Bank of America 2007 Annual Report Download - page 127

Download and view the complete annual report

Please find page 127 of the 2007 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

|

|

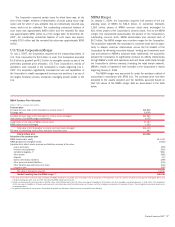

Level 1

Quoted prices in active markets for identical assets or

liabilities. Level 1 assets and liabilities include debt and

equity securities and derivative contracts that are traded in

an active exchange market, as well as certain U.S. Treas-

ury securities that are highly liquid and are actively traded

in over-the-counter markets.

Level 2

Observable inputs other than Level 1 prices, such as

quoted prices for similar assets or liabilities; quoted prices

in markets that are not active; or other inputs that are

observable or can be corroborated by observable market

data for substantially the full term of the assets or

liabilities. Level 2 assets and liabilities include debt secu-

rities with quoted prices that are traded less frequently

than exchange-traded instruments and derivative contracts

whose value is determined using a pricing model with

inputs that are observable in the market or can be derived

principally from or corroborated by observable market

data. This category generally includes U.S. Government

and agency mortgage-backed debt securities, corporate

debt securities, derivative contracts, residential mortgage

and loans held-for-sale.

Level 3

Unobservable inputs that are supported by little or no

market activity and that are significant to the fair value of

the assets or liabilities. Level 3 assets and liabilities

include financial instruments whose value is determined

using pricing models, discounted cash flow methodologies,

or similar techniques, as well as instruments for which the

determination of fair value requires significant manage-

ment judgment or estimation. This category generally

includes certain private equity investments, retained

residual interests in securitizations, residential MSRs,

asset-backed securities (ABS), highly structured or long-

term derivative contracts and certain collateralized debt

obligations (CDO) where independent pricing information

was not able to be obtained for a significant portion of the

underlying assets.

For more information on the fair value of the Corporation’s financial

instruments see Note 19 – Fair Value Disclosures to the Consolidated

Financial Statements.

Income Taxes

The Corporation accounts for income taxes in accordance with SFAS

No. 109, “Accounting for Income Taxes” (SFAS 109) as interpreted by FIN

48, resulting in two components of income tax expense: current and

deferred. Current income tax expense approximates taxes to be paid or

refunded for the current period. Deferred income tax expense results from

changes in deferred tax assets and liabilities between periods. These

gross deferred tax assets and liabilities represent decreases or increases

in taxes expected to be paid in the future because of future reversals of

temporary differences in the bases of assets and liabilities as measured

by tax laws and their bases as reported in the financial statements.

Deferred tax assets are also recognized for tax attributes such as net

operating loss carryforwards and tax credit carryforwards. Valuation allow-

ances are then recorded to reduce deferred tax assets to the amounts

management concludes are more-likely-than-not to be realized.

Under FIN 48, income tax benefits are recognized and measured

based upon a two-step model: 1) a tax position must be more-likely-

than-not to be sustained based solely on its technical merits in order to be

recognized, and 2) the benefit is measured as the largest dollar amount of

that position that is more-likely-than-not to be sustained upon settlement.

The difference between the benefit recognized for a position in accordance

with this FIN 48 model and the tax benefit claimed on a tax return is

referred to as an unrecognized tax benefit (UTB). The Corporation accrues

income-tax-related interest and penalties (if applicable) within income tax

expense.

For additional information on income taxes, see Note 18 – Income

Taxes to the Consolidated Financial Statements.

Retirement Benefits

The Corporation has established qualified retirement plans covering sub-

stantially all full-time and certain part-time employees. Pension expense

under these plans is charged to current operations and consists of several

components of net pension cost based on various actuarial assumptions

regarding future experience under the plans.

In addition, the Corporation has established unfunded supplemental

benefit plans and supplemental executive retirement plans for selected

officers of the Corporation and its subsidiaries (SERPS) that provide bene-

fits that cannot be paid from a qualified retirement plan due to Internal

Revenue Code restrictions. The SERPS were frozen and the executive offi-

cers do not accrue any additional benefits. These plans are nonqualified

under the Internal Revenue Code and assets used to fund benefit pay-

ments are not segregated from other assets of the Corporation; therefore,

in general, a participant’s or beneficiary’s claim to benefits under these

plans is as a general creditor. In addition, the Corporation has established

several postretirement healthcare and life insurance benefit plans.

The Corporation accounts for its retirement benefit plans in accord-

ance with SFAS No. 87, “Employers’ Accounting for Pensions” (SFAS 87),

SFAS No. 88, “Employers’ Accounting for Settlements and Curtailment of

Defined Benefit Pension Plans and for Termination Benefits,” and SFAS

No. 106, “Employers’ Accounting for Postretirement Benefits Other Than

Pensions,” as applicable.

On December 31, 2006, the Corporation adopted SFAS No. 158,

“Employers’ Accounting for Defined Benefit Pension and Other Postretire-

ment Plans, an amendment of FASB Statements No. 87, 88, 106, and

132(R)” (SFAS 158) which requires the recognition of a plan’s over-funded

or under-funded status as an asset or liability with an offsetting adjust-

ment to accumulated OCI. SFAS 158 requires the determination of the fair

values of a plan’s assets at a company’s year end and recognition of

actuarial gains and losses, prior service costs or credits, and transition

assets or obligations as a component of accumulated OCI. These amounts

were previously netted against the plans’ funded status in the Corpo-

ration’s Consolidated Balance Sheet. These amounts will be subsequently

recognized as components of net periodic benefit costs. Further, actuarial

gains and losses that arise in subsequent periods that are not initially

recognized as a component of net periodic benefit cost will be recognized

as a component of accumulated OCI. Those amounts will subsequently be

recorded as a component of net periodic benefit cost as they are amor-

tized during future periods.

Accumulated Other Comprehensive Income

The Corporation records gains and losses on cash flow hedges, unrealized

gains and losses on AFS debt and marketable equity securities, unrecog-

nized actuarial gains and losses, transition obligation and prior service

costs on pension and postretirement plans, foreign currency translation

adjustments, and related hedges of net investments in foreign operations

in accumulated OCI, net-of-tax. Accumulated OCI also includes fair value

adjustments on certain retained interests in the Corporation’s securitiza-

tion transactions. Gains or losses on derivatives accounted for as cash

Bank of America 2007

125