Bank of America 2007 Annual Report Download - page 76

Download and view the complete annual report

Please find page 76 of the 2007 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

|

|

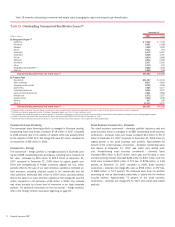

Table 15 Nonperforming Consumer Assets Activity (1)

(Dollars in millions) 2007 2006

Nonperforming loans and leases

Balance, January 1

$1,030

$ 785

Additions to nonperforming loans and leases:

LaSalle balance, October 1, 2007

232

–

New nonaccrual loans and leases

3,829

1,432

Reductions in nonperforming loans and leases:

Paydowns and payoffs

(260)

(157)

Sales

–

(117)

Returns to performing status

(2)

(855)

(698)

Charge-offs

(3)

(374)

(150)

Transfers to foreclosed properties

(152)

(65)

Transfers to loans held-for-sale

(8)

–

Total net additions to nonperforming loans and leases

2,412

245

Total nonperforming loans and leases, December 31

3,442

1,030

Foreclosed properties

Balance, January 1

59

61

Additions to foreclosed properties:

LaSalle balance, October 1, 2007

70

–

New foreclosed properties

468

159

Reductions in foreclosed properties:

Sales

(82)

(76)

Writedowns

(239)

(85)

Total net additions to (reductions in) foreclosed properties

217

(2)

Total foreclosed properties, December 31

276

59

Nonperforming consumer assets, December 31

$3,718

$1,089

Nonperforming consumer loans and leases as a percentage of outstanding consumer loans and leases

0.62%

0.22%

Nonperforming consumer assets as a percentage of outstanding consumer loans, leases and foreclosed properties

0.67

0.23

(1) Balances do not include nonperforming loans held-for-sale included in other assets of $95 million and $30 million in 2007 and 2006.

(2) Consumer loans and leases may be restored to performing status when all principal and interest is current and full repayment of the remaining contractual principal and interest is expected, or when the loan otherwise

becomes well-secured and is in the process of collection.

(3) Our policy is not to classify consumer credit card and consumer non-real estate loans and leases as nonperforming; therefore, the charge-offs on these loans have no impact on nonperforming activity.

Nonperforming Consumer Assets Activity

Table 15 presents the additions and reductions to nonperforming assets

in the held consumer portfolio during 2007 and 2006. Net additions to

nonperforming loans and leases in 2007 were $2.4 billion compared to

$245 million in 2006. The increase in 2007 was driven by seasoning of

the home equity and residential mortgage portfolios reflective of growth in

these businesses and the weakening housing market. The nonperforming

consumer loans and leases ratio increased 40 bps compared to 2006

driven by increases in the home equity and residential mortgage portfolios,

especially in geographic regions most impacted by home price declines

and in part due to our Community Reinvestment Act portfolio. These fac-

tors also drove the increase in foreclosed properties of $217 million and

home price declines drove higher writedowns.

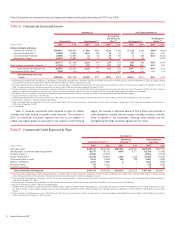

Commercial Portfolio Credit Risk Management

Credit risk management for the commercial portfolio begins with an

assessment of the credit risk profile of the borrower or counterparty based

on an analysis of their financial position. As part of the overall credit risk

assessment of a borrower or counterparty, most of our commercial credit

exposure or transactions are assigned a risk rating and are subject to

approval based on defined credit approval standards. Subsequent to loan

origination, risk ratings are monitored on an ongoing basis. If necessary,

risk ratings are adjusted to reflect changes in the financial condition, cash

flow or financial situation of a borrower or counterparty. We use risk rating

aggregations to measure and evaluate concentrations within portfolios.

Risk ratings are a factor in determining the level of assigned economic

capital and the allowance for credit losses. In making credit decisions, we

consider risk rating, collateral, country, industry and single name concen-

tration limits while also balancing the total borrower or counterparty rela-

tionship. Our lines of business and risk management personnel use a

variety of tools to continuously monitor the ability of a borrower or counter-

party to perform under its obligations.

For information on our accounting policies regarding delinquencies,

nonperforming status and charge-offs for the commercial portfolio, see

Note 1 – Summary of Significant Accounting Principles to the Consolidated

Financial Statements.

Management of Commercial Credit Risk

Concentrations

Portfolio credit risk is evaluated and managed with a goal that concen-

trations of credit exposure do not result in undesirable levels of risk. We

review, measure, and manage concentrations of credit exposure by

industry, product, geography and customer relationship. Distribution of

loans and leases by loan size is an additional measure of the portfolio risk

diversification. We also review, measure, and manage commercial real

estate loans by geographic location and property type. In addition, within

our international portfolio, we evaluate borrowings by region and by coun-

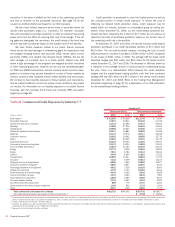

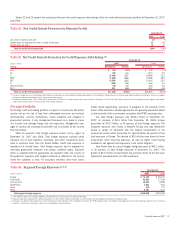

try. Tables 19, 21, 24 and 25 summarize our concentrations. Additionally,

we utilize syndication of exposure to third parties, loan sales, hedging and

other risk mitigation techniques to manage the size and risk profile of the

loan portfolio.

74

Bank of America 2007