Bank of America 2007 Annual Report Download - page 54

Download and view the complete annual report

Please find page 54 of the 2007 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

|

|

seasoning and deterioration, and the level of commercial recoveries

declined.

Noninterest expense increased $111 million, or five percent, primar-

ily due to the LaSalle merger.

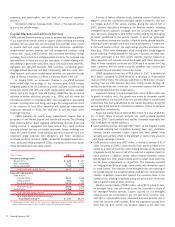

Capital Markets and Advisory Services

CMAS provides financial products, advisory services and financing globally

to our institutional investor clients in support of their investing and trading

activities. We also work with our commercial and corporate issuer clients

to provide debt and equity underwriting and distribution capabilities,

merger-related advisory services and risk management solutions using

interest rate, equity, credit, currency and commodity derivatives, foreign

exchange, fixed income and mortgage-related products. The business may

take positions in these products and participate in market-making activ-

ities dealing in government securities, equity and equity-linked securities,

high-grade and high-yield corporate debt securities, commercial paper,

mortgage-backed securities and ABS. Underwriting debt and equity, secu-

rities research and certain market-based activities are executed through

Banc of America Securities, LLC which is a primary dealer in the U.S.

In January 2008, we announced changes in our CMAS business

which better align the strategy of this business with GCIB’s broader

integrated platform. We will continue to provide corporate, commercial and

sponsored clients with debt and equity capital-raising services, strategic

advice, and a full range of corporate banking capabilities. We will reduce

activities in certain structured products (e.g., CDOs) and will resize the

international platform to emphasize debt, cash management, and trading

services, including rates and foreign exchange. The realignment will result

in the reduction of front office personnel with additional infrastructure

headcount reduction to follow. We also plan to sell our equity prime

brokerage business.

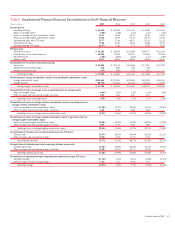

CMAS evaluates its results using market-based revenue that is

comprised of net interest income and noninterest income. The following

table presents further detail regarding market-based revenue. Sales and

trading revenue is segregated into fixed income from liquid products

(primarily interest rate and commodity derivatives, foreign exchange con-

tracts and public finance), credit products (primarily investment and non-

investment grade corporate debt obligations and credit derivatives),

structured products (primarily CMBS, residential mortgage-backed secu-

rities, structured credit trading and CDOs), and equity income from equity-

linked derivatives and cash equity activity.

(Dollars in millions) 2007 2006

Investment banking income

Advisory fees

$ 446

$ 337

Debt underwriting

1,772

1,824

Equity underwriting

319

315

Total investment banking income

2,537

2,476

Sales and trading revenue

Fixed income:

Liquid products

2,111

2,158

Credit products

(537)

821

Structured products

(5,176)

1,449

Total fixed income

(3,602)

4,428

Equity income

1,298

1,571

Total sales and trading revenue

(2,304)

5,999

Total Capital Markets and Advisory Services

market-based revenue

(1)

$ 233

$8,475

(1) CMAS revenue of $303 million for 2007 consists of market-based revenue of $233 million and $70

million of net interest income on loans for which the fair value option has been elected.

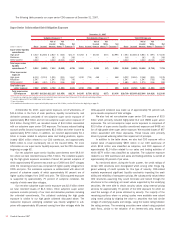

A variety of factors influence results including volume of activity, the

degree in which we successfully anticipate market movements, and how

our hedges perform in the various markets. During the second half of

2007, extreme dislocations emerged in the financial markets, including

leveraged finance, subprime mortgage, and the commercial paper mar-

kets, and these dislocations were further compounded by the decoupling

of typical correlations in the various markets in which we participate.

These conditions created less liquidity, a flight to quality, greater volatility,

widening of credit spreads and a lack of price transparency. Furthermore,

in the fourth quarter of 2007, the credit ratings of certain structured secu-

rities (e.g., CDOs) were downgraded which among other things triggered

further widening of credit spreads for this type of security. We have been

an active participant in the CDO market, maintain ongoing exposure to

these securities and incurred losses associated with these exposures.

Many of these conditions continued into 2008 and it is unclear how long

these conditions and the overall economic slowdown may continue and

what impact they will ultimately have on our results.

CMAS recognized a net loss of $3.4 billion in 2007, a decrease of

$5.0 billion, compared to 2006 driven by a decrease in market-based

revenue of $8.2 billion. The decrease was driven by $5.6 billion of losses

resulting from our CDO exposure and other trading losses. Partially off-

setting this decrease was a reduction in noninterest expense due to lower

performance-based incentive compensation.

Investment banking income increased $61 million to $2.5 billion due

to growth in advisory fees. This growth was driven by increased market

activity primarily in the first half of the year partially offset by reduced debt

underwriting fees that were affected by the market disruptions during the

second half of the year which included the utilization of fees to distribute

leveraged loan commitments.

Sales and trading revenue declined $8.3 billion to a loss of $2.3 bil-

lion in 2007. While structured products and credit products reported

losses for 2007, liquid products and equities compared reasonably well

with 2006 given the market conditions.

ŠLiquid products revenue decreased $47 million as the negative impact

of spread widening and correlations breaking down (e.g., correlation

between certain municipal market indices and bond market swap

spreads) were partially offset by the strength in interest rate products

and foreign exchange contracts.

ŠCredit products losses were $537 million, a decline in revenue of $1.4

billion compared to 2006. Losses resulted from positions taken in the

market as a result of customer market making activities as the widening

of spreads during the second half of the year had a negative impact on

these positions. In addition, certain indices became extremely volatile

and diverged from other related indices and from single name credit risk

(bonds, loans or derivatives) in our portfolio. This negatively impacted

our hedging of portfolios of single name credits with derivatives based

on these indices. One example of this divergence was the widening of

the spread between the investment grade cash and the credit derivative

markets. In addition, losses also resulted from positions taken in the

market as the widening of spreads during the second half of the year

had a negative impact on these positions.

We also incurred losses of $292 million, net of $471 million of fees,

on leveraged loans, loan commitments and the Corporation’s share of

the leveraged forward calendar. Losses incurred on our leveraged

exposure were not concentrated in any one type (senior secured, cove-

nant light or subordinated/senior unsecured) and were generally due to

wider new issuance credit spreads. Since the negotiated spreads were

lower than the then current new issuance spread, a fair value loss

52

Bank of America 2007