Bank of America 2007 Annual Report Download - page 77

Download and view the complete annual report

Please find page 77 of the 2007 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

|

|

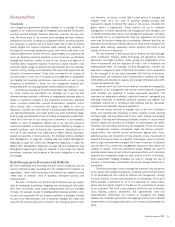

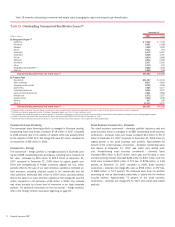

From the perspective of portfolio risk management, customer concen-

tration management is most relevant in GCIB. Within that segment’s Busi-

ness Lending and CMAS businesses, we facilitate bridge financing (high

grade debt, high yield debt, CMBS and equity) to fund acquisitions, recapi-

talizations and other short-term needs as well as provide syndicated

financing for our clients. These concentrations are managed in part

through our established “originate to distribute” strategy. These client

transactions are sometimes large and leveraged. They can also have a

higher degree of risk as we are providing offers or commitments for vari-

ous components of the clients’ capital structures, including lower rated

unsecured and subordinated debt tranches and/or equity. In many cases,

these offers to finance will not be accepted. If accepted, these conditional

commitments are often retired prior to or shortly following funding via the

placement of securities, syndication or the client’s decision to terminate.

Where we have a binding commitment and there is a market disruption or

other unexpected event, there may be heightened exposure in the portfo-

lios and forward calendar, and a higher potential for writedown or loss

unless the terms of the commitment can be modified and/or an orderly

disposition of the exposure can be made.

The Corporation’s share of the leveraged finance and CMBS forward

calendars were $12.2 billion and $2.0 billion, respectively, at

December 31, 2007. Funded leveraged finance and CMBS exposure

included in assets held-for-sale totaled $6.1 billion and $13.7 billion at

December 31, 2007. The funded CMBS exposure includes amounts

assumed with the acquisition of LaSalle. The funded CMBS debt consisted

of $6.9 billion of floating-rate acquisition related financings to major, well

known operating companies. In addition, of the CMBS forward calendar,

$1.1 billion were floating-rate acquisition related financings. Writedowns

were taken on both funded and forward calendar commitments to reflect

the current market prices, if available, or the estimated price at which the

exposures could be distributed in the market. In the first quarter of 2008

the leveraged finance markets began to experience disruptions similar to

those experienced in the second half of 2007 and it is unclear what

impact these conditions will have on our results.

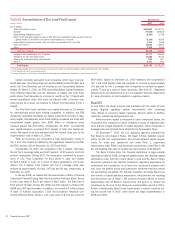

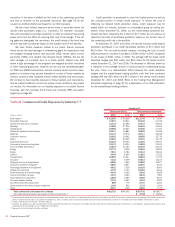

Prior to January 1, 2007, the Corporation accounted for all loans in

the held-to-maturity portfolio on a historical cost basis and incurred losses

on this portfolio were charged against the allowance for loan and lease

losses. Effective January 1, 2007, the Corporation elected to account for

certain large corporate loans and loan commitments (including issued but

unfunded letters of credit which are considered utilized for credit risk

management purposes), which exceed the Corporation’s single name

credit risk concentration guidelines at fair value in accordance with SFAS

159.

The Corporation initially adopted the fair value option for $4.0 billion

of outstanding commercial loans as of January 1, 2007 and recorded

pre-tax net losses of $21 million (net of adjustments related to the allow-

ance for loan and lease losses and direct loan origination fees and costs)

representing the excess of carrying value over fair value of the funded

loans, with the after-tax amount recorded in retained earnings. The Corpo-

ration also initially adopted the fair value option for $21.1 billion of

unfunded commercial commitments, including letters of credit, as of Jan-

uary 1, 2007, and recorded pre-tax net losses of $321 million (net of

associated adjustments related to the reserve for unfunded lending com-

mitments) representing the difference between the carrying value and the

fair value of the unfunded lending commitments, with the after-tax amount

recorded in retained earnings.

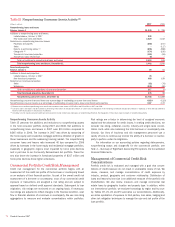

After the initial application of SFAS 159, any fair value adjustment

upon origination and subsequent changes in the fair value of loans and

unfunded commitments is recorded in other income. By including the

credit risk of the borrower in the fair value adjustments, any credit deterio-

ration or improvement is recorded immediately as part of the fair value

adjustment. As a result, the allowance for loan and lease losses and the

reserve for unfunded lending commitments are no longer used to capture

credit losses inherent in these nonperforming or impaired loans and

unfunded commitments. The remaining Commercial Credit Portfolio tables

have been modified to exclude loans and unfunded commitments that are

carried at fair value and to adjust certain ratios for this accounting change.

See Note 19 – Fair Value Disclosures to the Consolidated Financial

Statements for additional information on the adoption of SFAS 159.

At December 31, 2007, outstanding commercial loans measured at

fair value had an aggregate fair value of $4.59 billion recorded in loans

and leases and included commercial – domestic loans of $3.50 billion,

commercial – foreign loans of $790 million and commercial real estate

loans of $304 million. The Corporation recorded net losses of $139 mil-

lion in other income resulting from changes in the fair value of the loan

portfolio during 2007.

In addition, unfunded lending commitments and letters of credit had

an aggregate fair value of $660 million and were recorded in accrued

expenses and other liabilities. The December 31, 2007 aggregate notional

amount of unfunded lending commitments and letters of credit subject to

fair value treatment was $20.9 billion. Net losses resulting from changes

in fair value of commitments and letters of credit of $274 million were

recorded in other income during 2007.

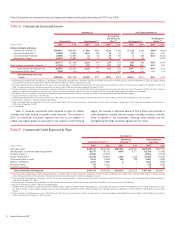

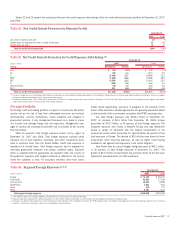

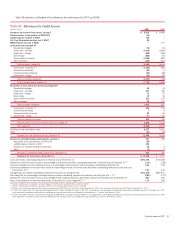

Commercial Credit Portfolio

Commercial credit quality indicators deteriorated from favorable levels

experienced in 2006, in part attributable to the weakness in the housing

and financial markets. The loans and leases net charge-off ratio increased

to 0.40 percent from 0.13 percent a year ago. The increase was princi-

pally attributable to seasoning and deterioration in our small business

portfolio in GCSBB as well as a lower level of commercial recoveries in

GCIB and GWIM. Excluding small business commercial – domestic the

total commercial net charge-off ratio was 0.08 percent compared to a net

recovery ratio of 0.03 percent in 2006, primarily due to a lower level of

recoveries in 2007. The nonperforming loan and commercial utilized criti-

cized exposure ratios were 0.67 percent and 4.17 percent at

December 31, 2007 compared to 0.31 percent and 2.20 percent at

December 31, 2006, mostly related to the addition of LaSalle and

exposure to the homebuilder and mortgage lender sectors.

Bank of America 2007

75