Bank of America 2007 Annual Report Download - page 74

Download and view the complete annual report

Please find page 74 of the 2007 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

|

|

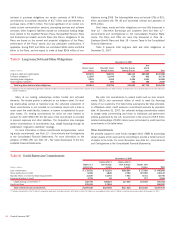

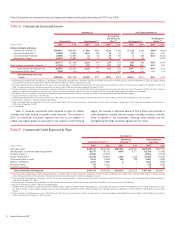

Credit Card – Domestic

The consumer domestic credit card portfolio is managed in Card Services.

Outstandings in the held domestic credit card loan portfolio increased

$4.6 billion in 2007 compared to 2006 due to organic growth in the portfo-

lio partially offset by an increase in securitized levels. The $136 million

decrease in held domestic loans past due 90 days or more and still accru-

ing interest was driven by the addition of higher loss profile accounts to

the securitization trust and an increased level of securitizations partially

offset by portfolio seasoning.

Net charge-offs for the held domestic portfolio decreased $31 million

to $3.1 billion, or 5.29 percent of total average held credit card – domes-

tic loans compared to 4.85 percent (5.00 percent excluding the impact of

SOP 03-3) in 2006. Net charge-offs decreased primarily due to the addi-

tion of higher loss profile accounts to the securitization trust and an

increased level of securitizations as well as the absence of 2006 charge-

offs related to changes made in credit card minimum payment require-

ments. These decreases were partially offset by portfolio seasoning and

increases from the unusually low charge-off levels experienced in 2006

post bankruptcy reform.

Managed domestic credit card outstandings increased $9.3 billion to

$151.9 billion in 2007 compared to 2006 due to an increase in retail and

cash volumes and lower payment rates. Managed net losses increased

$1.6 billion to $7.0 billion, or 4.91 percent of total average managed

domestic loans compared to 3.89 percent (3.96 percent excluding the

impact of SOP 03-3) in 2006. The increases were primarily due to portfolio

seasoning and increases from the unusually low loss levels experienced in

2006 post bankruptcy reform.

See page 73 for a discussion of the impact of SOP 03-3 on managed

losses and net charge-offs.

Credit Card – Foreign

The consumer foreign credit card portfolio is managed in Card Services.

Outstandings in the held foreign credit card loan portfolio increased $4.0

billion to $15.0 billion in 2007 compared to 2006 due to the strengthen-

ing of foreign currencies against the U.S. dollar, organic growth and portfo-

lio acquisitions. Net charge-offs for the held foreign portfolio increased

$153 million to $378 million, or 3.06 percent of total average held credit

card – foreign loans compared to 2.46 percent (3.05 percent excluding the

impact of SOP 03-3) in 2006. The increases in held net charge-offs were

due to seasoning of the European portfolio and strengthening of foreign

currencies against the U.S. dollar.

Managed foreign credit card outstandings increased $3.9 billion to

$31.8 billion in 2007 compared to 2006 due to the same reasons as the

increase in held outstandings stated above. Net losses for the managed

foreign portfolio increased $274 million to $1.3 billion, or 4.24 percent of

total average managed credit card – foreign loans compared to 3.95 per-

cent (4.17 percent excluding the impact of SOP 03-3) in 2006. The

increases in managed net losses were due to the same reasons as the

increases in held net charge-offs stated above.

See page 73 for a discussion of the impact of SOP 03-3 on managed

losses and net charge-offs.

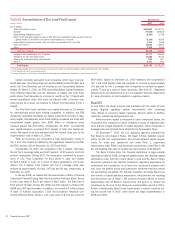

Home Equity

At December 31, 2007, approximately 74 percent of the managed home

equity portfolio was included in GCSBB, while the remainder of the portfo-

lio was mostly in GWIM. This portfolio consists of both revolving and

non-revolving first and second lien residential mortgage loans and lines of

credit. On a held basis, outstanding home equity loans increased $26.9

billion, or 31 percent, at December 31, 2007 compared to 2006, largely

due to organic home equity production and the LaSalle acquisition.

Nonperforming home equity loans increased $1.0 billion and net

charge-offs increased $223 million to $274 million or 0.28 percent of total

average held home equity loans compared to 0.07 percent in 2006. These

increases were driven by deterioration in the housing markets, including

significant declines in home prices in certain geographic areas, as well as

the seasoning of the portfolio reflective of growth. Although it remains

unclear how long the recent and accelerated declines in the consumer

housing markets will continue, this recent deterioration will negatively

impact our home equity portfolio and will result in a higher provision for

credit losses.

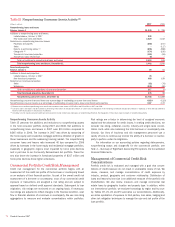

Direct/Indirect Consumer

At December 31, 2007, approximately 50 percent of the managed direct/

indirect portfolio was included in Business Lending (automotive, marine,

motorcycle and recreational vehicle loans); 44 percent was included in

GCSBB (student and other non-real estate secured and unsecured

personal loans) and the remainder was included in GWIM (other non-real

estate secured and unsecured personal loans).

On a held basis, outstanding loans and leases increased $17.5 bil-

lion in 2007 compared to 2006 due to growth in the Card Services

unsecured lending product, retail automotive portfolio purchases and

reduced securitization activity. Loans past due 90 days or more and still

accruing interest increased $367 million due to portfolio seasoning

reflective of growth in the businesses and reduced securitization activity.

Net charge-offs increased $763 million to $1.4 billion, or 1.95 percent of

total average held direct/indirect loans compared to 1.14 percent (1.36

percent excluding the impact of SOP 03-3) in 2006. The increases were

primarily driven by growth, seasoning and increases from the unusually low

charge-off levels experienced in 2006 post bankruptcy reform in the Card

Services unsecured lending portfolio, growth, seasoning and deterioration

in the retail automotive and other dealer-related portfolios and the impact

of the Corporation discontinuing sales of receivables into the unsecured

lending trust.

Managed direct/indirect loans outstanding increased $12.3 billion to

$78.6 billion in 2007 compared to 2006, driven by growth in the Card

Services unsecured lending product and retail automotive portfolio pur-

chases. Net losses for the managed loan portfolio increased $678 million

to $1.6 billion, or 2.14 percent of total average managed direct/indirect

loans compared to 1.49 percent (1.69 percent excluding the impact of

SOP 03-3) in 2006. The increases were primarily driven by growth, season-

ing and increases from the unusually low loss levels experienced in 2006

post bankruptcy reform in the Card Services unsecured lending portfolio

and higher losses in the retail automotive and other dealer-related portfo-

lios due to growth, seasoning and deterioration.

See page 73 for a discussion of the impact of SOP 03-3 on managed

losses and net charge-offs.

Other Consumer

At December 31, 2007, approximately 78 percent of the other consumer

portfolio was primarily associated with the portfolios from certain

consumer finance businesses that we have previously exited and was

included in All Other. The remainder consisted of the foreign consumer

loan portfolio which was mostly included in Card Services. Other consumer

outstanding loans and leases decreased $1.2 billion, or 24 percent, at

December 31, 2007 compared to December 31, 2006, driven mainly by

the sale of our Latin American operations. The Corporation classifies

deposit overdraft charge-offs as other consumer. Net charge-offs increased

$61 million, or 357 bps, compared to 2006 driven by overdraft net charge-

offs associated with deposit account growth.

72

Bank of America 2007