Bank of America 2007 Annual Report Download - page 86

Download and view the complete annual report

Please find page 86 of the 2007 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

|

|

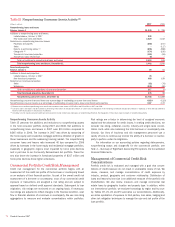

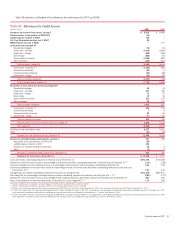

The allowance for loan and lease losses as a percentage of total

loans and leases outstanding was 1.33 percent at December 31, 2007,

compared to 1.28 percent at December 31, 2006. The increase in the

ratio was driven by reserve increases for higher inherent losses in the

small business and home equity portfolios within GCSBB, reflecting growth

of these businesses and deterioration in the portfolios, and seasoning of

the Card Services unsecured lending portfolio as well as discontinuing

sales of new receivables into the unsecured lending trust. These

increases were partially offset by growth in the residential mortgage portfo-

lio, which has a low loss profile, as the Corporation increased retention of

residential mortgage loans for ALM purposes. Also offsetting the increases

were reserve reductions related to the addition of higher loss profile

accounts to the domestic credit card securitization trust and the sales of

our Latin American portfolios and operations.

Reserve for Unfunded Lending Commitments

In addition to the allowance for loan and lease losses, we also estimate

probable losses related to unfunded lending commitments measured at

historical cost, such as letters of credit and financial guarantees, and

binding unfunded loan commitments. Unfunded lending commitments are

subject to the same assessment as funded loans, except utilization

assumptions are considered. The reserve for unfunded lending commit-

ments is included in accrued expenses and other liabilities on the Con-

solidated Balance Sheet with changes to the reserve generally made

through the provision for credit losses.

The reserve for unfunded lending commitments at December 31,

2007 was $518 million, a $121 million increase from December 31,

2006 primarily driven by the acquisition of LaSalle.

84

Bank of America 2007