Bank of America 2007 Annual Report Download - page 171

Download and view the complete annual report

Please find page 171 of the 2007 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179

|

|

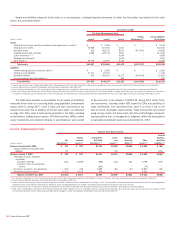

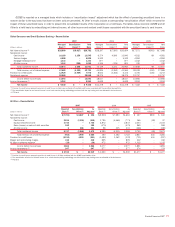

Note 22 – Business Segment Information

The Corporation reports the results of its operations through three busi-

ness segments: Global Consumer and Small Business Banking (GCSBB),

Global Corporate and Investment Banking (GCIB) and Global Wealth and

Investment Management (GWIM). The Corporation may periodically

reclassify business segment results based on modifications to its

management reporting methodologies and changes in organizational

alignment.

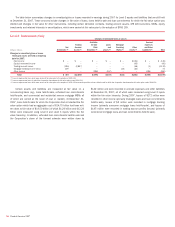

Global Consumer and Small Business Banking

GCSBB provides a diversified range of products and services to individuals

and small businesses. The Corporation reports GCSBB’s results, specifi-

cally credit card, business card and certain unsecured lending portfolios,

on a managed basis. This basis of presentation excludes the Corpo-

ration’s securitized mortgage and home equity portfolios for which the

Corporation retains servicing. Reporting on a managed basis is consistent

with the way that management evaluates the results of GCSBB. Managed

basis assumes that securitized loans were not sold and presents earnings

on these loans in a manner similar to the way loans that have not been

sold (i.e., held loans) are presented. Loan securitization is an alternative

funding process that is used by the Corporation to diversify funding sour-

ces. Loan securitization removes loans from the Consolidated Balance

Sheet through the sale of loans to an off-balance sheet QSPE which is

excluded from the Corporation’s Consolidated Financial Statements in

accordance with GAAP.

The performance of the managed portfolio is important in under-

standing GCSBB’s results as it demonstrates the results of the entire

portfolio serviced by the business. Securitized loans continue to be serv-

iced by the business and are subject to the same underwriting standards

and ongoing monitoring as held loans. In addition, retained excess servic-

ing income is exposed to similar credit risk and repricing of interest rates

as held loans. GCSBB’s managed income statement line items differ from

a held basis as follows:

ŠManaged net interest income includes GCSBB’s net interest income on

held loans and interest income on the securitized loans less the

internal funds transfer pricing allocation related to securitized loans.

ŠManaged noninterest income includes GCSBB’s noninterest income on

a held basis less the reclassification of certain components of card

income (e.g., excess servicing income) to record managed net interest

income and provision for credit losses. Noninterest income, both on a

held and managed basis, also includes the impact of adjustments to

the interest-only strip that are recorded in card income as management

continues to manage this impact within GCSBB.

ŠProvision for credit losses represents the provision for credit losses on

held loans combined with realized credit losses associated with the

securitized loan portfolio.

Global Corporate and Investment Banking

GCIB provides a wide range of financial services to both the Corporation’s

issuer and investor clients that range from business banking clients to

large international corporate and institutional investor clients using a

strategy to deliver value-added financial products and advisory solutions.

Global Wealth and Investment Management

GWIM offers investment and brokerage services, estate management,

financial planning services, fiduciary management, credit and banking

expertise, and diversified asset management products to institutional cli-

ents, as well as affluent and high net-worth individuals. GWIM also

includes the impact of migrated qualifying affluent customers, including

their related deposit balances, from GCSBB. After migration, the asso-

ciated net interest income, service charges and noninterest expense on

the deposit balances are recorded in GWIM.

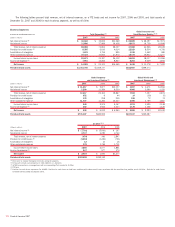

All Other

All Other consists of equity investment activities including Principal Inves-

ting, Corporate Investments and Strategic Investments, the residual

impact of the allowance for credit losses and the cost allocation proc-

esses, merger and restructuring charges, intersegment eliminations, and

the results of certain businesses that are expected to be or have been

sold or are in the process of being liquidated (e.g., the Corporation’s

Brazilian operations, Asia Commercial Banking business and operations in

Chile and Uruguay). All Other also includes certain amounts associated

with ALM activities, including the residual impact of funds transfer pricing

allocation methodologies, amounts associated with the change in the

value of derivatives used as economic hedges of interest rate and foreign

exchange rate fluctuations that did not qualify for SFAS 133 hedge

accounting treatment, foreign exchange rate fluctuations related to SFAS

52 revaluation of foreign-denominated debt issuances, certain gains

(losses) on sales of whole mortgage loans, and gains (losses) on sales of

debt securities. All Other also includes adjustments to noninterest income

and income tax expense to remove the FTE impact of items (primarily low-

income housing tax credits) that have been grossed up within noninterest

income to a FTE amount in the business segments. In addition, GCSBB is

reported on a managed basis which includes a “securitization impact”

adjustment which has the effect of assuming that loans that have been

securitized were not sold and presenting these loans in a manner similar

to the way loans that have not been sold are presented. All Other’s results

include a corresponding “securitization offset” which removes the impact

of these securitized loans in order to present the consolidated results of

the Corporation on a GAAP basis (i.e., held basis).

Basis of Presentation

Total revenue, net of interest expense, includes net interest income on a

FTE basis and noninterest income. The adjustment of net interest income

to a FTE basis results in a corresponding increase in income tax expense.

The net interest income of the businesses includes the results of a funds

transfer pricing process that matches assets and liabilities with similar

interest rate sensitivity and maturity characteristics. Net interest income of

the business segments also includes an allocation of net interest income

generated by the Corporation’s ALM activities.

Certain expenses not directly attributable to a specific business

segment are allocated to the segments based on predetermined means.

The most significant of these expenses include data processing costs,

item processing costs and certain centralized or shared functions. Data

processing costs are allocated to the segments based on equipment

usage. Item processing costs are allocated to the segments based on the

volume of items processed for each segment. The costs of certain central-

ized or shared functions are allocated based on methodologies which

reflect utilization.

Bank of America 2007

169