Bank of America 2007 Annual Report Download - page 91

Download and view the complete annual report

Please find page 91 of the 2007 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

|

|

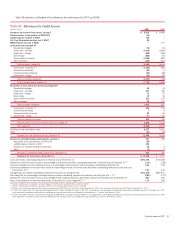

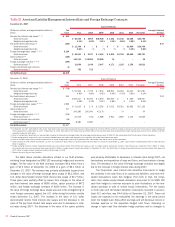

Trading Risk and Return

Daily Trading-Related Revenue and VAR

Daily Trading-

Related

Revenue

VA R

-200

-150

-100

-50

0

50

100

12/31/2006 3/31/2007 6/30/2007 9/30/2007 12/31/2007

(Dollars in millions)

The graph above shows daily trading-related revenue and VAR exclud-

ing the discrete writedowns on our super senior CDO exposure for the

twelve months ended December 31, 2007. Excluding these writedowns,

actual losses exceeded daily trading VAR fourteen times in the twelve

months ended December 31, 2007 and losses did not exceed daily trad-

ing VAR in the twelve months ended December 31, 2006. The losses that

exceeded daily trading VAR for the twelve months ended December 31,

2007, occurred during the market disruption which took place during the

second half of 2007. The sudden increase in market volatility during this

period produced a large number of price changes that exceeded the 99

th

percentile of the three year history used for our VAR calculations.

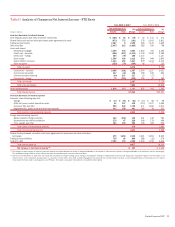

Table 28 presents average, high and low daily trading VAR for the

twelve months ended December 31, 2007 and 2006.

The increase in average VAR from 2006 was driven by the increased

market volatility during the second half of 2007. In particular, with the

dislocation in structured and credit products, many credit spreads used in

the calculation of VAR increased by unprecedented amounts. In addition,

many trading assets became extremely illiquid which required changes in

assumptions to properly incorporate them in the VAR model as was the

case with our CDO exposure for which we have updated our model at vari-

ous times during the second half of 2007. In periods of stress, the GRC

members communicate daily to discuss losses, VAR limit excesses and

the impact to regulatory capital. As a result of this process, the lines of

business may selectively reduce risk. Where economically feasible, posi-

tions are sold or macro economic hedges are executed to reduce the

exposure.

Stress Testing

Because the very nature of a VAR model suggests results can exceed our

estimates, we also “stress test” our portfolio. Stress testing estimates

the value change in our trading portfolio that may result from abnormal

market movements. Various types of stress tests are run regularly against

the overall trading portfolio and individual businesses. Historical scenarios

simulate the impact of price changes which occurred during a set of

extended historical market events. The results of these scenarios are

reported daily to management. During the twelve months ended

December 31, 2007, the largest daily losses among these scenarios

ranged from $9 million to $529 million.

Table 28 Trading Activities Market Risk (1)

Twelve Months Ended December 31

2007 2006

VAR VAR

(Dollars in millions) Average High

(2)

Low

(2)

Average High

(2)

Low

(2)

Foreign exchange

$ 7.2 $25.3 $ 3.8

$ 8.2 $22.9 $ 3.1

Interest rate

13.9 31.9 6.6

18.5 50.0 7.3

Credit

39.5 69.9 23.4

26.8 36.7 18.4

Real estate/mortgage

14.1 23.5 5.7

8.4 12.7 4.7

Equities

24.6 45.8 9.6

18.8 39.6 9.9

Commodities

7.2 10.7 3.7

6.1 9.9 3.4

Portfolio diversification

(53.9) – –

(45.5) – –

Total market-based trading portfolio (3)

$ 52.6 $91.5 $32.9

$ 41.3 $59.8 $26.0

(1) Excludes our discrete writedowns on super senior CDO exposure. For more information on the CDO writedowns and the impact of the market disruption on the Corporation’s results, see the CDO discussion beginning on page

53.

(2) The high and low for the total portfolio may not equal the sum of the individual components as the highs or lows of the individual portfolios may have occurred on different trading days.

(3) For a discussion of the VAR related to the credit derivatives that economically hedge the loan portfolio, see Industry Concentrations beginning on page 79. The table above does not include credit protection purchased to

manage our counterparty credit risk. During the three months ended December 31, 2007, the average VAR of this protection was $9 million.

Bank of America 2007

89