Bank of America 2004 Annual Report Download - page 102

Download and view the complete annual report

Please find page 102 of the 2004 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

|

|

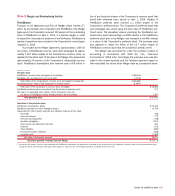

$10.0 billion. There was no material impact to Net Income or Tier 1

Capital as a result of the adoption of FIN 46 or the subsequent

deconsolidation of this entity, and prior periods were not restated. In

December 2003, the FASB issued FASB Interpretation No. 46

(Revised December 2003), “Consolidation of Variable Interest

Entities, an interpretation of ARB No. 51” (FIN 46R), which is an

update of FIN 46. The Corporation adopted FIN 46R as of March 31,

2004. Adoption of this rule did not have a material impact on the

Corporation’s results of operations or financial condition. For addi-

tional information on VIEs, see Note 8 of the Consolidated Financial

Statements.

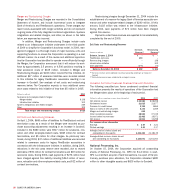

On December 12, 2003, the American Institute of Certified

Public Accountants issued Statement of Position No. 03-3,

“Accounting for Certain Loans or Debt Securities Acquired in a

Transfer” (SOP 03-3). SOP 03-3 requires acquired impaired loans for

which it is probable that the investor will be unable to collect all

contractually required payments receivable to be recorded at the

present value of amounts expected to be received and prohibits

carrying over or creation of valuation allowances in the initial

accounting for these loans. SOP 03-3 is effective for loans acquired

in fiscal years beginning after December 31, 2004. SOP 03-3 is not

expected to have a material impact on the Corporation’s results of

operations or financial condition.

On March 9, 2004, the Securities and Exchange Commission

(SEC) issued Staff Accounting Bulletin No. 105, “Application of

Accounting Principles to Loan Commitments” (SAB 105), which spec-

ifies that servicing assets embedded in commitments for loans to be

held-for-sale should be recognized only when the servicing asset has

been contractually separated from the associated loans by sale or

securitization. The adoption of SAB 105 is effective for commitments

entered into after March 31, 2004. The adoption of SAB 105 had no

material impact on the Corporation’s results of operations or financial

condition.

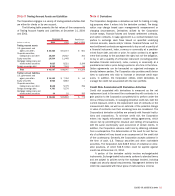

On March 18, 2004, the Emerging Issues Task Force (EITF)

issued EITF 03-1, “The Meaning of Other-Than-Temporary Impairment

and Its Application to Certain Investments” (EITF 03-1). EITF 03-1

provides recognition and measurement guidance regarding when

impairments of equity and debt securities are considered other-than-

temporary thereby requiring a charge to earnings, and also requires

additional annual disclosures for investments in unrealized loss posi-

tions. The additional annual disclosure requirements were previously

issued by the EITF in November 2003 and were effective for the

Corporation for the year ended December 31, 2003. In September

2004, the FASB issued FASB Staff Position (FSP) EITF 03-1-1, which

delays the recognition and measurement provisions of EITF 03-1

pending the issuance of further implementation guidance. We are

currently evaluating the effect of the recognition and measurement

provisions of EITF 03-1.

In the third quarter of 2004, the Corporation adopted FSP No.

FAS 106-2, “Accounting and Disclosure Requirements Related to the

Medicare Prescription Drug, Improvement and Modernization Act of

2003” (FSP No. 106-2), which superseded FSP No. FAS 106-1. FSP

No. 106-2 provides authoritative guidance on accounting for the fed-

eral subsidy and other provisions of the Medicare Prescription Drug,

Improvement and Modernization Act of 2003 (the Medicare Act). The

effects of these provisions were recognized prospectively from July 1,

2004. A remeasurement on that date resulted in a reduction of $53

million in the Corporation’s accumulated postretirement benefit obli-

gation. In addition, the Corporation’s net periodic benefit cost for

other postretirement benefits has decreased by $15 million for 2004

as a result of the remeasurement.

On December 16, 2004, the FASB issued Statement of Financial

Accounting Standards (SFAS) No. 123 (revised 2004) “Share-based

Payment” (SFAS 123R) which eliminates the ability to account for

share-based compensation transactions using Accounting Principles

Board (APB) Opinion No. 25, “Accounting for Stock Issued to

Employees,” (APB 25) and generally requires that such transactions

be accounted for using a fair value-based method with the resulting

compensation cost recognized over the period that the employee is

required to provide service in order to receive their compensation.

SFAS 123R also amends SFAS No. 95, “Statement of Cash Flows,”

requiring the benefits of tax deductions in excess of recognized com-

pensation cost to be reported as a financing cash flow, rather than

as an operating cash flow as currently required. The Corporation

plans to adopt SFAS 123R beginning July 1, 2005, using the modi-

fied-prospective method. The Corporation adopted the fair value-

based method of accounting for stock-based employee compensation

prospectively as of January 1, 2003, and as a result, adoption of

SFAS 123R is not expected to have a material impact on the

Corporation’s results of operations or financial condition.

On December 21, 2004, the FASB issued FSP No. 109-2,

“Accounting and Disclosure Guidance for the Foreign Earnings

Repatriation Provision within the American Jobs Creation Act of

2004” (FSP No. 109-2). FSP No. 109-2 provides accounting and

disclosure guidance for the foreign earnings repatriation provision

within the American Jobs Creation Act of 2004 (the Act). The Act,

signed into law on October 22, 2004, provided U.S. companies with

the ability to elect to apply a special one-time tax deduction equal to

85 percent of certain earnings remitted from foreign subsidiaries,

provided certain criteria are met. Much of the detailed guidance

about how this special deduction will operate has yet to be issued

by the U.S. Department of the Treasury and the Internal Revenue

BANK OF AMERICA 2004 101