Bank of America 2004 Annual Report Download - page 82

Download and view the complete annual report

Please find page 82 of the 2004 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

|

|

BANK OF AMERICA 2004 81

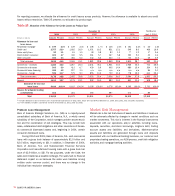

Goodwill

The nature of and accounting for Goodwill is discussed in detail in

Notes 1 and 9 of the Consolidated Financial Statements. Goodwill is

reviewed for potential impairment at the reporting unit level on an

annual basis, or in interim periods if events or circumstances indicate

a potential impairment. The reporting units utilized for this test were

those that are one level below the business segments identified on

page 40. The impairment test is performed in two phases. The first

step of the Goodwill impairment test compares the fair value of the

reporting unit with its carrying amount, including Goodwill. If the fair

value of the reporting unit exceeds its carrying amount, Goodwill of

the reporting unit is considered not impaired; however, if the carrying

amount of the reporting unit exceeds its fair value, an additional pro-

cedure must be performed. That additional procedure compares the

implied fair value of the reporting unit’s Goodwill (as defined in SFAS

142) with the carrying amount of that Goodwill. An impairment loss

is recorded to the extent that the carrying amount of Goodwill

exceeds its implied fair value.

The fair values of the reporting units were determined using a

combination of valuation techniques consistent with the income

approach and the market approach. For purposes of the income

approach, discounted cash flows were calculated by taking the net

present value of estimated cash flows using a combination of histor-

ical results, estimated future cash flows and an appropriate price to

earnings multiple. We use our internal forecasts to estimate future

cash flows and actual results may differ from forecasted results.

However, these differences have not been material and we believe

that this methodology provides a reasonable means to determine fair

values. Cash flows were discounted using a discount rate based on

expected equity return rates, which was 11 percent for 2004.

Expected rates of equity returns were estimated based on historical

market returns and risk/return rates for similar industries of the

reporting unit. For purposes of the market approach, valuations of

reporting units were based on actual comparable market transac-

tions and market earnings multiples for similar industries of the

reporting unit.

Our evaluations for the year ended December 31, 2004 indicated

there was no impairment of our Goodwill.

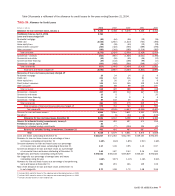

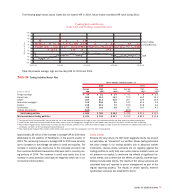

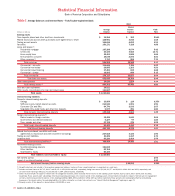

2003 Compared to 2002

The following discussion and analysis provides a comparison of our

results of operations for 2003 and 2002. This discussion should be

read in conjunction with the Consolidated Financial Statements and

related Notes on pages 96 through 150. In addition, Tables 1 and 2

contain financial data to supplement this discussion.

Overview

Net Income

Net Income totaled $10.8 billion, or $3.57 per diluted common

share, in 2003 compared to $9.2 billion, or $2.95 per diluted com-

mon share, in 2002. The return on average common shareholders’

equity was 21.99 percent in 2003 compared to 19.44 percent in

2002. These earnings provided sufficient cash flow to allow us to

return $9.8 billion and $8.5 billion in 2003 and 2002, respectively,

in capital to shareholders in the form of dividends and share

repurchases, net of employee stock options exercised.

Net Interest Income

Net Interest Income on a FTE basis increased $596 million to $22.1

billion in 2003. This increase was driven by higher ALM portfolio lev-

els (consisting of securities, whole loan mortgages and derivatives),

higher consumer loan levels, larger trading-related contributions,

higher mortgage warehouse and higher core deposit funding levels.

Partially offsetting these increases was the impact of lower interest

rates and reductions in the large corporate, foreign and exited con-

sumer loan businesses portfolios. The net interest yield on a FTE

basis declined 37 bps to 3.40 percent in 2003 due to the negative

impact of increases in lower-yielding trading-related assets and declin-

ing rates offset partially by our ALM portfolio repositioning.

Noninterest Income

Noninterest Income increased $2.9 billion to $16.5 billion in 2003,

due to increases in Mortgage Banking Income of $1.2 billion, Equity

Investment Gains of $495 million, Other Noninterest Income of $484

million, Card Income of $432 million, and Service Charges of $342

million. The increase in Mortgage Banking Income was driven by

gains from higher volumes of mortgage loans sold into the secondary

market and improved profit margins. Other Noninterest Income of

$1.1 billion included gains of $772 million, an increase of $272 million

over 2002, as we sold whole loan mortgages to manage prepayment

risk due to the longer than anticipated low interest rate environment.

Additionally, Other Noninterest Income included the equity in the

earnings of our investment in GFSS of $122 million.