Bank of America 2007 Annual Report Download - page 73

Download and view the complete annual report

Please find page 73 of the 2007 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

|

|

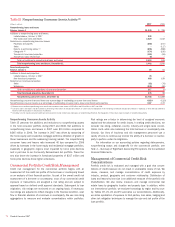

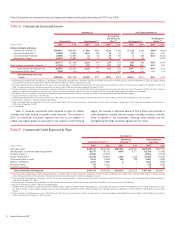

Table 13 Consumer Loans and Leases

December 31 Year Ended December 31

Outstandings Nonperforming

(1, 2)

Accruing Past

Due 90 Days

or More

(3)

Net Charge-

offs/Losses

Net Charge-off/

Loss Ratios

(4)

(Dollars in millions) 2007 2006 2007 2006 2007 2006 2007 2006 2007 2006

Held basis

Residential mortgage

$274,949

$241,181

$1,999

$ 660

$ 237

$ 118

$57

$39

0.02%

0.02%

Credit card – domestic

65,774

61,195

n/a

n/a

1,855

1,991

3,063

3,094

5.29

4.85

Credit card – foreign

14,950

10,999

n/a

n/a

272

184

378

225

3.06

2.46

Home equity

(5)

114,834

87,893

1,340

291

–

–

274

51

0.28

0.07

Direct/Indirect consumer

(5, 6)

76,844

59,378

8

2

745

378

1,373

610

1.95

1.14

Other consumer

(5, 7)

3,850

5,059

95

77

4

7

278

217

6.54

2.97

Total held

551,201

465,705

3,442

1,030

3,113

2,678

5,423

4,236

1.07

1.01

Securitization impact

108,646

110,151

2

2

2,764

2,407

5,003

3,371

4.54

3.22

Total consumer loans and leases – managed

$659,847

$575,856 $3,444 $1,032 $5,877 $5,085 $10,426 $7,607 1.69 1.45

Managed basis

Residential mortgage

$278,733

$245,840

$1,999

$ 660

$ 237

$ 118

$57

$39

0.02%

0.02%

Credit card – domestic

151,862

142,599

n/a

n/a

4,170

3,828

6,960

5,395

4.91

3.89

Credit card – foreign

31,829

27,890

n/a

n/a

714

608

1,254

980

4.24

3.95

Home equity

(5)

115,009

88,202

1,342

293

–

–

274

51

0.28

0.07

Direct/Indirect consumer

(5, 6)

78,564

66,266

8

2

752

524

1,603

925

2.14

1.49

Other consumer

(5, 7)

3,850

5,059

95

77

4

7

278

217

6.54

2.97

Total consumer loans and leases – managed

$659,847

$575,856

$3,444

$1,032

$5,877

$5,085

$10,426

$7,607

1.69

1.45

(1) The definition of nonperforming does not include consumer credit card and consumer non-real estate loans and leases. These loans are charged-off no later than the end of the month in which the account becomes 180 days

past due.

(2) Nonperforming consumer loans and leases as a percentage of outstanding consumer loans and leases were 0.62 percent and 0.22 percent on a held basis, and 0.52 percent and 0.18 percent on a managed basis at

December 31, 2007 and 2006.

(3) Accruing consumer loans and leases past due 90 days or more as a percentage of outstanding consumer loans and leases were 0.57 percent and 0.58 percent on a held basis, and 0.89 percent and 0.88 percent on a

managed basis at December 31, 2007 and 2006.

(4) Net charge-off/loss ratios are calculated as held net charge-offs or managed net losses divided by average outstanding held or managed loans and leases during the year for each loan and lease category.

(5) Home equity loan balances previously included in direct/indirect consumer and other consumer were reclassified to home equity to conform to current year presentation. Additionally, certain foreign consumer balances were

reclassified from other consumer to direct/indirect consumer to conform to current year presentation.

(6) Outstandings include foreign consumer loans of $3.4 billion and $3.9 billion at December 31, 2007 and 2006.

(7) Outstandings include foreign consumer loans of $829 million and $2.3 billion and consumer finance loans of $3.0 billion and $2.8 billion at December 31, 2007 and 2006.

n/a = not applicable

Consumer Credit Portfolio

Table 13 presents our held and managed consumer loans and leases, and

related credit quality information for 2007 and 2006. Overall, consumer

credit quality indicators deteriorated from the favorable levels experienced

in 2006. Weakness in the housing markets resulted in rising credit risk,

most notably in home equity.

Residential Mortgage

The residential mortgage portfolio makes up the largest percentage of our

consumer loan portfolio at 50 percent of held consumer loans and leases

and 42 percent of managed consumer loans and leases at December 31,

2007. Approximately 24 percent of the managed residential portfolio is in

GCSBB and GWIM and represents residential mortgages that are origi-

nated for the home purchase and refinancing needs of our customers. The

remaining portion of the managed portfolio is mostly in All Other, and is

comprised of purchased and originated residential mortgage loans used in

our overall ALM activities.

Residential mortgage loans to borrowers in the state of California

represented 34 percent and 33 percent of total residential mortgage loans

at December 31, 2007 and 2006. The Los Angeles-Long Beach-Santa Ana

MSA within California represented 11 percent of the total residential mort-

gage portfolio at both 2007 and 2006. In addition, residential mortgage

loans to borrowers in the state of Florida represented six percent and

seven percent of the total residential mortgage portfolio at December 31,

2007 and 2006. No single MSA within Florida represented more than 10

percent of the residential mortgage portfolio at December 31, 2007 and

2006. A portion of our credit risk on 68 percent and 56 percent of our

residential mortgage loans in California and Florida was mitigated through

the purchase of credit protection. See Management of Consumer Credit

Risk Concentrations beginning on page 70 for more information.

On a held basis, outstanding loans and leases increased $33.8 bil-

lion at December 31, 2007 compared to 2006 driven by retained mort-

gage production and the acquisition of LaSalle. Nonperforming balances

increased $1.3 billion due to portfolio seasoning reflective of growth in the

business and the impact of the weak housing market. At December 31,

2007 and 2006, loans past due 90 days or more and still accruing inter-

est of $237 million and $118 million were related to repurchases pur-

suant to our servicing agreements with Government National Mortgage

Association (GNMA) mortgage pools where repayments are insured by the

Federal Housing Administration or guaranteed by the Department of Veter-

ans Affairs.

Due to current market conditions, members of the mortgage servicing

industry are evaluating a number of programs for identifying subprime

residential mortgage loan borrowers who are at risk of default and offering

loss mitigation strategies, including repayment plans and loan mod-

ifications, to such borrowers. Generally these programs require that the

borrower and subprime residential mortgage loan meet certain criteria in

order to qualify for a modification. The SEC’s Office of the Chief Account-

ant (OCA) noted that if certain loan modification requirements are met, the

OCA will not object to continued status of the transferee as a QSPE under

SFAS 140. We do not currently originate or service significant subprime

residential mortgage loans, nor do we hold a significant amount of benefi-

cial interests in QSPE securitizations of subprime residential mortgage

loans. We do not expect that the implementation of these programs

will have a significant impact on our financial condition and results of

operations.

Bank of America 2007

71