Bank of America 2007 Annual Report Download - page 165

Download and view the complete annual report

Please find page 165 of the 2007 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

-

177

-

178

-

179

|

|

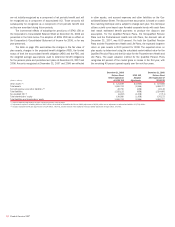

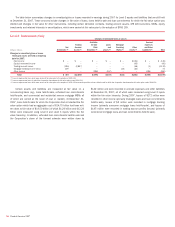

Loans Held-for-Sale

The Corporation also elected to account for certain loans held-for-sale at

fair value. Electing to use fair value allows a better offset of the changes

in fair values of the loans and the derivative instruments used to econom-

ically hedge them without the burden of complying with the requirements

for hedge accounting under SFAS 133. The Corporation has not elected to

fair value other loans held-for-sale primarily because these loans are float-

ing rate loans that are not economically hedged using derivative instru-

ments. Fair values for loans held-for-sale are based on quoted market

prices, where available, or are determined by discounting estimated cash

flows using interest rates approximating the Corporation’s current origi-

nation rates for similar loans and adjusted to reflect the inherent credit

risk. At December 31, 2007, residential mortgage loans, commercial

mortgage loans, and other loans held-for-sale for which the fair value

option was elected had an aggregate fair value of $15.77 billion and an

aggregate outstanding principal balance of $16.72 billion and were

recorded in other assets. Interest income on these loans is recorded in

other interest income. Net gains (losses) resulting from changes in fair

value of these loans, including realized gains (losses) on sale, of $333

million were recorded in mortgage banking income, $(348) million were

recorded in trading account profits (losses), and $(58) million were

recorded in other income during 2007. These changes in fair value are

mostly offset by hedging activities. An immaterial portion of these amounts

was attributable to changes in instrument-specific credit risk. The adoption

of SFAS 159 resulted in an increase of $256 million in mortgage banking

income, and in an increase of $212 million in noninterest expense for

2007. Subsequent to the adoption of SFAS 159, mortgage loan origination

costs are recognized in noninterest expense when incurred. Previously,

mortgage loan origination costs would have been capitalized as part of the

carrying amount of the loans and recognized as a reduction of mortgage

banking income upon the sale of such loans.

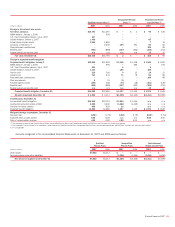

Debt Securities

Effective January 1, 2007, the Corporation elected to fair value $3.7 bil-

lion of AFS debt securities through earnings. Changes in fair value result-

ing from foreign currency exposure, which was the primary driver of fair

value for these securities, had previously been hedged by derivatives that

qualified for fair value hedge accounting in accordance with SFAS 133.

Electing the fair value option allows the Corporation to eliminate the bur-

den of complying with the requirements for hedge accounting under SFAS

133 without introducing accounting volatility. Following election of the fair

value option, these securities were reclassified to trading account assets.

The Corporation did not elect the fair value option for other AFS debt secu-

rities because they were not hedged by derivatives that qualified for hedge

accounting in accordance with SFAS 133.

Structured Reverse Repurchase Agreements

The Corporation elected to fair value certain structured reverse repurchase

agreements which were hedged with derivatives which qualified for fair

value hedge accounting in accordance with SFAS 133. Election of the fair

value option allows the Corporation to reduce the burden of complying with

the requirements of hedge accounting under SFAS 133. At December 31,

2007, these instruments had an aggregate fair value of $2.58 billion and

a principal balance of $2.54 billion recorded in federal funds sold and

securities purchased under agreements to resell. Interest earned on these

instruments continues to be recorded in interest income. Net gains result-

ing from changes in fair value of these instruments of $23 million were

recorded in other income for 2007. The Corporation did not elect to fair

value other financial instruments within the same balance sheet category

because they were not economically hedged using derivatives.

Long-term Deposits

The Corporation elected to fair value certain long-term fixed rate deposits

which are economically hedged with derivatives. At December 31, 2007,

these instruments had an aggregate fair value of $2.00 billion and princi-

pal balance of $1.99 billion recorded in interest-bearing deposits. Interest

paid on these instruments continues to be recorded in interest expense.

Net losses resulting from changes in fair value of these instruments of

$26 million were recorded in other income for 2007. Election of the fair

value option will allow the Corporation to reduce the accounting volatility

that would otherwise result from the accounting asymmetry created by

accounting for the financial instruments at historical cost and the

economic hedges at fair value. The Corporation did not elect to fair value

other financial instruments within the same balance sheet category

because they were not economically hedged using derivatives.

Fair Value Measurement

SFAS 157 defines fair value as the exchange price that would be received

for an asset or paid to transfer a liability (an exit price) in the principal or

most advantageous market for the asset or liability in an orderly trans-

action between market participants on the measurement date. For addi-

tional information on how the Corporation measures fair value, see Note 1

– Summary of Significant Accounting Principles to the Consolidated Finan-

cial Statements.

Bank of America 2007

163