Bank of America 2007 Annual Report Download - page 137

Download and view the complete annual report

Please find page 137 of the 2007 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

|

|

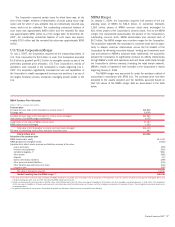

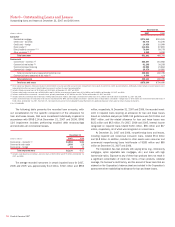

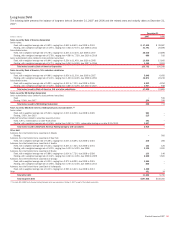

Note 7 – Allowance for Credit Losses

The following table summarizes the changes in the allowance for credit losses for 2007, 2006 and 2005.

(Dollars in millions) 2007 2006 2005

Allowance for loan and lease losses, January 1

$ 9,016

$ 8,045 $ 8,626

Adjustment due to the adoption of SFAS 159

(32)

––

LaSalle balance, October 1, 2007

725

––

U.S. Trust Corporation balance, July 1, 2007

25

––

MBNA balance, January 1, 2006 – 577 –

Loans and leases charged off

(7,730)

(5,881) (5,794)

Recoveries of loans and leases previously charged off

1,250

1,342 1,232

Net charge-offs

(6,480)

(4,539) (4,562)

Provision for loan and lease losses

8,357

5,001 4,021

Other

(23)

(68) (40)

Allowance for loan and lease losses, December 31

11,588

9,016 8,045

Reserve for unfunded lending commitments, January 1

397

395 402

Adjustment due to the adoption of SFAS 159

(28)

––

LaSalle balance, October 1, 2007

124

––

Provision for unfunded lending commitments

28

9 (7)

Other

(3)

(7) –

Reserve for unfunded lending commitments, December 31

518

397 395

Allowance for credit losses, December 31

$12,106

$ 9,413 $ 8,440

Note 8 – Securitizations

The Corporation securitizes loans which may be serviced by the Corpo-

ration or by third parties. With each securitization, the Corporation may

retain all or a portion of the securities, subordinated tranches, interest-

only strips, subordinated interests in accrued interest and fees on the

securitized receivables, and, in some cases, cash reserve accounts, all of

which are called retained interests. These retained interests are recorded

in other assets and/or AFS debt securities and are carried at fair value or

amounts that approximate fair value with changes recorded in income or

accumulated OCI. Changes in the fair value for credit card-related interest-

only strips are recorded in card income.

Mortgage-related Securitizations

The Corporation securitizes a portion of its residential mortgage loan origi-

nations in conjunction with or shortly after loan closing. In addition, the

Corporation may, from time to time, securitize commercial mortgages and

first residential mortgages that it originates or purchases from other enti-

ties. In 2007 and 2006, the Corporation converted a total of $84.5 billion

(including $13.2 billion originated by other entities) and $70.4 billion

(including $20.4 billion originated by other entities), of commercial mort-

gages and first residential mortgages into mortgage-backed securities

issued through Fannie Mae, Freddie Mac, GNMA, Bank of America, N.A.

and Banc of America Mortgage Securities. At December 31, 2007 and

2006, the Corporation retained $9.2 billion (including $3.3 billion issued

prior to 2007) and $5.5 billion (including $4.2 billion issued prior to 2006)

of securities that were valued using quoted market prices. In addition, the

Corporation retained securities, including residual interests, which totaled

$196 million and $224 million at December 31, 2007 and 2006 and are

classified in trading account assets, with changes in fair value recorded in

earnings.

In 2007, the Corporation reported $633 million in gains on loans

converted into securities and sold, of which gains of $584 million were

from loans originated by the Corporation and $49 million were from loans

originated by other entities. In 2006, the Corporation reported $357 mil-

lion in gains on loans converted into securities and sold, of which gains of

$329 million were from loans originated by the Corporation and $28 mil-

lion were from loans originated by other entities. At December 31, 2007

and 2006, the Corporation had recourse obligations of $150 million and

$412 million with varying terms up to seven years on loans that had been

securitized and sold.

In 2007 and 2006, the Corporation purchased $18.1 billion and

$17.4 billion of mortgage-backed securities from third parties and

resecuritized them. Net gains, which include net interest income earned

during the holding period, totaled $13 million and $25 million. At

December 31, 2007, the Corporation retained $540 million of the secu-

rities issued in these transactions. At December 31, 2006, the Corpo-

ration did not retain any securities issued in these transactions.

The Corporation has retained MSRs from the sale or securitization of

mortgage loans. Servicing fee and ancillary fee income on all mortgage

loans serviced, including securitizations, was $810 million and $775 mil-

lion in 2007 and 2006. For more information on MSRs, see Note

21 – Mortgage Servicing Rights to the Consolidated Financial Statements.

Due to current market conditions, members of the mortgage servicing

industry are evaluating a number of programs for identifying subprime

residential mortgage loan borrowers who are at risk of default and offering

loss mitigation strategies, including repayment plans and loan mod-

ifications, to such borrowers. Generally these programs require that the

borrower and subprime residential mortgage loan meet certain criteria in

order to qualify for a modification. The SEC’s Office of the Chief Account-

ant (OCA) noted that if certain loan modification requirements are met, the

OCA will not object to continued status of the transferee as a QSPE under

SFAS 140. The Corporation does not currently originate or service sig-

nificant subprime residential mortgage loans, nor does it hold a significant

amount of beneficial interests in QSPE securitizations of subprime resi-

dential mortgage loans. The Corporation does not expect that the

implementation of these programs will have a significant impact on its

financial condition and results of operations.

Bank of America 2007

135