Bank of America 2007 Annual Report Download - page 71

Download and view the complete annual report

Please find page 71 of the 2007 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

|

|

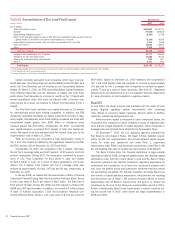

Dividends

In 2007, the Corporation paid cash dividends of $10.7 billion on its

common stock. Effective for the third quarter 2007 dividend, the Board

increased the quarterly cash dividend 14 percent from $0.56 to $0.64 per

share. In October 2007, the Board declared a fourth quarter cash dividend

of $0.64 which was paid on December 28, 2007 to common shareholders

of record on December 7, 2007. In January 2008, the Board authorized a

quarterly cash dividend of $0.64 per common share payable on March 28,

2008 to shareholders of record on March 7, 2008.

In 2007, the Corporation paid a total of $182 million in cash divi-

dends on its various series of preferred stock. In January 2008, we also

declared five dividends in regards to preferred stock. The first was a $1.75

regular quarterly cash dividend on the 7 percent Cumulative Redeemable

Preferred Stock, Series B, payable April 25, 2008 to shareholders of

record on April 11, 2008. The second was a regular quarterly cash divi-

dend of $0.38775 per depositary share on the 6.204% Non-Cumulative

Preferred Stock, Series D, payable March 14, 2008 to shareholders of

record on February 29, 2008. The third was a regular quarterly cash divi-

dend of $0.33342 per depositary share on the Floating Rate

Non-Cumulative Preferred Stock, Series E, payable on February 15, 2008

to shareholders of record on January 31, 2008. The fourth was a regular

quarterly cash dividend of $0.41406 per depositary share on the 6.625%

Non-Cumulative Preferred Stock, Series I, payable April 1, 2008 to share-

holders of record on March 15, 2008. The fifth was the initial cash divi-

dend of $0.35750 per depositary share on the 7.25% Non-Cumulative

Preferred Stock, Series J, payable on February 1, 2008 to shareholders of

record on January 15, 2008.

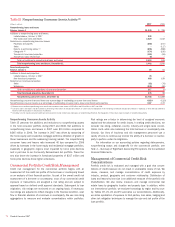

Common Share Repurchases

We expect to continue to repurchase shares, from time to time, in the

open market or in private transactions through our approved repurchase

programs. We repurchased approximately 73.7 million shares of common

stock in 2007 which more than offset the 53.5 million shares issued

under employee stock plans.

In January 2007, the Board authorized a stock repurchase program of

up to 200 million shares of the Corporation’s common stock at an

aggregate cost not to exceed $14.0 billion to be completed within a period

of 12 to 18 months of which the lesser of approximately $13.5 billion, or

189.4 million shares, remains available for repurchase under the program

at December 31, 2007.

Preferred Stock

In January 2008, we issued 240 thousand shares of Bank of America

Corporation Fixed-to-Floating Rate Non-Cumulative Preferred Stock, Series

K with a par value of $0.01 per share for $6.0 billion. The fixed rate is

8.00 percent through January 29, 2018 and then adjusts to three-month

LIBOR plus 363 bps thereafter. In addition, we issued 6.9 million shares

of Bank of America Corporation 7.25% Non-Cumulative Perpetual Con-

vertible Preferred Stock, Series L with a par value of $0.01 per share for

$6.9 billion.

In November and December 2007, the Corporation issued 41 thousand

shares of Bank of America Corporation 7.25% Non-Cumulative Preferred

Stock, Series J, with a par value of $0.01 per share for $1.0 billion.

In September 2007, the Corporation issued 22 thousand shares of

Bank of America Corporation 6.625% Non-Cumulative Preferred Stock,

Series I, with a par value of $0.01 per share for $550 million.

For additional information on the issuance and redemption of pre-

ferred stock, see Note 14 – Shareholders’ Equity and Earnings per Com-

mon Share to the Consolidated Financial Statements.

Credit Risk Management

Credit risk is the risk of loss arising from the inability of a borrower or

counterparty to meet its obligations. Credit risk can also arise from opera-

tional failures that result in an erroneous advance, commitment or invest-

ment of funds. We define the credit exposure to a borrower or counterparty

as the loss potential arising from all product classifications including loans

and leases, derivatives, trading account assets, assets held-for-sale,

deposit overdrafts and unfunded lending commitments that include loan

commitments, letters of credit and financial guarantees. Derivative posi-

tions, trading account assets and assets held-for-sale are recorded at fair

value, or the lower of cost or fair value. Loans and unfunded commit-

ments, which the Corporation elected to account for at fair value in

accordance with SFAS 159, are also recorded at fair value. Credit risk for

these categories of assets is not accounted for as part of the allowance

for credit losses but as part of the fair value adjustment recorded in earn-

ings in the period incurred. For derivative positions, our credit risk is

measured as the net replacement cost in the event the counterparties with

contracts in a gain position to us fail to perform under the terms of those

contracts. We use the current mark-to-market value to represent credit

exposure without giving consideration to future mark-to-market changes.

The credit risk amounts take into consideration the effects of legally

enforceable master netting agreements and cash collateral. Our consumer

and commercial credit extension and review procedures take into account

funded and unfunded credit exposures. For additional information on

derivatives and credit extension commitments, see Note 4 – Derivatives

and Note 13 – Commitments and Contingencies to the Consolidated

Financial Statements.

For credit risk purposes, we evaluate our consumer businesses on

both a held and managed basis. Managed basis assumes that loans that

have been securitized were not sold and presents earnings on these loans

in a manner similar to the way loans that have not been sold (i.e., held

loans) are presented. We evaluate credit performance on a managed basis

as the receivables that have been securitized are subject to the same

underwriting standards and ongoing monitoring as held loans. In addition

to the discussion of credit quality statistics of both held and managed

loans included in this section, refer to the Card Services discussion begin-

ning on page 47. For additional information on our managed portfolio and

securitizations, see Note 8 – Securitizations to the Consolidated Financial

Statements.

We manage credit risk based on the risk profile of the borrower or

counterparty, repayment sources, the nature of underlying collateral, and

other support given current events, conditions and expectations. We

classify our portfolios as either consumer or commercial and monitor

credit risk in each as discussed below.

The financial market conditions that existed in the second half of

2007 have continued to affect the economy and the financial services

sector in 2008. It remains unclear what impact the housing downturn,

declines in real estate values and the overall economic slowdown will

ultimately have and how long these conditions will exist. We expect that

certain industry sectors, in particular those that are dependent on the

housing sector, and certain geographic regions, will experience further

stress. Continued deterioration of the housing market, including reces-

sionary conditions, will negatively impact the credit quality of our consumer

portfolio as well as the credit quality of the consumer dependent sectors

of our commercial portfolio and will result in a higher provision for credit

losses in future periods. The degree of the impact will be dependent upon

the duration and severity of the housing downturn. As part of our credit

risk management culture, we continually evaluate our credit standards and

adjust them to be consistent with changes in the environment. For exam-

Bank of America 2007

69