Bank of America 2007 Annual Report Download - page 140

Download and view the complete annual report

Please find page 140 of the 2007 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

|

|

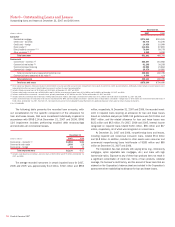

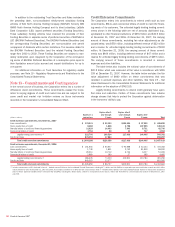

Note 9 – Variable Interest Entities

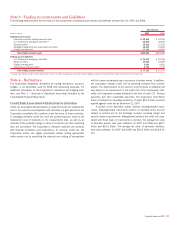

The following table presents total assets of those VIEs in which the Corporation holds a significant variable interest and, in the unlikely event that all of the

assets in the VIEs become worthless, the Corporation’s maximum exposure to loss. The Corporation’s maximum exposure to loss incorporates not only

potential losses associated with assets recorded on the Corporation’s balance sheet but also off-balance sheet commitments, such as unfunded liquidity

and lending commitments and other contractual arrangements.

Consolidated

(1)

Unconsolidated

(Dollars in millions) Total Assets Loss Exposure Total Assets Loss Exposure

Variable interest entities, December 31, 2007

Corporation-sponsored multi-seller conduits

$11,944 $16,984 $29,363 $47,335

Collateralized debt obligation vehicles

4,464 4,311 8,324 7,410

Leveraged lease trusts

6,236 6,236 – –

Other

13,771 12,347 8,260 5,953

Total variable interest entities

$36,415 $39,878 $45,947 $60,698

Variable interest entities, December 31, 2006

Corporation-sponsored multi-seller conduits $ 9,090 $11,515 $18,983 $29,836

Collateralized debt obligation vehicles – – 8,489 7,658

Leveraged lease trusts 8,575 8,575 – –

Other 4,717 3,019 12,709 9,310

Total variable interest entities $22,382 $23,109 $40,181 $46,804

(1) The Corporation consolidates VIEs when it is the primary beneficiary that will absorb the majority of the expected losses or expected residual returns of the VIEs or both.

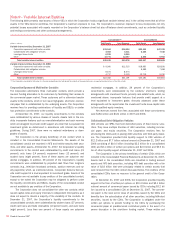

Corporation-Sponsored Multi-seller Conduits

The Corporation administers three multi-seller conduits which provide a

low-cost funding alternative to its customers by facilitating their access to

the commercial paper market. These customers sell or otherwise transfer

assets to the conduits, which in turn issue high-grade, short-term commer-

cial paper that is collateralized by the underlying assets. The Corporation

receives fees for providing combinations of liquidity and SBLCs or similar

loss protection commitments to the conduits.

At December 31, 2007, our liquidity commitments to the conduits

were collateralized by various classes of assets. Assets held in the con-

duits incorporate features such as overcollateralization and cash reserves

which are designed to provide credit support at a level that is equivalent to

investment grade as determined in accordance with internal risk rating

guidelines. During 2007, there were no material write-downs or down-

grades of assets.

The Corporation is the primary beneficiary of one conduit which is

included in the Consolidated Financial Statements. The assets of the

consolidated conduit are recorded in AFS and held-to-maturity debt secu-

rities, and other assets. At December 31, 2007, the Corporation’s liquidity

commitments to the conduit were collateralized by credit card loans (21

percent), auto loans (14 percent), equipment loans (13 percent), and

student loans (eight percent). None of these assets are subprime resi-

dential mortgages. In addition, 29 percent of the Corporation’s liquidity

commitments were collateralized by projected cash flows from long-term

contracts (e.g., television broadcast contracts, stadium revenues and roy-

alty payments) which, as mentioned above, incorporate features that pro-

vide credit support at a level equivalent to investment grade. Assets of the

Corporation are not available to pay creditors of the consolidated conduit,

except to the extent the Corporation may be obligated to perform under

the liquidity commitments and SBLCs. Assets of the consolidated conduit

are not available to pay creditors of the Corporation.

The Corporation does not consolidate the other two conduits which

issued capital notes and equity interests to independent third parties as it

does not expect to absorb a majority of the variability of the conduits. At

December 31, 2007, the Corporation’s liquidity commitments to the

unconsolidated conduits were collateralized by student loans (27 percent),

credit card loans and trade receivables (10 percent each), and auto loans

(eight percent). Less than one percent of these assets are subprime

residential mortgages. In addition, 29 percent of the Corporation’s

commitments were collateralized by the conduits’ short-term lending

arrangements with investment funds, primarily real estate funds, which, as

mentioned above, incorporate features that provide credit support at a

level equivalent to investment grade. Amounts advanced under these

arrangements will be repaid when the investment funds issue capital calls

to their qualified equity investors.

Net revenues earned from fees associated with these commitments

were $184 million and $121 million in 2007 and 2006.

Collateralized Debt Obligation Vehicles

CDO vehicles are SPEs that hold diversified pools of fixed income secu-

rities. They issue multiple tranches of debt securities, including commer-

cial paper, and equity securities. The Corporation receives fees for

structuring the CDOs and/or placing debt securities with third party invest-

ors. The Corporation provided total liquidity support to CDO vehicles of

$12.3 billion and $7.7 billion notional amount at December 31, 2007 and

2006 consisting of $10.0 billion (including $3.2 billion for a consolidated

CDO) and $2.1 billion of written put options and $2.3 billion and $5.5 bil-

lion of other liquidity support at December 31, 2007 and 2006.

The Corporation is the primary beneficiary of certain CDOs which are

included in the Consolidated Financial Statements at December 31, 2007.

Assets held in the consolidated CDOs are classified in trading account

assets and AFS debt securities, including AFS debt securities with a fair

value of $2.8 billion that were principally related to certain assets that

were removed from the CDO conduit discussed below. The creditors of the

consolidated CDOs have no recourse to the general credit of the Corpo-

ration.

At December 31, 2007 and 2006, the Corporation provided liquidity

support in the form of written put options on $10.0 billion and $2.1 billion

notional amount of commercial paper issued by CDOs including $3.2 bil-

lion issued by a consolidated CDO at December 31, 2007. The commer-

cial paper is the most senior class of securities issued by the CDOs and

benefits from the subordination of all other securities, including AAA-rated

securities, issued by the CDOs. The Corporation is obligated under the

written put options to provide funding to the CDOs by purchasing the

commercial paper at predetermined contractual yields in the event of a

severe disruption in the short-term funding market. These written put

138

Bank of America 2007