Bank of America 2004 Annual Report Download - page 32

Download and view the complete annual report

Please find page 32 of the 2004 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

|

|

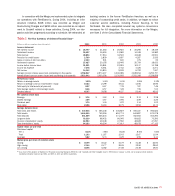

Nonperforming assets were 0.47% of total loans,

leases and foreclosed properties, or $2.46 billion, as of

December 31, 2004. This compared to 0.81%, or $3.02

billion, on December 31, 2003.

The allowance for loan and lease losses stood at

1.65% of loans and leases, or $8.63 billion, on December

31, 2004. This compared to 1.66%, or $6.16 billion, on

December 31, 2003. Criticized exposure declined from

$12.7 billion or 5.9% of total utilized commercial exposure

in 2003, to $10.2 billion or 3.4% in 2004.

Capital

Bank of America’s capital position remained strong in

2004. Total shareholders’ equity was $99.6 billion at

December 31, 2004, representing 9% of period-end assets

of $1.1 trillion. The Tier 1 capital ratio rose to 8.1% from

7.9% at the end of 2003.

Business segments

Global Consumer and Small Business Banking earned

$6.55 billion. In addition to adding Fleet, this segment

achieved strong growth in checking and savings

accounts, which helped to drive double-digit growth in

deposit balances. Home equity and credit card loan

outstandings grew. Mortgage results were adversely

affected by higher interest rates, which significantly

reduced refinance volumes, and by adjustments to the

value of mortgage servicing rights.

Global Business and Financial Services earned

$2.83 billion. The main drivers of this segment’s perform-

ance were significant improvements in credit quality,

which resulted in negative provision expense. Excluding

the impact of Fleet, loans grew modestly during the year

and deposits also rose. Treasury management fee growth

also contributed to higher net income.

Global Capital Markets and Investment Banking

earned $1.95 billion in 2004 and had negative provision

expense due to improved credit quality. Excluding the

impact of Fleet, investment banking income increased,

reflecting the company’s continued buildout of that

platform, and trading-related revenue also rose.

Results were adversely impacted by the mutual fund

settlement.

Global Wealth and Investment Management

earned $1.58 billion. Excluding the addition of Fleet,

growth in assets under management and earnings was

driven by strong performance in the credit portfolios of

Premier Banking and The Private Bank and increased

market valuations in the asset management portfolio.

Results were adversely impacted by the mutual fund

settlement.

BANK OF AMERICA 2004 31