Bank of America 2007 Annual Report Download - page 93

Download and view the complete annual report

Please find page 93 of the 2007 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

|

|

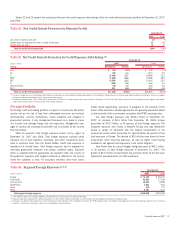

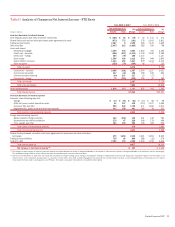

Our core net interest income – managed basis, was liability sensitive

at both December 31, 2007 and 2006. At December 31, 2007, our core

net interest income – managed basis became more liability sensitive as

we positioned ourselves for greater downside risk than was reflected in

the forward curve. We evaluate our balance sheet position on an ongoing

basis. Since December 31, 2007, we have repositioned our balance sheet

to a more modest level given changes in forward rates and we will con-

tinue to evaluate our balance sheet positioning going forward. Over a

12-month horizon, we would benefit from falling rates or a steepening of

the yield curve beyond what is already implied in the forward market curve.

As part of our ALM activities, we use securities, residential mort-

gages, and interest rate and foreign exchange derivatives in managing

interest rate sensitivity.

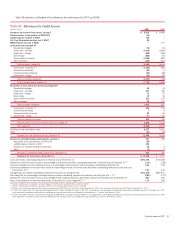

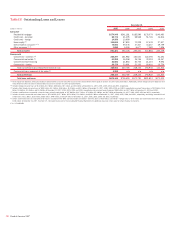

Securities

The securities portfolio is an integral part of our ALM position. The secu-

rities portfolio is primarily comprised of debt securities and includes

mortgage-backed securities and to a lesser extent corporate, municipal

and other investment grade debt securities. During 2007 and 2006, we

purchased AFS debt securities of $28.0 billion and $40.9 billion, sold

$27.9 billion and $55.1 billion, and had maturities and received paydowns

of $19.2 billion and $22.4 billion. We realized $180 million in gains and

$443 million in losses on sales of debt securities during 2007 and 2006.

Additionally, during 2007, we acquired $32.4 billion of AFS debt securities

as part of the LaSalle and U.S. Trust Corporation acquisitions and con-

tinue to evaluate the appropriate holding levels.

The value of our accumulated OCI loss related to AFS debt securities

improved by a pre-tax amount of $2.0 billion during 2007, driven by a

decrease in interest rates. For those securities that are in an unrealized

loss position we have the intent and ability to hold these securities to

recovery.

Accumulated OCI includes $6.5 billion in after-tax gains at

December 31, 2007, related to unrealized gains associated with our AFS

securities portfolio, including $1.9 billion of unrealized losses related to

AFS debt securities and $8.4 billion of unrealized gains related to AFS

marketable equity securities. Total market value of the AFS debt securities

was $213.3 billion at December 31, 2007 with a weighted average dura-

tion of 4.3 years and primarily relates to our mortgage-backed securities

portfolio.

Prospective changes to the accumulated OCI amounts for the AFS

securities portfolio will be driven by further interest rate, credit or price

fluctuations (including market value fluctuations associated with our CCB

investment), the collection of cash flows including prepayment and

maturity activity, and the passage of time. During the fourth quarter of

2007, shares of the Corporation’s strategic investment in CCB are now

accounted for as AFS marketable equity securities and are carried at a fair

value of $16.2 billion. The unrealized gain on this investment of $8.4 bil-

lion net-of-tax is subject to currency and price fluctuation, and is recorded

in accumulated OCI.

In connection with adopting SFAS 159, the Corporation reclassified

approximately $3.7 billion from AFS debt securities to trading account

assets during the first quarter of 2007. There were no net unrealized gains

or losses associated with these securities recorded in accumulated OCI as

these securities were hedged using SFAS 133 hedge accounting. Accord-

ingly, there was no impact on the Corporation’s transition adjustment to

beginning retained earnings upon adoption of SFAS 159 on January 1,

2007.

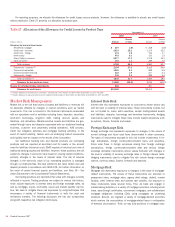

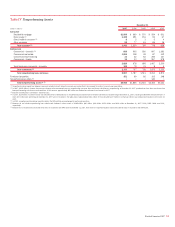

Residential Mortgage Portfolio

During 2007 and 2006, we purchased $22.5 billion and $42.3 billion of

residential mortgages related to ALM activities, and added $66.3 billion

and $51.9 billion of originated residential mortgages. We sold $34.0 bil-

lion and $11.0 billion of residential mortgages during 2007 and 2006,

which included $23.7 billion and $9.2 billion of originated residential

mortgages, resulting in gains of $271 million and $98 million. Additionally,

we received paydowns of $28.2 billion and $24.7 billion during 2007 and

2006. The ending balance at December 31, 2007 was $274.9 billion

compared to $241.2 billion at December 31, 2006.

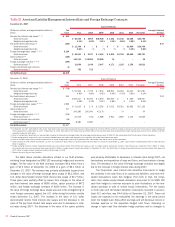

Interest Rate and Foreign Exchange Derivative

Contracts

Interest rate and foreign exchange derivative contracts are utilized in our

ALM activities and serve as an efficient tool to mitigate our interest rate

and foreign exchange risk. We use derivatives to hedge the variability in

cash flows or changes in fair value on our balance sheet due to interest

rate and foreign exchange components. For additional information on our

hedging activities, see Note 4 – Derivatives to the Consolidated Financial

Statements.

Our interest rate contracts are generally non-leveraged generic inter-

est rate and foreign exchange basis swaps, options, futures, and for-

wards. In addition, we use foreign exchange contracts, including cross-

currency interest rate swaps and foreign currency forward contracts, to

mitigate the foreign exchange risk associated with foreign currency-

denominated assets and liabilities, as well as certain equity investments

in foreign subsidiaries. Table 31 reflects the notional amounts, fair value,

weighted average receive fixed and pay fixed rates, expected maturity, and

estimated duration of our open ALM derivatives at December 31, 2007

and 2006.

Changes to the composition of our derivatives portfolio over the

course of 2007 reflect actions taken for interest rate and foreign exchange

rate risk management. The decisions to reposition our derivative portfolio

are based upon the current assessment of economic and financial con-

ditions including the interest rate environment, balance sheet composition

and trends, and the relative mix of our cash and derivative positions. Our

interest rate swap positions (including foreign exchange contracts)

changed to a net receive fixed position of $101.9 billion on December 31,

2007 compared to a net receive fixed position of $12.3 billion on

December 31, 2006. Changes in the notional levels of our interest rate

swap position were driven by the net termination of $88.9 billion in pay

fixed swaps, the net termination of $9.5 billion in U.S. dollar denominated

receive fixed swaps, and the addition of $10.2 billion in foreign denomi-

nated receive fixed swaps. The notional amount of our foreign exchange

basis swaps increased $22.6 billion to $54.5 billion at December 31,

2007 compared to $31.9 billion at December 31, 2006. The notional

amount of our option position decreased $103.2 billion to $140.1 billion

at December 31, 2007 compared to $243.3 billion at December 31,

2006. The decrease in the notional amount of options was due to the net

terminations and expirations of $85.0 billion in caps and floors and termi-

nations of $18.2 billion of swaptions.

Bank of America 2007

91