Bank of America 2007 Annual Report Download - page 82

Download and view the complete annual report

Please find page 82 of the 2007 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

|

|

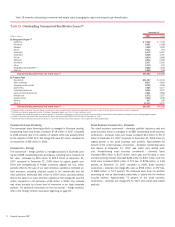

securities. In the case of default we first look to the underlying securities

and then to recovery on the purchased insurance. See page 53 for dis-

cussion on credit protection purchased on our CDO exposure.

We also have indirect exposure as we invest in securities where the

issuers have purchased wraps (i.e., insurance). For example, municipal-

ities and corporations purchase protection in order to enhance their pricing

power which has the effect of reducing their cost of borrowings. If the rat-

ing agencies downgrade the monolines, the credit rating of the bond may

fall and may have an adverse impact on the market value of the security.

We have further exposure related to our public finance business

where we are the lead manager or remarketing agent for transactions that

are wrapped including auction rate securities (ARS), tender option munici-

pal bonds (TOBs), and variable rate demand bonds (VRDBs). We are the

lead manager on municipal and, to a lesser extent, student loan ARS

where a high percentage of the programs are wrapped by either monolines

or other financial guarantors. However, we are only the remarketing agent

on TOBs and VRDBs transactions. Recent concerns about monoline down-

grades or insolvency has caused disruptions in each of these markets as

investor concerns have impacted overall market liquidity and bond prices.

We continue to have liquidity exposure to these markets and instruments,

and as market conditions continue to evolve, these conditions may impact

our results. For information on our liquidity exposure to our public finance

business, see the municipal bond trusts and corporate SPEs discussion

beginning on page 62.

Credit protection is purchased to cover the funded portion as well as

the unfunded portion of certain credit exposure. To lessen the cost of

obtaining our desired credit protection levels, credit exposure may be

added within an industry, borrower or counterparty group by selling pro-

tection. Since December 31, 2006, our net credit default protection pur-

chased has been reduced by $1.1 billion to $7.1 billion as we continue to

reposition the level of purchased protection based on our current view of

the underlying credit risk in the portfolio.

At December 31, 2007 and 2006, we had net notional credit default

protection purchased in our credit derivatives portfolio of $7.1 billion and

$8.3 billion. The net mark-to-market impacts, including the cost of credit

default protection, resulted in net gains of $160 million in 2007 compared

to net losses of $241 million in 2006. The average VAR for these credit

derivative hedges was $22 million and $54 million for the twelve months

ended December 31, 2007 and 2006. The decrease in VAR was driven by

a reduction in the average amount of credit protection outstanding during

the year. There is a diversification effect between the credit derivative

hedges and the market-based trading portfolio such that their combined

average VAR was $55 million and $57 million for the twelve months ended

December 31, 2007 and 2006. Refer to the Trading Risk Management

discussion beginning on page 87 for a description of our VAR calculation

for the market-based trading portfolio.

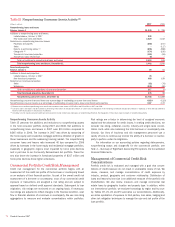

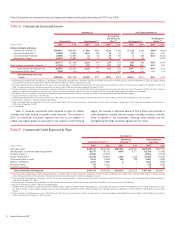

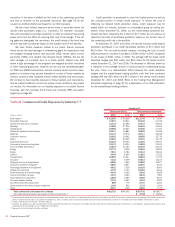

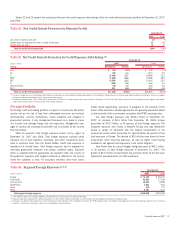

Table 21 Commercial Credit Exposure by Industry (1, 2)

December 31

Commercial Utilized Total Commercial Committed

(Dollars in millions) 2007 2006 2007 2006

Real estate

(3)

$ 81,260

$ 49,259

$111,742

$ 73,544

Diversified financials

37,872

24,813

86,118

67,038

Government and public education

31,743

22,495

57,437

39,254

Retailing

33,280

27,226

55,184

44,064

Capital goods

25,908

16,830

52,356

37,363

Healthcare equipment and services

24,337

15,881

40,962

31,189

Materials

22,176

15,978

38,717

28,789

Consumer services

23,382

19,191

38,650

32,734

Banks

21,261

26,405

35,323

36,735

Individuals and trusts

22,323

18,792

32,425

29,167

Commercial services and supplies

21,175

15,224

31,858

23,532

Food, beverage and tobacco

13,919

11,384

25,701

21,124

Energy

12,772

9,505

23,510

18,460

Media

7,901

8,784

19,343

19,181

Utilities

6,438

6,624

19,281

17,222

Transportation

12,803

11,637

18,824

17,375

Insurance

7,162

6,759

16,014

14,122

Religious and social organizations

8,208

7,840

10,982

10,507

Consumer durables and apparel

5,802

4,827

10,907

9,124

Technology hardware and equipment

4,615

3,326

10,239

8,093

Software and services

4,739

2,763

10,128

6,212

Pharmaceuticals and biotechnology

4,349

2,530

8,563

6,289

Telecommunication services

3,475

3,565

8,235

7,981

Automobiles and components

2,648

1,584

6,960

5,153

Food and staples retailing

2,732

2,153

5,318

4,222

Household and personal products

889

779

2,776

2,264

Semiconductors and semiconductor equipment

1,140

802

1,734

1,364

Other

8,407

7,346

8,505

7,775

Total commercial credit exposure by industry

$452,716

$344,302

$787,792

$619,877

Net credit default protection purchased on total commitments

(4)

$ (7,146)

$ (8,260)

(1) Total commercial utilized and total commercial committed exposure includes loans and letters of credit measured at fair value in accordance with SFAS 159 and are comprised of loans outstanding of $4.59 billion and issued

letters of credit at notional value of $1.1 billion at December 31, 2007. In addition, total commercial committed exposure includes unfunded loan commitments at notional value of $19.8 billion at December 31, 2007.

(2) Includes small business commercial – domestic exposure.

(3) Industries are viewed from a variety of perspectives to best isolate the perceived risks. For purposes of this table, the real estate industry is defined based upon the borrowers’ or counterparties’ primary business activity using

operating cash flow and primary source of repayment as key factors.

(4) Represents net notional credit protection purchased.

80

Bank of America 2007