Bank of America 2007 Annual Report Download - page 53

Download and view the complete annual report

Please find page 53 of the 2007 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

|

|

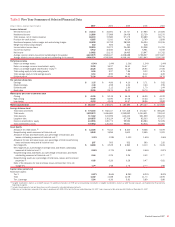

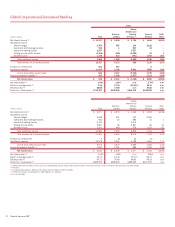

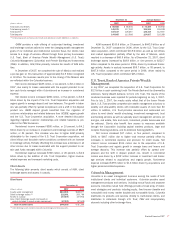

December 31 Average Balance

(Dollars in millions) 2007 2006

2007

2006

Total loans and leases

$324,198

$242,700

$274,015

$232,623

Total trading-related assets

308,315

309,097

362,193

336,860

Total market-based earning assets

(1)

359,730

348,717

412,326

370,187

Total earning assets

(2)

673,552

599,326

676,500

609,100

Total assets

(2)

776,107

685,935

770,360

691,414

Total deposits

246,788

212,028

220,724

194,972

(1) Total market-based earning assets represents earning assets included in CMAS but excludes loans for which the fair value option has been elected.

(2) Total earning assets and total assets include asset allocations to match liabilities (i.e., deposits).

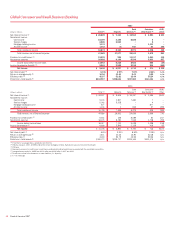

GCIB provides a wide range of financial services to both our issuer

and investor clients that range from business banking clients to large

international corporate and institutional investor clients using a strategy to

deliver value-added financial products and advisory solutions. GCIB’s

products and services are delivered from three primary businesses: Busi-

ness Lending, CMAS, and Treasury Services, and are provided to our cli-

ents through a global team of client relationship managers and product

partners. In addition, ALM/Other includes the results of ALM activities and

other GCIB activities (e.g., Commercial Insurance business which was sold

in the fourth quarter of 2007). Our clients are supported through offices in

22 countries that are divided into four distinct geographic regions: U.S.

and Canada; Asia; Europe, Middle East, and Africa; and Latin America. For

more information on our foreign operations, see Foreign Portfolio beginning

on page 81.

Effective January 1, 2007, the Corporation adopted SFAS 159 and

elected to account for loans and loan commitments to certain large corpo-

rate clients at fair value. For more information on the adoption of SFAS

159, see Note 19 – Fair Value Disclosures to the Consolidated Financial

Statements and see page 74 for a discussion of loans and loan commit-

ments measured at fair value in accordance with SFAS 159. The results of

loans and loan commitments to certain large corporate clients for which

the Corporation elected the fair value option (including the associated risk

mitigation tools) are recorded in CMAS.

Net income decreased $5.5 billion, or 91 percent, to $538 million and

total revenue decreased $7.7 billion, or 37 percent, to $13.4 billion in

2007 compared to 2006. These decreases were driven by $5.6 billion of

losses resulting from our CDO exposure and other trading losses. Addition-

ally, we experienced increases in provision for credit losses and noninterest

expense, which were partially offset by an increase in net interest income.

Net interest income increased $1.3 billion, or 14 percent, due to

higher market-based net interest income of $1.1 billion and the FTE

impact of a one-time tax benefit from restructuring our existing non-U.S.

based commercial aircraft leasing business. Additionally, the benefit of

growth in average loans and leases of $41.4 billion, or 18 percent, was

partially offset by spread compression on core lending and deposit-related

activities, and a change in the mix between interest-bearing and

noninterest-bearing deposits as clients maintained lower noninterest-

bearing compensating balances by shifting to interest bearing and/or

higher yielding investment alternatives. The growth in average loans and

average deposits was due to organic growth as well as the LaSalle merger.

Noninterest income decreased $9.1 billion, or 81 percent, in 2007

compared to 2006, driven by declines in trading account profits (losses) of

$8.1 billion and all other income of $1.1 billion. For more information on

these decreases, see the CMAS discussion.

Provision for credit losses was $652 million in 2007 compared to $9

million in 2006. The increase was driven by the absence of 2006 releases

of reserves, higher net charge-offs and an increase in reserves during

2007 reflecting the impact of the weak housing market particularly on the

homebuilder loan portfolio. Net charge-offs increased in the retail automo-

tive and other dealer-related portfolios due to growth, seasoning and

deterioration, as well as from a lower level of commercial recoveries.

Noninterest expense increased $347 million, or three percent, mainly

due to the addition of LaSalle and Visa-related litigation costs, equally

allocated to Treasury Services and Card Services on a management

accounting basis, partially offset by a reduction in performance-based

incentive compensation in CMAS. For additional information on Visa-

related litigation, see Note 13 – Commitments and Contingencies to the

Consolidated Financial Statements.

Business Lending

Business Lending provides a wide range of lending-related products and

services to our clients through client relationship teams along with various

product partners. Products include commercial and corporate bank loans

and commitment facilities which cover our business banking clients, mid-

dle market commercial clients and our large multinational corporate cli-

ents. Real estate lending products are issued primarily to public and

private developers, homebuilders and commercial real estate firms. Leas-

ing and asset-based lending products offer our clients innovative financing

solutions. Products also include indirect consumer loans which allow us to

offer financing through automotive, marine, motorcycle and recreational

vehicle dealerships across the U.S. Business Lending also contains the

results for the economic hedging of our risk to certain credit counter-

parties utilizing various risk mitigation tools.

Net income decreased $128 million, or six percent, to $2.1 billion in

2007 compared to 2006 as increases in net interest income and non-

interest income were more than offset by increases in provision for credit

losses and noninterest expense. Net interest income increased $445 mil-

lion, or 10 percent, driven by the FTE impact of approximately $350 million

related to a one-time tax benefit from restructuring our existing non-U.S.

based commercial aircraft leasing business, and average loan growth of

14 percent. These increases were partially offset by the impact of spread

compression on the loan portfolio. The increase in average loans and

leases was attributable to growth in commercial loans, the LaSalle merger

and increases in the indirect consumer loan portfolio related to bulk pur-

chases of retail automotive loans. The increase in noninterest income of

$112 million, or 11 percent, was driven by improved economic hedging

results of our exposures to certain large corporate clients and higher tax

credits from community development activities partially offset by derivative

fair value adjustments related to an option to purchase retail automotive

loans.

Provision for credit losses was $647 million in 2007 compared to

negative $2 million in 2006. The increase was driven by the absence of

2006 releases of reserves related to favorable commercial credit market

conditions, higher net charge-offs and an increase in reserves during 2007

reflecting the impact of the weak housing market particularly on the home-

builder loan portfolio. Net charge-offs increased in 2007 as retail automo-

tive and other dealer-related portfolio losses rose due to growth,

Bank of America 2007

51