Bank of America 2007 Annual Report Download - page 128

Download and view the complete annual report

Please find page 128 of the 2007 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

|

|

flow hedges are reclassified to income when the hedged transaction

affects earnings. Gains and losses on AFS debt and marketable equity

securities are reclassified to income as the gains or losses are realized

upon sale of the securities. Other-than-temporary impairment charges are

reclassified to income at the time of the charge. Translation gains or

losses on foreign currency translation adjustments are reclassified to

income upon the substantial sale or liquidation of investments in foreign

operations.

Earnings Per Common Share

Earnings per common share is computed by dividing net income available

to common shareholders by the weighted average common shares issued

and outstanding. For diluted earnings per common share, net income

available to common shareholders is divided by the weighted average

number of common shares issued and outstanding for each period plus

amounts representing the dilutive effect of stock options outstanding,

restricted stock and restricted stock units, if applicable. The effects of

restricted stock, restricted stock units and stock options are excluded

from the computation of diluted earnings per common share in periods in

which the effect would be antidilutive. Dilutive potential common shares

are calculated using the treasury stock method.

Foreign Currency Translation

Assets, liabilities and operations of foreign branches and subsidiaries are

recorded based on the functional currency of each entity. For certain of the

foreign operations, the functional currency is the local currency, in which

case the assets, liabilities and operations are translated, for consolidation

purposes, at period-end rates from the local currency to the reporting cur-

rency, the U.S. dollar. The resulting unrealized gains or losses are

reported as a component of accumulated OCI on a net-of-tax basis. When

the foreign entity’s functional currency is determined to be the U.S. dollar,

the resulting remeasurement currency gains or losses on foreign-

denominated assets or liabilities are included in net income.

Credit Card Arrangements

Endorsing Organization Agreements

The Corporation contracts with other organizations to obtain their endorse-

ment of the Corporation’s loan products. This endorsement may provide

the Corporation exclusive rights to market to the organization’s members

or to customers on behalf of the Corporation. These organizations endorse

the Corporation’s loan products and provide the Corporation with their

mailing lists and marketing activities. These agreements generally have

terms that range from five to seven years. The Corporation typically pays

royalties in exchange for their endorsement. These compensation costs to

the Corporation are recorded as contra-revenue against card income.

Cardholder Reward Agreements

The Corporation offers reward programs that allow its cardholders to earn

points that can be redeemed for a broad range of rewards including cash,

travel and discounted products. The Corporation establishes a rewards

liability based upon the points earned which are expected to be redeemed

and the average cost per point redemption. The points to be redeemed are

estimated based on past redemption behavior, card product type, account

transaction activity and other historical card performance. The liability is

reduced as the points are redeemed. The estimated cost of the rewards

programs is recorded as contra-revenue against card income.

Stock-based Compensation

On January 1, 2006, the Corporation adopted SFAS No. 123 (Revised

2004), “Share-Based Payment” (SFAS 123R) under the modified-

prospective application. The Corporation had previously adopted the fair

value-based method of accounting for stock-based employee compensa-

tion under SFAS No. 148, “Accounting for Stock-Based Compensation –

Transition and Disclosure – an amendment of FASB Statement No. 123,”

(SFAS 148) prospectively, on January 1, 2003. Had the Corporation

adopted SFAS 148 retrospectively, the impact in 2005 would not have

been material. For additional information on stock-based employee com-

pensation, see Note 17 – Stock-Based Compensation Plans to the Con-

solidated Financial Statements.

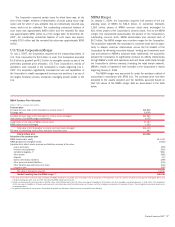

Note 2 – Merger and Restructuring Activity

LaSalle Bank Corporation Merger

On October 1, 2007, the Corporation acquired all the outstanding shares

of LaSalle, for $21.0 billion in cash. As part of the acquisition, ABN AMRO

Bank N.V. (the seller) capitalized approximately $6.3 billion as equity of

intercompany debt prior to the date of the acquisition. With this acquis-

ition, the Corporation significantly expanded its presence in metropolitan

Chicago, Illinois and Michigan by adding LaSalle’s commercial banking

clients, retail customers, and banking centers. LaSalle’s results of oper-

ations were included in the Corporation’s results beginning October 1,

2007.

The LaSalle acquisition was accounted for under the purchase

method of accounting in accordance with SFAS No. 141, “Business

Combinations” (SFAS 141). The preliminary purchase price has been allo-

cated to the assets acquired and the liabilities assumed based on their

fair values at the LaSalle acquisition date as summarized in the following

table.

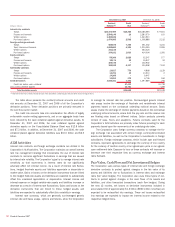

LaSalle Preliminary Purchase Price Allocation

(Dollars in millions)

Purchase price

$21,015

Preliminary allocation of the purchase price

LaSalle stockholders’ equity 12,495

LaSalle goodwill and intangible assets (2,728)

Adjustments to reflect assets acquired and liabilities assumed

at fair value:

Loans and leases (88)

Premises and equipment (139)

Identified intangibles

(1)

1,029

Other assets (248)

Exit and termination liabilities (339)

Other liabilities and deferred income taxes (72)

Fair value of net assets acquired 9,910

Preliminary goodwill resulting from the LaSalle merger (2)

$11,105

(1) Includes core deposit intangibles of $700 million and other intangibles of $329 million. The amortization

life for core deposit intangibles and other intangibles is 10 years. These intangibles are amortized on an

accelerated basis.

(2) No goodwill is expected to be deductible for tax purposes. The goodwill has been allocated across all of

the Corporation’s business segments.

126

Bank of America 2007