Bank of America 2007 Annual Report Download - page 138

Download and view the complete annual report

Please find page 138 of the 2007 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

|

|

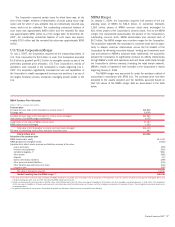

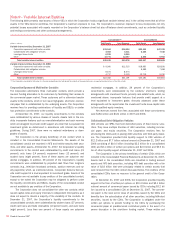

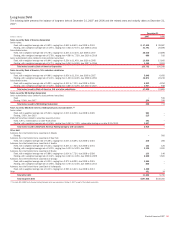

Credit Card and Other Securitizations

The Corporation maintains interests in credit card, other consumer, and

commercial loan securitization vehicles. These acquired interests include

interest-only strips, subordinated tranches, cash reserve accounts, and

subordinated interests in accrued interest and fees on the securitized

receivables. During 2007 and 2006, the Corporation securitized $19.9

billion and $23.7 billion of credit card receivables resulting in $99 million

and $104 million in gains (net of securitization transaction costs of $14

million and $28 million) which were recorded in card income. As of

December 31, 2007 and 2006, the aggregate debt securities outstanding

for the Corporation’s credit card securitization trusts were $101.3 billion

and $96.8 billion.

The Corporation also securitized $3.3 billion of automobile loans and

recorded losses of $6 million in 2006. The Corporation did not securitize

any automobile loans in 2007. At December 31, 2007 and 2006,

aggregate debt securities outstanding for the Corporation’s automobile

securitization vehicles were $2.6 billion and $5.2 billion, and the Corpo-

ration held residual interests which totaled $100 million and $130 million.

At December 31, 2007 and 2006, the remaining other consumer and

commercial loan securitization vehicles were not material to the Corpo-

ration.

At December 31, 2007 and 2006, the Corporation held investment

grade securities issued by its securitization vehicles of $2.1 billion ($425

million of which were issued in 2007) and $3.5 billion (none of which were

issued in 2006) in the AFS debt securities portfolio which are valued using

quoted market prices. At December 31, 2007 and 2006, there were no

recognized servicing assets or liabilities associated with any of these

credit card and other securitization transactions.

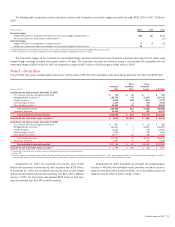

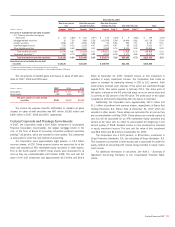

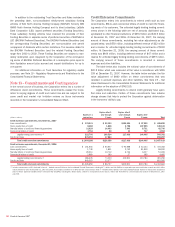

Key economic assumptions used in measuring the fair value of cer-

tain residual interests that continue to be held by the Corporation

(included in other assets) in credit card securitizations and the sensitivity

of the current fair value of residual cash flows to changes in those

assumptions are disclosed in the table below.

The sensitivities in the table below are hypothetical and should be

used with caution. As the amounts indicate, changes in fair value

based on variations in assumptions generally cannot be extrapolated

because the relationship of the change in assumption to the change in fair

value may not be linear. Also, the effect of a variation in a particular

assumption on the fair value of an interest that continues to be held by

the Corporation is calculated without changing any other assumption. In

reality, changes in one factor may result in changes in another, which

might magnify or counteract the sensitivities. Additionally, the Corporation

has the ability to hedge interest rate risk associated with retained residual

positions. The above sensitivities do not reflect any hedge strategies that

may be undertaken to mitigate such risk.

Principal proceeds from collections reinvested in revolving credit card

securitizations were $178.6 billion and $163.4 billion in 2007 and 2006.

Contractual credit card servicing fee income totaled $2.1 billion and $1.9

billion in 2007 and 2006. Other cash flows received on retained interests,

such as cash flow from interest-only strips, were $6.6 billion and $6.7 bil-

lion in 2007 and 2006, for credit card securitizations. Proceeds from col-

lections reinvested in revolving commercial loan securitizations were $2.9

billion and $4.6 billion in 2007 and 2006. Servicing fees and other cash

flows received on retained interests, such as cash flows from interest-only

strips, were $1 million and $9 million in 2007, and $2 million and $15

million in 2006 for commercial loan securitizations.

The Corporation also reviews its loans and leases portfolio on a

managed basis. Managed loans and leases are defined as on-balance

sheet loans and leases as well as those loans in revolving securitizations

and other securitizations where servicing is retained that are undertaken

for corporate management purposes, which include credit card, commer-

cial loans, automobile and certain mortgage securitizations. Managed

loans and leases exclude originate-to-distribute loans and other loans in

securitizations where the Corporation has not retained servicing. New

advances on accounts for which previous loan balances were sold to the

securitization trusts will be recorded on the Corporation’s Consolidated

Balance Sheet after the revolving period of the securitization, which has

the effect of increasing loans and leases on the Corporation’s Con-

solidated Balance Sheet and increasing net interest income and charge-

offs, with a related reduction in noninterest income.

(Dollars in millions) 2007 2006

Carrying amount of residual interests (at fair value) (1)

$ 2,766

$ 2,929

Balance of unamortized securitized loans

102,967

98,295

Weighted average life to call or maturity (in years)

0.3

0.3

Monthly payment rate

11.6-16.6%

11.2-19.8%

Impact on fair value of 10% favorable change

$51

$43

Impact on fair value of 25% favorable change

158

133

Impact on fair value of 10% adverse change

(35)

(38)

Impact on fair value of 25% adverse change

(80)

(82)

Expected credit losses (annual rate)

3.7-5.4%

3.8-5.8%

Impact on fair value of 10% favorable change

$ 141

$86

Impact on fair value of 25% favorable change

374

218

Impact on fair value of 10% adverse change

(133)

(85)

Impact on fair value of 25% adverse change

(333)

(211)

Residual cash flows discount rate (annual rate)

11.5%

12.5%

Impact on fair value of 100 bps favorable change

$9

$12

Impact on fair value of 200 bps favorable change

13

17

Impact on fair value of 100 bps adverse change

(12)

(14)

Impact on fair value of 200 bps adverse change

(23)

(27)

(1) Residual interests include interest-only strips, subordinated tranches, subordinated interests in accrued interest and fees on the securitized receivables and cash reserve accounts which are carried at fair value or amounts

that approximate fair value.

136

Bank of America 2007