Bank of America 2007 Annual Report Download - page 92

Download and view the complete annual report

Please find page 92 of the 2007 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

|

|

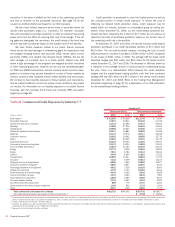

Hypothetical scenarios evaluate the potential impact of extreme but

plausible events over periods as long as one month. These scenarios are

developed to address perceived vulnerabilities in the market and in our

portfolios, and are periodically updated. They are also reviewed and

updated to reflect changing market conditions, such as were experienced

during the second half of 2007. For example, many trading assets became

extremely illiquid which required changes in assumptions to properly

incorporate them in the stress models. This was the case with our CDO-

related exposure for which we have updated our models at various times

during the second half of 2007. Management reviews and evaluates

results of these scenarios monthly. During the twelve months ended

December 31, 2007, the largest daily losses among these scenarios

ranged from $459 million to $1.5 billion. Worst-case losses, which repre-

sent the most extreme losses in our daily VAR calculation, are reported

daily. Finally, desk-level stress tests are performed daily for individual

businesses. These stress tests evaluate the potential adverse impact of

large moves in the market risk factors to which those businesses are

most sensitive.

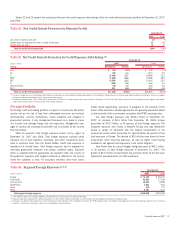

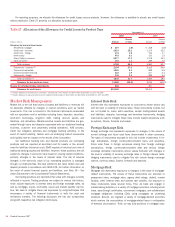

Interest Rate Risk Management for Nontrading

Activities

Interest rate risk represents the most significant market risk exposure to

our nontrading exposures. Our overall goal is to manage interest rate risk

so that movements in interest rates do not adversely affect core net inter-

est income – managed basis. Interest rate risk is measured as the poten-

tial volatility in our core net interest income – managed basis caused by

changes in market interest rates. Client facing activities, primarily lending

and deposit-taking, create interest rate sensitive positions on our balance

sheet. Interest rate risk from these activities, as well as the impact of

changing market conditions, is managed through our ALM activities.

Simulations are used to estimate the impact on core net interest

income – managed basis using numerous interest rate scenarios, balance

sheet trends and strategies. These simulations evaluate how the above

mentioned scenarios impact core net interest income – managed basis on

short-term financial instruments, debt securities, loans, deposits, borrow-

ings, and derivative instruments. In addition, these simulations

incorporate assumptions about balance sheet dynamics such as loan and

deposit growth and pricing, changes in funding mix, and asset and liability

repricing and maturity characteristics. These simulations do not include

the impact of hedge ineffectiveness.

Management analyzes core net interest income – managed basis

forecasts utilizing different rate scenarios, with the base case utilizing the

forward interest rates. Management frequently updates the core net inter-

est income – managed basis forecast for changing assumptions and differ-

ing outlooks based on economic trends and market conditions. Thus, we

continually monitor our balance sheet position in an effort to maintain an

acceptable level of exposure to interest rate changes.

We prepare forward-looking forecasts of core net interest income –

managed basis. These baseline forecasts take into consideration

expected future business growth, ALM positioning, and the direction of

interest rate movements as implied by forward interest rates. We then

measure and evaluate the impact that alternative interest rate scenarios

have to these static baseline forecasts in order to assess interest rate

sensitivity under varied conditions. The spot and 12-month forward

monthly rates used in our respective baseline forecasts at December 31,

2007 and 2006 are shown in Table 29.

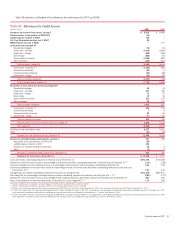

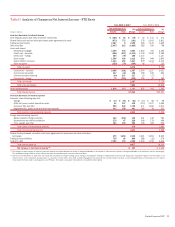

Table 30 reflects the pre-tax dollar impact to forecasted core net

interest income – managed basis over the next twelve months from

December 31, 2007 and 2006, resulting from a 100 bp gradual parallel

increase, a 100 bp gradual parallel decrease, a 100 bp gradual curve flat-

tening (increase in short-term rates or decrease in long-term rates) and a

100 bp gradual curve steepening (decrease in short-term rates or increase

in long-term rates) from the forward market curve. For further discussion of

core net interest income – managed basis see page 44.

The sensitivity analysis in Table 30 assumes that we take no action

in response to these rate shifts over the indicated years. The estimated

exposure is reported on a managed basis and reflects impacts that may

be realized primarily in net interest income and card income. This sensi-

tivity analysis excludes any impact that could occur in the valuation of

retained interests in the Corporation’s securitizations due to changes in

interest rate levels. For additional information on securitizations, see Note

8 – Securitizations to the Consolidated Financial Statements.

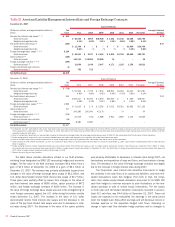

Table 29 Forward Rates

December 31

2007 2006

Federal

Funds

Ten-Year

Swap

Federal

Funds

Ten-Year

Swap

Spot rates

4.25% 4.67%

5.25% 5.18%

12-month forward rates

3.13

4.79 4.85 5.19

Table 30 Estimated Core Net Interest Income – Managed Basis at Risk

(Dollars in millions) December 31

Curve Change Short Rate Long Rate 2007 2006

+100 Parallel shift +100 +100

$ (952)

$(557)

-100 Parallel shift -100 -100

865

770

Flatteners

Short end +100 –

(1,127)

(687)

Long end – -100

(386)

(192)

Steepeners

Short end -100 –

1,255

971

Long end – +100

181

138

90

Bank of America 2007