Bank of America 2007 Annual Report Download - page 72

Download and view the complete annual report

Please find page 72 of the 2007 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

|

|

ple, we have adjusted our underwriting criteria, as well as enhanced our

line management and collection strategies across the consumer busi-

nesses. In the commercial businesses, we have increased the frequency

of portfolio monitoring and are aggressively managing exposure when we

begin to see signs of deterioration.

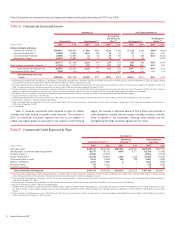

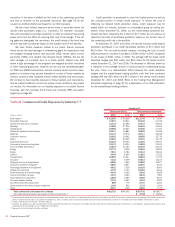

Consumer Portfolio Credit Risk Management

Credit risk management for the consumer portfolio begins with initial under-

writing and continues throughout a borrower’s credit cycle. Statistical

techniques in conjunction with experiential judgment are used in all

aspects of portfolio management including underwriting, product pricing,

risk appetite, setting credit limits, operating processes and metrics to

quantify and balance risks and returns. In addition, credit decisions are

statistically based with tolerances set to decrease the percentage of

approvals as the risk profile increases. Statistical models are built using

detailed behavioral information from external sources such as credit

bureaus and/or internal historical experience. These models are a critical

component of our consumer credit risk management process and are used

in the determination of both new and existing credit decisions, portfolio

management strategies including authorizations and line management,

collection practices and strategies, determination of the allowance for

credit losses, and economic capital allocations for credit risk.

For information on our accounting policies regarding delinquencies,

nonperforming status and charge-offs for the consumer portfolio, see Note

1 – Summary of Significant Accounting Principles to the Consolidated

Financial Statements.

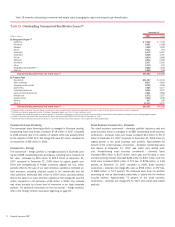

Management of Consumer Credit Risk

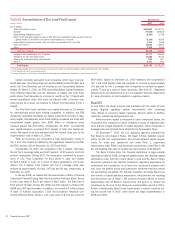

Concentrations

Consumer credit risk is evaluated and managed with a goal that credit

concentrations do not result in undesirable levels of risk. We review,

measure and manage credit exposure in numerous ways such as by prod-

uct and geography in order to achieve the desired mix. Additionally, to

enhance our overall risk management strategy credit protection is pur-

chased on certain portions of our portfolio.

Our consumer loan portfolio in the states of California, Florida, New

York and Texas represented in aggregate 43 percent and 42 percent of

total managed consumer loans at December 31, 2007 and 2006. Our

consumer loan portfolio in the state of California represented approx-

imately 24 percent and 23 percent of total managed consumer loans at

December 31, 2007 and 2006, primarily driven by the consumer real

estate portfolio. Our consumer loan portfolio in the state of Florida is our

second largest concentration and represented approximately eight percent

of total managed consumer loans at both December 31, 2007 and 2006,

primarily driven by the consumer real estate portfolio. New York and Texas

represented six percent and five percent of total managed consumer loans

at both December 31, 2007 and 2006. No state other than California, and

no single Metropolitan Statistical Area (MSA) within California represented

more than 10 percent of the total managed consumer portfolio. No other

single state represented over five percent of total managed consumer

loans.

We have mitigated a portion of our credit risk in our residential mort-

gage loan portfolio by using synthetic securitizations. These agreements

are cash collateralized and will reimburse us in the event that losses

exceed established loss levels. As of December 31, 2007 and 2006,

approximately $140.0 billion and $130.0 billion of mortgage loans were

protected by these agreements. In addition, we have entered into credit

protection agreements with government-sponsored agencies on approx-

imately $33.0 billion and $5.0 billion as of December 31, 2007 and

2006, providing full protection on conforming residential mortgage loans

that become severely delinquent. Our regulatory risk-weighted assets were

reduced as a result of these transactions because we transferred a por-

tion of our credit risk to unaffiliated parties. At December 31, 2007 and

2006, these transactions had the cumulative effect of reducing our risk-

weighted assets by $49.0 billion and $36.4 billion, and resulted in

increases of 27 bps and 30 bps in our Tier 1 Capital ratio at

December 31, 2007 and 2006.

70

Bank of America 2007