Bank of America 2007 Annual Report Download - page 164

Download and view the complete annual report

Please find page 164 of the 2007 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

-

176

-

177

-

178

-

179

|

|

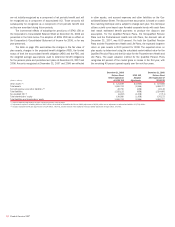

Note 19 – Fair Value Disclosures

Effective January 1, 2007, the Corporation adopted SFAS 157, which pro-

vides a framework for measuring fair value under GAAP. SFAS 157 also

eliminated the deferral of gains and losses at inception of certain

derivative contracts whose fair value was not evidenced by market

observable data. SFAS 157 requires that the impact of this change in

accounting for derivative contracts be recorded as an adjustment to begin-

ning retained earnings in the period of adoption.

The Corporation also adopted SFAS 159 on January 1, 2007. SFAS

159 allows an entity the irrevocable option to elect fair value for the initial

and subsequent measurement for certain financial assets and liabilities

on a contract-by-contract basis. The Corporation elected to adopt the fair

value option for certain financial instruments on the adoption date. SFAS

159 requires that the difference between the carrying value before election

of the fair value option and the fair value of these instruments be recorded

as an adjustment to beginning retained earnings in the period of adoption.

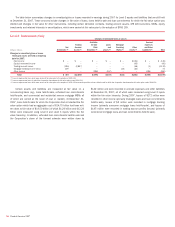

The following table summarizes the impact of the change in account-

ing for derivative contracts described above and the impact of adopting the

fair value option for certain financial instruments on January 1, 2007.

Amounts shown represent the carrying value of the affected instruments

before and after the changes in accounting resulting from the adoption of

SFAS 157 and SFAS 159.

Transition Impact

(Dollars in millions)

Ending Balance

Sheet

December 31, 2006

Adoption Net

Gain/(Loss)

Opening Balance

Sheet

January 1, 2007

Impact of adopting SFAS 157

Net derivative assets and liabilities

(1)

$7,100 $ 22 $7,122

Impact of electing the fair value option under SFAS 159

Loans and leases

(2)

3,968 (21) 3,947

Accrued expenses and other liabilities

(3)

(28) (321) (349)

Other assets

(4)

8,778 – 8,778

Available-for-sale debt securities

(5)

3,692 – 3,692

Federal funds sold and securities purchased under agreements to resell

(6)

1,401 (1) 1,400

Interest-bearing deposit liabilities in domestic offices

(7)

(548) 1 (547)

Cumulative-effect adjustment, pre-tax (320)

Tax impact 112

Cumulative-effect adjustment, net-of-tax, decrease to retained earnings $(208)

(1) The transition adjustment reflects the impact of recognizing previously deferred gains and losses as a result of the rescission of certain requirements of EITF 02-3 in accordance with SFAS 157.

(2) Includes loans to certain large corporate clients. The ending balance at December 31, 2006 and the transition adjustment were net of a $32 million reduction in the allowance for loan and lease losses.

(3) The January 1, 2007 balance after adoption represents the fair value of certain unfunded commercial loan commitments. The December 31, 2006 balance prior to adoption represents the reserve for unfunded lending

commitments associated with these commitments.

(4) Other assets include loans held-for-sale. No transition adjustment was recorded for the loans held-for-sale because they were already recorded at fair value pursuant to lower of cost or market accounting.

(5) Changes in fair value of these AFS debt securities resulting from foreign currency exposure, which is the primary driver of fair value for these securities, had previously been hedged by derivatives that qualified for fair value

hedge accounting in accordance with SFAS 133. As a result, there was no transition adjustment. Following the election of the fair value option, these AFS debt securities have been transferred to trading account assets.

(6) Includes structured reverse repurchase agreements that were hedged with derivatives in accordance with SFAS 133.

(7) Includes long-term fixed rate deposits that were economically hedged with derivatives.

Fair Value Option Elections

Corporate Loans and Loan Commitments

The Corporation elected to account for certain large corporate loans and

loan commitments which exceeded the Corporation’s single name credit

risk concentration guidelines at fair value in accordance with SFAS 159.

Lending commitments, both funded and unfunded, are actively managed

and monitored, and, as appropriate, credit risk for these lending relation-

ships may be mitigated through the use of credit derivatives, with the

Corporation’s credit view and market perspectives determining the size

and timing of the hedging activity. These credit derivatives do not meet the

requirements for hedge accounting under SFAS 133 and are therefore car-

ried at fair value with changes in fair value recorded in other income. Elect-

ing the fair value option allows the Corporation to account for these loans

and loan commitments at fair value, which is more consistent with man-

agement’s view of the underlying economics and the manner in which they

are managed. In addition, accounting for these loans and loan commit-

ments at fair value reduces the accounting asymmetry that would other-

wise result from carrying the loans at historical cost and the credit

derivatives at fair value.

Fair values for the loans and loan commitments are based on market

prices, where available, or discounted cash flows using market-based

credit spreads of comparable debt instruments or credit derivatives of the

specific borrower or comparable borrowers. Results of discounted cash

flow calculations may be adjusted, as appropriate, to reflect other market

conditions or the perceived credit risk of the borrower.

At December 31, 2007, funded loans which the Corporation has

elected to fair value had an aggregate fair value of $4.59 billion recorded

in loans and leases and an aggregate outstanding principal balance of

$4.82 billion. At December 31, 2007, unfunded loan commitments that

the Corporation has elected to fair value had an aggregate fair value of

$660 million recorded in accrued expenses and other liabilities and an

aggregate committed exposure of $20.9 billion. Interest income on these

loans is recorded in interest and fees on loans and leases. At

December 31, 2007, none of these loans were 90 days or more past due

and still accruing interest or had been placed on nonaccrual status. Net

losses resulting from changes in fair value of these loans and loan

commitments of $413 million were recorded in other income during 2007.

These losses were significantly attributable to changes in instrument-

specific credit risk. Following adoption of SFAS 159, approximately $5 mil-

lion of direct loan origination fees and costs related to items for which the

fair value option was elected were recognized in earnings during 2007.

Previously, these items would have been capitalized and amortized to

earnings over the life of the loans.

162

Bank of America 2007