Bank of America 2007 Annual Report Download - page 167

Download and view the complete annual report

Please find page 167 of the 2007 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

-

179

|

|

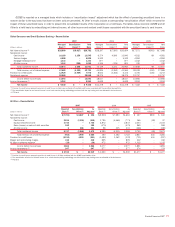

Level 3 Valuation Techniques

Financial instruments are considered Level 3 when their values are

determined using pricing models, discounted cash flow methodologies or

similar techniques and at least one significant model assumption or input

is unobservable. Level 3 financial instruments also include those for which

the determination of fair value requires significant management judgment

or estimation. For more information on Level 3 financial instruments, see

Note 1 – Summary of Significant Accounting Policies to the Consolidated

Financial Statements. A brief description of the valuation techniques used

for Level 3 assets and liabilities is provided below.

Derivatives

The fair values of Level 3 derivative instruments are estimated using propri-

etary valuation models that utilize both market observable and

unobservable parameters. Level 3 derivative instruments have primary risk

characteristics that relate to unobservable pricing parameters such as

private name credit spreads, credit correlations, long dated equity or inter-

est rate volatility skews and forward spreads.

Trading Account Assets and Available-for-Sale Debt Securities

Level 3 trading account assets and available-for-sale debt securities

include CDO positions and other ABS. At December 31, 2007, the majority

of these instruments were valued using a net asset value approach, which

considers the value of the underlying securities. Underlying assets are

valued using external pricing services, where available, or matrix pricing

based on the vintages and ratings, where applicable, of the assets. In

some situations when other market information was not available, secu-

rities are valued using projected cash flows, similar to the valuation of an

interest-only strip, based on estimated average life, seniority level and

vintage of underlying assets.

Loans and Leases

Certain large corporate loans including loan commitments, which the

Corporation has elected to account for at fair value and for which

observable market prices are not available, are considered Level 3. This is

normally the result of illiquidity due to the customer, the size of the loan or

the particular loan terms. In these cases, fair value is estimated using

discounted cash flow models with market-based credit spreads of com-

parable debt instruments or credit derivatives of the specific borrower or

comparable borrowers.

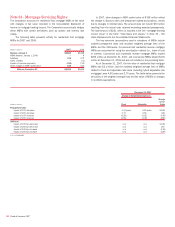

Mortgage Servicing Rights

The fair value of MSRs is determined using models which depend on esti-

mates of prepayment rates and resultant weighted average lives of the

MSRs and the option adjusted spread levels (OAS). For more information

on Level 3 MSRs, see Note 21 – Mortgage Servicing Rights to the Con-

solidated Financial Statements.

Other Assets

Level 3 other assets consist primarily of non-public equity investments,

certain held-for-sale loans and retained residual interests in securitiza-

tions. Non-public equity investments are initially valued at transaction price

and subsequently, adjusted when evidence is available to support such

adjustments. Such evidence includes changes in value as a result of IPOs,

market comparables, market liquidity, the investees’ financial results,

sales restrictions, or other changes in value. Mortgages are valued based

on instruments or portfolios with similar loan terms, collateral type and

credit quality. Retained residual interests in securitizations are based on

certain observable inputs such as interest rates and credit spreads, as

well as unobservable inputs such as estimated net charge-off and pay-

ment rates.

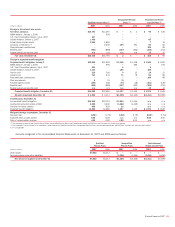

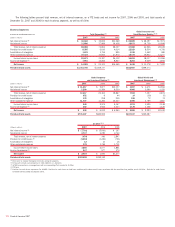

The table below summarizes gains and losses due to changes in fair value, including both realized and unrealized gains and losses, recorded in earn-

ings for Level 3 assets and liabilities during 2007. These amounts include gains and losses generated by loans, loans held-for-sale and loan commitments

for which the fair value option was elected and by other instruments, including certain derivative contracts, trading account assets, AFS debt securities,

MSRs, equity investments and retained interests in securitizations, which were carried at fair value prior to the adoption of SFAS 159.

Level 3 Instruments Only

Total Gains and Losses

(Dollars in millions)

Net

Derivatives

(1)

Trading

Account

Assets

(1)

Available-for-

Sale Debt

Securities

(1, 5)

Loans

and

Leases

(2)

Mortgage

Servicing

Rights

(1)

Other

Assets

(3)

Accrued

Expenses

and Other

Liabilities

(2)

Total

Classification of gains and losses (realized/

unrealized) included in earnings for 2007:

Card income $ – $ – $ – $ – $ – $ 103 $ – $ 103

Equity investment income

(4)

– – – – – 1,971 – 1,971

Trading account losses (515) (2,959) – (1) – (61) (5) (3,541)

Mortgage banking income (loss) 174 – – – 231 (29) – 376

Other income – – (398) (139) – 75 (274) (736)

Total

$(341) $(2,959) $(398) $(140) $231 $2,059 $(279) $(1,827)

(1) Amounts represented items which were carried at fair value prior to the adoption of SFAS 159.

(2) Amounts represented items for which the Corporation had elected the fair value option under SFAS 159.

(3) Amounts represented items which were carried at fair value prior to the adoption of SFAS 159 and certain portfolios of loans held-for-sale for which the Corporation had elected the fair value option under SFAS 159.

(4) During 2007, more than 90 percent of equity investment income’s Level 3 net gains were received in cash.

(5) Amount represents writedowns on certain securities that were deemed to be other-than-temporarily impaired during 2007.

Bank of America 2007

165