Bank of America 2007 Annual Report Download - page 65

Download and view the complete annual report

Please find page 65 of the 2007 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

|

|

commitments to these CDOs. The commercial paper is the most senior

class of securities issued by the CDOs and benefits from the sub-

ordination of all other securities, including AAA-rated securities. The

amount that is principally backed by subprime residential mortgage

exposure (net of insurance and prior to writedowns) totaled $7.4 billion.

This amount included approximately $2.8 billion of high grade ABS, $4.2

billion of CDOs-squared, of which $3.2 billion were consolidated, and

$363 million of mezzanine ABS.

The commercial paper subject to the put options is the most senior

class of securities issued by the CDOs and benefits from the sub-

ordination of all other securities, including AAA-rated securities. We are

obligated under the written put options to provide funding to the CDOs by

purchasing the commercial paper at predetermined contractual yields in

the event of a severe disruption in the short-term funding market as evi-

denced by the inability of the CDOs to issue commercial paper at spreads

below a predetermined rate.

Prior to the second half of 2007, we believed that the likelihood of

our experiencing an economic loss as the result of our obligations under

the written put options was remote. However, due to severe market dis-

ruptions during the second half of 2007, the CDOs holding the put options

began to experience difficulties in issuing commercial paper. Shortly

thereafter, a significant portion of the assets held in these CDOs were

downgraded or threatened with downgrade by the rating agencies. As a

result of these factors, we began to purchase commercial paper that could

not be issued to third parties at less than the contractual yield specified in

our liquidity obligations. See Note 13 – Commitments and Contingencies

to the Consolidated Financial Statements for more information on the writ-

ten put options. These written put options are recorded as derivatives on

the Consolidated Balance Sheet and are carried at fair value with changes

in fair value recorded in trading account profits (losses). Derivative activity

related to these entities is included in Note 4 – Derivatives to the Con-

solidated Financial Statements.

We also administer a CDO conduit that obtains funds by issuing

commercial paper to third party investors. The conduit held $2.3 billion

and $5.5 billion of assets at December 31, 2007 and 2006 consisting of

super senior tranches of debt securities issued by other CDOs, none of

which are principally backed by subprime residential mortgages at

December 31, 2007. We provide liquidity support equal to the amount of

assets in this conduit which obligates us to purchase the commercial

paper at a predetermined contractual yield in the event of a severe dis-

ruption in the short-term funding market as evidenced by the inability of

the conduit to issue commercial paper at spreads below a predetermined

rate. In addition, we are obligated to purchase assets from the conduit or

absorb market losses on the sale of assets in the event of a downgrade or

decline in credit quality of the assets. Our $2.3 billion liquidity commit-

ment to the conduit at December 31, 2007 is included in Table 10 in the

Obligations and Commitments section. We are the sole provider of liquidity

to the CDO vehicle.

During the fourth quarter of 2007, as contractually allowed in our role

as conduit administrator, the Corporation removed certain assets from the

CDO conduit due to a decline in credit quality. The CDO conduit also began

to experience difficulties in issuing commercial paper due to market dis-

ruptions during the second half of 2007, and we began to purchase

commercial paper that could not be issued to third parties at less than the

contractual yield specified in our liquidity obligations.

At December 31, 2007, we held $6.6 billion of commercial paper on

the balance sheet that was issued by unconsolidated CDO vehicles of

which $5.0 billion related to the written put options and $1.6 billion

related to other liquidity support. We also held AFS debt securities in

consolidated CDO vehicles with a fair value of $2.8 billion that were princi-

pally related to certain assets that were removed from the CDO conduit, as

discussed above. We recorded losses of $3.2 billion, net of insurance,

in trading account profits (losses) in 2007 of which $2.7 billion related to

written put options and $519 million related to other liquidity support.

These losses are included in the $4.0 billion of net writedowns on super

senior CDO exposure which is discussed in more detail beginning on

page 53.

Asset Acquisition Conduits

We administer two unconsolidated conduits which acquire assets on

behalf of our customers. The return on the assets held in the conduits,

which consist principally of liquid exchange-traded securities and some

leveraged loans, is passed through to our customers through a series of

derivative contracts. We consolidate a third conduit which holds sub-

ordinated debt securities for our benefit. These conduits obtain funding

through the issuance of commercial paper and subordinated certificates to

third party investors. Repayment of the commercial paper and certificates

is assured by derivative contracts between the Corporation and the con-

duits, and we are reimbursed through the derivative contracts with our

customers. Our performance under the derivatives is collateralized by the

underlying assets. Derivative activity related to these entities is included in

Note 4 – Derivatives to the Consolidated Financial Statements.

Despite the market disruptions in the second half of 2007, the con-

duits did not experience any material difficulties in issuing commercial

paper. The Corporation did not hold a significant amount of commercial

paper issued by the conduits at any time during 2007. At December 31,

2007, the weighted average life of commercial paper issued by the con-

duits was 34 days.

We have no other contractual obligations to the conduits described

above, nor do we intend to provide noncontractual or other forms of

support.

Customer-Sponsored Conduits

We provide liquidity facilities to conduits that are sponsored by our custom-

ers and which provide them with direct access to the commercial paper

market. We are typically one of several liquidity providers for a customer’s

conduit. We do not provide SBLCs or other forms of credit enhancement to

these conduits. Assets of these conduits consist primarily of auto loans,

student loans and credit card receivables. The liquidity commitments

benefit from structural protections which vary depending upon the pro-

gram, but given these protections, the exposures are viewed to be of

investment grade quality.

These commitments are included in Table 10 in the Obligations and

Commitments section. As we typically provide less than 20 percent of the

total liquidity commitments to these conduits and do not provide other

forms of support, we have concluded that we do not hold a significant

variable interest in the conduits and they are not included in our dis-

cussion of VIEs in Note 9 – Variable Interest Entities to the Consolidated

Financial Statements.

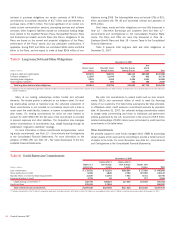

Obligations and Commitments

We have contractual obligations to make future payments on debt and

lease agreements. Additionally, in the normal course of business, we enter

into contractual arrangements whereby we commit to future purchases of

products or services from unaffiliated parties. Obligations that are legally

binding agreements whereby we agree to purchase products or services

with a specific minimum quantity defined at a fixed, minimum or variable

price over a specified period of time are defined as purchase obligations.

Bank of America 2007

63