Bank of America 2007 Annual Report Download - page 69

Download and view the complete annual report

Please find page 69 of the 2007 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

|

|

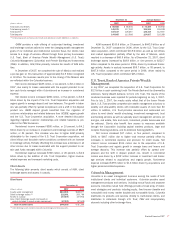

Our borrowing costs and ability to raise funds are directly impacted by our credit ratings. The credit ratings of Bank of America Corporation and Bank of

America, N.A. are reflected in the table below.

Table 11 Credit Ratings

December 31, 2007

Bank of America Corporation Bank of America, N.A.

Senior Debt

Subordinated

Debt

Commercial

Paper

Short-term

Borrowings

Long-term

Debt

Moody’s Investors Service Aa1 Aa2 P-1 P-1 Aaa

Standard & Poor’s AA AA- A-1+ A-1+ AA+

Fitch Ratings AA AA- F1+ F1+ AA

Under normal business conditions, primary sources of funding for the

parent company include dividends received from its banking and non-

banking subsidiaries, and proceeds from the issuance of senior and sub-

ordinated debt, as well as commercial paper and equity. Primary uses of

funds for the parent company include repayment of maturing debt and

commercial paper, share repurchases, dividends paid to shareholders,

and subsidiary funding through capital or debt.

The parent company maintains a cushion of excess liquidity that

would be sufficient to fully fund the holding company and nonbank affiliate

operations for an extended period during which funding from normal sour-

ces is disrupted. The primary measure used to assess the parent compa-

ny’s liquidity is the “Time to Required Funding” during such a period of

liquidity disruption. This measure assumes that the parent company is

unable to generate funds from debt or equity issuance, receives no divi-

dend income from subsidiaries, and no longer pays dividends to share-

holders while continuing to meet nondiscretionary uses needed to

maintain bank operations and repayment of contractual principal and

interest payments owed by the parent company and affiliated companies.

Under this scenario, the amount of time the parent company and its non-

bank subsidiaries can operate and meet all obligations before the current

liquid assets are exhausted is considered the “Time to Required Funding.”

ALCO approves the target range set for this metric, in months, and mon-

itors adherence to the target. Maintaining excess parent company cash

ensures that “Time to Required Funding” remains in the target range of 21

to 27 months and is the primary driver of the timing and amount of the

Corporation’s debt issuances. As of December 31, 2007 “Time to

Required Funding” was 19 months compared to 24 months at

December 31, 2006. The reduction reflects the funding of the LaSalle

acquisition for $21.0 billion in cash which closed on October 1, 2007. We

had anticipated in the fourth quarter of 2007 that the “Time to Required

Funding” would decrease slightly below our target range as a result of the

funding of the LaSalle acquisition. We anticipate returning to our target

range in 2008 due in part to the issuance of preferred stock in the first

quarter of 2008. For additional information on our recent preferred stock

issuances, see the Preferred Stock discussion on page 69.

The primary sources of funding for our banking subsidiaries include

customer deposits and wholesale market–based funding. Primary uses of

funds for the banking subsidiaries include growth in the core asset portfo-

lios, including loan demand, and in the ALM portfolio. We use the ALM

portfolio primarily to manage interest rate risk and liquidity risk.

One ratio that can be used to monitor the stability of funding composi-

tion is the “loan to domestic deposit” ratio. This ratio reflects the percent

of loans and leases that are funded by domestic core deposits, a relatively

stable funding source. A ratio below 100 percent indicates that our loan

portfolio is completely funded by domestic core deposits. The ratio was

127 percent at December 31, 2007 compared to 118 percent at

December 31, 2006. The increase was primarily attributable to organic

growth in the loan and lease portfolio, and a decision to retain a larger

share of mortgage production on the Corporation’s balance sheet.

The strength of our balance sheet is a result of rigorous financial and

risk discipline. Our core deposit base, which is a low cost funding source,

is often used to fund the purchase of incremental assets (primarily loans

and securities), the composition of which impacts our loan to deposit

ratio. Mortgage-backed securities and mortgage loans have prepayment

risk which must be managed. Repricing of deposits is a key variable in this

process. The capital generated in excess of capital adequacy targets and

to support business growth, is available for the payment of dividends and

share repurchases.

ALCO determines prudent parameters for wholesale market-based

borrowing and regularly reviews the funding plan for the bank subsidiaries

to ensure compliance with these parameters. The contingency funding

plan for the banking subsidiaries evaluates liquidity over a 12-month

period in a variety of business environment scenarios assuming different

levels of earnings performance and credit ratings as well as public and

investor relations factors. Funding exposure related to our role as liquidity

provider to certain off-balance sheet financing entities is also measured

under a stress scenario. In this analysis, ratings are downgraded such that

the off-balance sheet financing entities are not able to issue commercial

paper and backup facilities that we provide are drawn upon. In addition,

potential draws on credit facilities to issuers with ratings below a certain

level are analyzed to assess potential funding exposure.

We originate loans for retention on our balance sheet and for dis-

tribution. As part of our “originate to distribute” strategy, commercial loan

originations are distributed through syndication structures, and residential

mortgages originated by Consumer Real Estate are frequently distributed

in the secondary market. In connection with our balance sheet manage-

ment activities, we may retain mortgage loans originated as well as pur-

chase and sell loans based on our assessment of market conditions.

Regulatory Capital

At December 31, 2007, the Corporation operated its banking activities

primarily under three charters: Bank of America, N.A., FIA Card Services,

N.A. and LaSalle Bank, N.A. As a regulated financial services company, we

are governed by certain regulatory capital requirements. At December 31,

2007 and 2006, the Corporation, Bank of America, N.A., and FIA Card

Services, N.A., were classified as “well-capitalized” for regulatory pur-

poses, the highest classification. At December 31, 2007, LaSalle Bank,

N.A. was also classified as “well-capitalized” for regulatory purposes.

There have been no conditions or events since December 31, 2007 that

management believes have changed the Corporation’s, Bank of America,

N.A.’s, FIA Card Services, N.A.’s, and LaSalle Bank, N.A.’s capital classi-

fications.

Bank of America 2007

67