Bank of America 2007 Annual Report Download - page 75

Download and view the complete annual report

Please find page 75 of the 2007 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

|

|

SOP 03-3

SOP 03-3 addresses accounting for differences between contractual cash

flows and cash flows expected to be collected from an investor’s initial

investment in loans acquired in a transfer if those differences are attribut-

able, at least in part, to credit quality. SOP 03-3 requires that impaired

loans be recorded at fair value and prohibits “carrying over” or the creation

of valuation allowances in the initial accounting of loans acquired in a

transfer that are within the scope of this SOP (categories of loans for

which it is probable, at the time of acquisition, that all amounts due

according to the contractual terms of the loan agreement will not be

collected). The prohibition of the valuation allowance carryover applies to

the purchase of an individual loan, a pool of loans, a group of loans, and

loans acquired in a purchase business combination.

In accordance with SOP 03-3, certain acquired loans of LaSalle in

2007 and MBNA in 2006 that were considered impaired were written

down to fair value at the acquisition date. Therefore, reported net charge-

offs and managed net losses were lower since these impaired loans that

would have been charged off during the period were reduced to fair value

as of the acquisition date. SOP 03-3 does not apply to the acquired loans

that have been securitized as they are not held on the Corporation’s Bal-

ance Sheet.

Consumer net charge-offs, managed net losses, and associated

ratios excluding the impact of SOP 03-3 for 2007 and 2006 are presented

in Table 14. Management believes that excluding the impact of SOP 03-3

provides a more accurate reflection of portfolio credit quality.

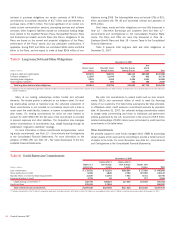

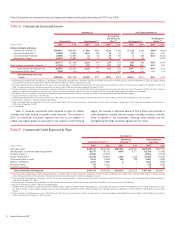

Table 14 Consumer Net Charge-offs/Managed Net Losses (Excluding the Impact of SOP 03-3) (1, 2, 3, 4)

Held Managed

Net Charge-offs Ratio Net Losses Ratio

(Dollars in millions) 2007 2006 2007 2006 2007 2006 2007 2006

Residential mortgage

$59

$39

0.02 %

0.02 %

$59

$39

0.02 %

0.02 %

Credit card – domestic

3,063

3,193

5.29

5.00

6,960

5,494

4.91

3.96

Credit card – foreign

378

278

3.06

3.05

1,254

1,033

4.24

4.17

Home equity

282

51

0.29

0.07

282

51

0.29

0.07

Direct/Indirect consumer

1,375

729

1.96

1.36

1,605

1,044

2.14

1.69

Other consumer

278

217

6.54

2.97

278

217

6.54

2.97

Total consumer

$5,435

$4,507

1.07

1.07

$10,438

$7,878

1.69

1.50

(1) Excluding the impact of SOP 03-3 is a non-GAAP financial measure. The impact of SOP 03-3 on average outstanding held and managed consumer loans and leases in 2007 and 2006 was not material.

(2) Net charge-off/loss ratios are calculated as held net charge-offs or managed net losses divided by average outstanding held or managed loans and leases during the year for each loan and lease category.

(3) Historical ratios have been adjusted for home equity, direct/indirect consumer and other consumer due to the reclassification of home equity loan balances from direct/indirect consumer to home equity, and certain foreign

consumer loans from other consumer to direct/indirect consumer.

(4) Including the impact of SOP 03-3 would decrease net charge-offs on residential mortgage $2 million, home equity $8 million, direct/indirect consumer $2 million in 2007. Including the impact of SOP 03-3 would decrease net

charge-offs on credit card – domestic $99 million, credit card – foreign $53 million and direct/indirect consumer $119 million in 2006.

Bank of America 2007

73