Bank of America 2007 Annual Report Download - page 55

Download and view the complete annual report

Please find page 55 of the 2007 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

|

|

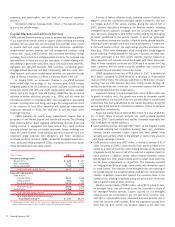

resulted. In several instances, commitments were either terminated by

the client or interest rate concessions (e.g., an increase in the stated

coupon) were obtained from the borrowers, thereby increasing the value

of the loans, in each case negating the need for any writedown. At

December 31, 2007, the Corporation’s share of the leveraged finance

forward calendar that consisted primarily of senior secured exposure

was $12.2 billion and our funded position held for distribution was $6.1

billion. In addition, we had limited investment grade exposure that was

in line with our normal exposure levels.

ŠStructured products losses were $5.2 billion, with a decline in revenue

of $6.6 billion in 2007 compared to the prior year. The decrease was

driven by $5.6 billion of losses resulting from our CDO exposure, $125

million of losses on CMBS funded debt and the forward calendar and

$875 million related to other structured products. See the detailed CDO

exposure discussion to follow. Other structured products, including resi-

dential mortgage-backed securities and structured credit trading, were

negatively impacted by spread widening due to the credit market dis-

ruptions during the second half of the year and by the breakdown of the

expected hedge correlations. For example, the divergence in valuation of

agency-based mortgage products, principally derivatives and forward

sales contracts, used to economically hedge non-agency mortgage

exposure resulted in losses on our residential mortgage-backed secu-

rities trading positions. At the end of the year, we held $13.7 billion of

funded CMBS debt of which $6.9 billion were floating-rate acquisition

related financings to major, well known operating companies. In addi-

tion, we had a forward calendar of just over $2.0 billion of which $1.1

billion were floating-rate acquisition related financings.

ŠEquity products revenue decreased $273 million primarily due to lower

client activity in equity capital markets and equity derivatives combined

with reduced trading results.

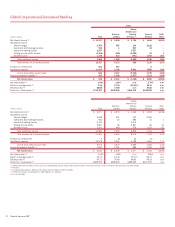

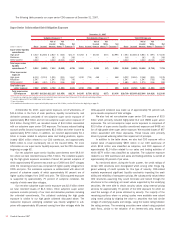

Collateralized Debt Obligation Exposure at December 31, 2007

CDO vehicles are special purpose entities that hold diversified pools of

fixed income securities. CDO vehicles issue multiple tranches of debt

securities, including commercial paper, mezzanine and equity securities.

We receive fees for structuring CDO vehicles and/or placing debt

securities with third party investors as part of our structured credit prod-

ucts business. Our CDO exposure can be divided into funded and

unfunded super senior liquidity commitment exposure, other super senior

exposure (i.e., cash positions and derivative contracts), warehouse, and

sales and trading positions. For more information on our CDO liquidity

commitments refer to Collateralized Debt Obligations as part of Off- and

On-Balance Sheet Arrangements beginning on page 60. Super senior

exposure represents the most senior class of commercial paper or notes

that are issued by the CDO vehicles. These financial instruments benefit

from the subordination of all other securities, including AAA-rated secu-

rities, issued by the CDO vehicles.

Bank of America 2007

53