Bank of America 2007 Annual Report Download - page 64

Download and view the complete annual report

Please find page 64 of the 2007 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

|

|

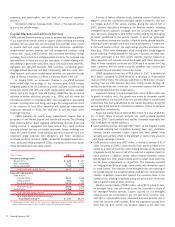

collateralized by projected cash flows from long-term contracts (e.g., tele-

vision broadcast contracts, stadium revenues and royalty payments)

which, as mentioned above, incorporate features that provide credit sup-

port at a level equivalent to an investment grade. At December 31, 2007,

the weighted average life of assets in the consolidated conduit was 5.4

years and the weighted average maturity of commercial paper issued by

this conduit was 40 days. Assets of the Corporation are not available to

pay creditors of the consolidated conduit except to the extent the Corpo-

ration may be obligated to perform under the liquidity commitments and

SBLCs. Assets of the consolidated conduit are not available to pay cred-

itors of the Corporation.

We do not consolidate the other two conduits as we do not expect to

absorb a majority of the variability of the conduits. At December 31, 2007,

our liquidity commitments to the unconsolidated conduits were collateral-

ized by student loans (27 percent), credit card loans and trade receivables

(10 percent each), and auto loans (eight percent). Less than one percent

of these assets are subprime residential mortgages. In addition, 29 per-

cent of our commitments were collateralized by the conduits’ short-term

lending arrangements with investment funds, primarily real estate funds,

which as mentioned above, incorporate features that provide credit sup-

port at a level equivalent to an investment grade. Amounts advanced

under these arrangements will be repaid when the investment funds issue

capital calls to their qualified equity investors. At December 31, 2007, the

weighted average life of assets in the unconsolidated conduits was 2.6

years and the weighted average maturity of commercial paper issued by

these conduits was 36 days.

The liquidity commitments and SBLCs provided to unconsolidated

conduits are included in Table 10 in the Obligations and Commitments

section beginning on page 63. We have no other contractual obligations to

the unconsolidated conduits, nor do we intend to provide noncontractual

or other forms of support.

On a combined basis, the unconsolidated conduits issued approx-

imately $27 million of capital notes and equity interests to third parties.

This represents the maximum amount of loss that would be absorbed by

the third party investors. Based on an analysis of projected cash flows, we

have determined that the Corporation will not absorb a majority of the

variability created by the assets of the conduits.

Despite the market disruptions in the second half of 2007, the con-

duits did not experience any material difficulties in issuing commercial

paper. The Corporation did not purchase any commercial paper issued by

the conduits other than incidentally and in its role as commercial paper

dealer.

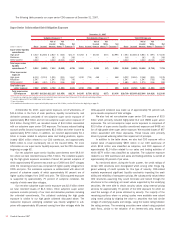

Municipal Bond Trusts and Corporate SPEs

We have provided a total of $17.7 billion and $7.9 billion in liquidity sup-

port to municipal bond trusts and corporate SPEs at December 31, 2007

and 2006. We administer municipal bond trusts that hold highly-rated,

long-term, fixed-rate municipal bonds, some of which are callable prior to

maturity, for which we provided liquidity support of $13.4 billion and $2.6

billion at December 31, 2007 and 2006. In addition, we administer sev-

eral conduits to which we provided $4.3 billion and $5.3 billion of liquidity

support at December 31, 2007 and 2006.

As it relates to the municipal bond trusts the weighted average

remaining life of the bonds at December 31, 2007 was 20.8 years. Sub-

stantially all of the bonds are rated AAA or AA and some of the bonds

benefit from being wrapped by monolines. There were no material write-

downs or downgrades of assets or issuers during 2007. The trusts obtain

financing by issuing floating-rate trust certificates that reprice on a weekly

basis to third party investors. The floating-rate investors have the right to

tender the certificates at any time upon seven days notice. We serve as

remarketing agent and liquidity provider for the trusts. Should we be

unable to remarket the tendered certificates, we are generally obligated to

purchase them at par. We are not obligated to purchase the certificate if a

bond’s credit rating declines below investment grade or in the event of

certain defaults or bankruptcy of the issuer and/or insurer. The total

notional amount of floating-rate certificates for which we provide liquidity

support was $13.4 billion and $2.6 billion at December 31, 2007 and

2006. Some of these trusts are QSPEs. We consolidate those trusts that

are not QSPEs if we hold the residual interest or otherwise expect to

absorb a majority of the variability of the trusts. We have $6.1 billion of

liquidity commitments to unconsolidated trusts at December 31, 2007,

which are included in Table 10 in the Obligations and Commitments sec-

tion beginning on page 63.

Assets of the other corporate conduits consisted primarily of high-

grade, long-term municipal, corporate, and mortgage-backed securities

which had a weighted average remaining life of approximately 7.5 years at

December 31, 2007. Substantially all of the securities are rated AAA or AA

and some of the bonds benefit from being wrapped by monolines. There

were no material write-downs or downgrades of assets or insurers during

2007. These conduits, which are QSPEs, obtain funding by issuing com-

mercial paper to third party investors. At December 31, 2007, the

weighted average maturity of the commercial paper was 25 days. We have

entered into derivative contracts which provide interest rate, currency and

a pre-specified amount of credit protection to the entities in exchange for

the commercial paper rate. In addition, we may be obligated to purchase

assets from the vehicles if the assets or insurers are downgraded. If an

asset’s rating declines below a certain investment quality as evidenced by

its credit rating or defaults, we are no longer exposed to the risk of loss.

Due to the market disruptions during the second half of 2007, these

conduits began to experience difficulties in issuing commercial paper as

credit spreads widened. On occasion, including in the first quarter of

2008, we held some of the issued commercial paper when marketing

attempts were unsuccessful. In the event that we are unable to remarket

the conduits’ commercial paper such that it no longer qualifies as a QSPE,

we would consolidate the conduit which may have an adverse impact on

the fair value of the related derivative contracts. At December 31, 2007

we did not hold any commercial paper issued by the conduits.

We have no other contractual obligations to the unconsolidated bond

trusts and conduits described above, nor do we intend to provide non-

contractual or other forms of support.

Derivative activity related to these entities is included in Note 4 –

Derivatives to the Consolidated Financial Statements. For more

information on QSPEs, see Note 9 – Variable Interest Entities to the Con-

solidated Financial Statements. For additional information on our monoline

exposure, see Industry Concentrations beginning on page 79.

Collateralized Debt Obligation Vehicles

CDOs are SPEs that hold diversified pools of fixed income securities. They

issue multiple tranches of debt securities, including commercial paper and

equity securities. We receive fees for structuring the CDOs and/or placing

debt securities with third party investors. We provided total liquidity sup-

port of $12.3 billion and $7.7 billion at December 31, 2007 and 2006

consisting of $10.0 billion and $2.1 billion of written put options and $2.3

billion and $5.5 billion of other forms of liquidity support.

At December 31, 2007 and 2006, we provided liquidity support in

the form of written put options on $10.0 billion and $2.1 billion of

commercial paper issued by CDOs, including $3.2 billion issued by a

consolidated CDO at December 31, 2007. No third parties provide similar

62

Bank of America 2007