card and foreign credit card. Does not include business card and unsecured

lending.

The table above and the discussion below presents select key

indicators for the Card Services and credit card portfolios.

Managed Card Services net losses increased $2.9 billion to $10.1

billion, or 4.81 percent of average outstandings, compared to $7.2 billion,

or 3.78 percent (3.93 percent excluding the impact of SOP 03-3) in 2006.

This increase was primarily driven by portfolio seasoning and increases

from the unusually low loss levels experienced in 2006 post bankruptcy

reform.

Managed Card Services total average loans and leases increased

$18.5 billion to $209.8 billion compared to the same period in 2006,

driven by growth in the unsecured lending, foreign and domestic card port-

folios.

Managed credit card net losses increased $1.8 billion to $8.2 billion,

or 4.79 percent of average credit card outstandings, compared to $6.4

billion, or 3.90 percent (3.99 percent excluding the impact of SOP 03-3) in

2006. The increase was driven by portfolio seasoning and increases from

the unusually low loss levels experienced in 2006 post bankruptcy reform.

Managed credit card total average loans and leases increased $8.0

billion to $171.4 billion compared to the same period in 2006. The

increase was driven by growth in the foreign and domestic portfolios.

For more information on credit quality, see Consumer Portfolio Credit

Risk Management beginning on page 70.

48

Bank of America 2007