Bank of America 2007 Annual Report Download - page 95

Download and view the complete annual report

Please find page 95 of the 2007 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

|

|

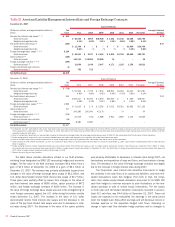

prices or interest rates beyond what is already implied in forward yield

curves at December 31, 2007, the pre-tax net losses are expected to be

reclassified into earnings as follows: $1.3 billion, or 19 percent within the

next year, 68 percent within five years, and 89 percent within 10 years,

with the remaining 11 percent thereafter. For more information on

derivatives designated as cash flow hedges, see Note 4 – Derivatives to

the Consolidated Financial Statements.

The amounts included in accumulated OCI for terminated derivative

contracts were losses of $3.8 billion and $3.2 billion, net-of-tax, at

December 31, 2007 and 2006. Losses on these terminated derivative

contracts are reclassified into earnings in the same period or periods dur-

ing which the hedged forecasted transaction affects earnings.

Mortgage Banking Risk Management

IRLCs and the related residential first mortgage loans held-for-sale are

subject to interest rate risk between the date of the IRLC and the date the

loans are sold to the secondary market. To hedge interest rate risk, we

utilize forward loan sale commitments and other derivative instruments

including purchased options. These instruments are used as economic

hedges of IRLCs and residential first mortgage loans held-for-sale. At

December 31, 2007, the notional amount of derivatives economically

hedging the IRLCs and residential first mortgage loans held-for-sale was

$18.6 billion.

The Corporation adopted SFAS 159 as of January 1, 2007 and

elected to account for certain originated mortgage loans held-for-sale at

fair value. Subsequent to the adoption, mortgage loan origination costs

are recognized in noninterest expense when incurred. Previously, mortgage

loan origination costs would have been capitalized as part of the carrying

amount of the loans and recognized as a reduction of mortgage banking

income upon the sale of such loans. At December 31, 2007, residential

mortgage loans held-for-sale in connection with mortgage banking activ-

ities for which the fair value option was elected had an aggregate fair

value of $9.56 billion and an aggregate outstanding principal balance of

$9.82 billion. Net gains resulting from changes in fair value of loans

held-for-sale that we originated, including realized gains and losses on

sale of $333 million, were recorded in mortgage banking income during

2007. The adoption of SFAS 159 resulted in an increase of $256 million

in mortgage banking income during 2007, and in an increase of $212 mil-

lion in noninterest expense during 2007.

We manage changes in the value of MSRs by entering into derivative

financial instruments. MSRs are a nonfinancial asset created when the

underlying mortgage loan is sold to investors and we retain the right to

service the loan. We use certain derivatives such as options and interest

rate swaps as economic hedges of MSRs. At December 31, 2007, the

amount of MSRs identified as being hedged by derivatives was approx-

imately $3.1 billion. The notional amount of the derivative contracts des-

ignated as economic hedges of MSRs at December 31, 2007 was $69.0

billion. For additional information on MSRs see Note 21 – Mortgage Servic-

ing Rights to the Consolidated Financial Statements.

Operational Risk Management

Operational risk is the risk of loss resulting from inadequate or failed

internal processes, people and systems, including system conversions

and integration, and external events. Successful operational risk manage-

ment is particularly important to diversified financial services companies

because of the nature, volume and complexity of the financial services

business.

We approach operational risk from two perspectives: corporate-wide

and line of business-specific. The Compliance and Operational Risk

Committee provides oversight of significant corporate-wide operational and

compliance issues. Within Global Risk Management, Enterprise Opera-

tional Risk Management develops policies, practices, controls and

monitoring tools for assessing and managing operational risks across the

Corporation. We also mitigate operational risk through a broad-based

approach to process management and process improvement. Improve-

ment efforts are focused on reduction of variation in outputs. We have a

dedicated Quality and Productivity team to manage and certify the process

management and improvement efforts. For selected risks, we use speci-

alized support groups, such as Information Security and Supply Chain

Management, to develop corporate-wide risk management practices, such

as an information security program and a supplier program to ensure that

suppliers adopt appropriate policies and procedures when performing work

on behalf of the Corporation. These specialized groups also assist the

lines of business in the development and implementation of risk manage-

ment practices specific to the needs of the individual businesses. These

groups also work with line of business executives and risk executives to

develop appropriate policies, practices, controls and monitoring tools for

each line of business. Through training and communication efforts, com-

pliance and operational risk awareness is driven across the Corporation.

The lines of business are responsible for all the risks within the

business line, including operational risks. Operational and Compliance

Risk executives, working in conjunction with senior line of business execu-

tives, have developed key tools to help identify, measure, mitigate and

monitor operational risk in each business line. Examples of these include

personnel management practices, data reconciliation processes, fraud

management units, transaction processing monitoring and analysis, busi-

ness recovery planning and new product introduction processes. In addi-

tion, the lines of business are responsible for monitoring adherence to

corporate practices. Line of business management uses a self-

assessment process, which helps to identify and evaluate the status of

risk and control issues, including mitigation plans, as appropriate. The

goal of the self-assessment process is to periodically assess changing

market and business conditions, to evaluate key operational risks impact-

ing each line of business, and assess the controls in place to mitigate the

risks. In addition to information gathered from the self-assessment proc-

ess, key operational risk indicators have been developed and are used to

help identify trends and issues on both a corporate and a line of business

level.

Recent Accounting and Reporting

Developments

See Note 1 – Summary of Significant Accounting Principles to the Con-

solidated Financial Statements for a discussion of recently issued account-

ing pronouncements.

Complex Accounting Estimates

Our significant accounting principles, as described in Note 1 – Summary of

Significant Accounting Principles to the Consolidated Financial State-

ments, are essential in understanding the MD&A. Many of our significant

accounting principles require complex judgments to estimate values of

assets and liabilities. We have procedures and processes to facilitate

making these judgments.

The more judgmental estimates are summarized below. We have

identified and described the development of the variables most important

in the estimation process that, with the exception of accrued taxes,

involve mathematical models to derive the estimates. In many cases,

there are numerous alternative judgments that could be used in the proc-

ess of determining the inputs to the model. Where alternatives exist, we

Bank of America 2007

93