Bank of America 2004 Annual Report Download - page 49

Download and view the complete annual report

Please find page 49 of the 2004 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

|

|

48 BANK OF AMERICA 2004

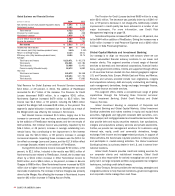

Partially offsetting these increases were declines in interest rate

and equities revenues. Interest rate revenues declined by $287 million,

or 30 percent, largely due to reduced corporate customer activity and

lower trading-related profits as a result of FRB tightening, uncertainty

related to the election, declining volatility in the options market and

more subdued economic growth than anticipated during the year.

Trading-related equities revenues declined by $149 million, or 43 percent.

Including commissions on equity transactions, trading-related equities

revenues declined $131 million, or 13 percent. The overall decline in

trading-related equities revenue was driven by net losses on a single

retained stock position in 2004 combined with the absence of gains

on a single position that we recorded in 2003.

Total trading-related revenues also included the cost associated

with credit portfolio hedges of $144 million in 2004, an improvement

of $186 million. The improvement was primarily due to stable

spreads in the first half of the year versus spreads tightening

throughout 2003.

The Provision for Credit Losses decreased $762 million to a

negative $459 million due to notable improvements in credit quality

in the large corporate portfolio partially due to the high levels of

liquidity in the capital markets, which enabled us to distribute paper

more readily. Also contributing to the decrease in the Provision for

Credit Losses was the reduction in net charge-offs of $311 million, or

71 percent. Additionally, nonperforming assets declined $589 million,

or 58 percent, to $424 million at December 31, 2004. For more

information, see Credit Risk Management beginning on page 58.

Noninterest Expense increased $1.2 billion, or 23 percent. This

increase was due, in part, to an increase in litigation-related charges

of $460 million, including the reversal of legal expenses previously

recorded in All Other that were reclassified to this segment. Also

impacting Noninterest Expense were higher incentive compensation

for market-based activities of $279 million and the mutual fund

settlement of $143 million.

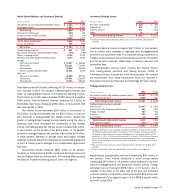

Global Wealth and Investment Management

This segment provides tailored investment services to individual and

institutional clients in various stages and economic cycles. Our

clients are served through five major businesses, Premier Banking,

Banc of America Investments (BAI), The Private Bank, Columbia

Management Group (CMG) and Other Services, each offering specific

products and services based on clients’ needs.

Premier Banking joins with BAI, our full-service retail brokerage

business, to bring together personalized banking and investment

expertise through priority service with client-dedicated teams. These

teams provide comprehensive advice, cash management strategies,

and customized investment and financial planning solutions for mass

affluent clients. Mass affluent clients have a personal wealth profile

that includes investable assets plus a mortgage that exceeds

$250,000 or they have at least $100,000 of investable assets.

BAI serves 1.3 million accounts through a network of over

2,100 financial advisors throughout the U.S.

The Private Bank provides integrated wealth management solu-

tions to high-net-worth individuals, mid-market institutions and chari-

table organizations with investable assets greater than $3 million.

Services include investment, trust, banking and lending services.

During the third quarter of 2004, we announced a new business

designed to serve the needs of ultra high-net-worth individuals and

families. The goal is for this new business to provide a higher level

of contact and tailored wealth management solutions to clients with

investable assets greater than $50 million. We expect this business

to be rolled out during the first quarter of 2005.

CMG is an asset management organization primarily serving the

needs of institutional customers. CMG provides asset management

services, liquidity strategies and separate accounts. CMG also provides

mutual funds offering a full range of investment styles across an array

of products including equities, fixed income (taxable and nontaxable)

and cash products. In addition to its service of institutional clients,

CMG distributes its products and services to individuals through

The Private Bank,BAI and nonproprietary channels including other

brokerage firms.

Other Services include the Investment Services Group, which

provides products and services from traditional capital markets

products to alternative investments and Banc of America Specialist,a

New York Stock Exchange market-maker. Other Services also included

U.S. Clearing which provides retail clearing services to broker/dealers

and other correspondent firms. U.S. Clearing was sold in the fourth

quarter of 2004.

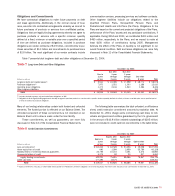

Global Wealth and Investment Management

(Dollars in millions) 2004 2003

Net interest income (fully taxable-equivalent basis) $ 2,854 $ 1,952

Noninterest income 3,064 2,078

Total revenue 5,918 4,030

Provision for credit losses (20) 11

Noninterest expense 3,449 2,101

Income before income taxes 2,489 1,918

Income tax expense 905 684

Net income $ 1,584 $ 1,234

Shareholder value added $ 782 $ 854

Net interest yield (fully taxable-equivalent basis) 3.35% 3.52%

Return on average equity 20.17 33.94

Efficiency ratio (fully taxable-equivalent basis) 58.28 52.11

Average:

Total loans and leases $ 44,049 $ 37,675

Total assets 91,443 58,606

Total deposits 83,049 53,996

Common equity/Allocated equity 7,854 3,637

Year end:

Total loans and leases 49,776 38,689

Total assets 121,974 69,370

Total deposits 111,107 62,730